Strategist

• 月次アウトルック

The power play pivot: Navigating the Fed-Trump clash

President Trump’s threats to the independence of the US Federal Reserve has implications for markets that may not yet be priced in, says strategist Peter van der Welle.

まとめ

- US central bank is under pressure from President Trump to cut rates

- Level of independence affects demand for equities, bonds and gold

- Three scenarios that have implications for multi-asset allocation

A litany of aggressive policies, from extensive tariffs on ‘Liberation Day’, to unprecedented insults sent to the Fed chairman after he refused to bow to pressure to cut interest rates, have already rattled equities and sovereign bonds. Safe havens such as gold have hit record highs since President Trump took office in January.

Yet, markets may be under-reacting to potential significance of the ongoing power play with the US central bank – traditionally independent from the US government since its creation in 1913 – says Van der Welle, multi-asset strategist with Robeco Investment Solutions.

A cornerstone of credibility

“The independence of central banks, particularly the US Federal Reserve, has long stood as a cornerstone of credible monetary policy and financial market stability,” he says. “Being credible as a central bank means medium-term inflation expectations remain well anchored, safeguarding future real purchasing power.”

“In our 2023 Expected Returns publication, ‘Triple Power Play’, we saw a power play unfold between the US central bank and US administration in the next five years as fiscal dominance has been on the rise post-Covid.”

“Recently, the tension between fiscal and monetary authorities has intensified, with the Fed increasingly battered with attacks from President Trump on social media, and legal efforts to fire Fed board member Lisa Cook ‘for cause’.”

“The outcome of this power play and the resulting degree and durability of Fed independence could have major impacts on financial markets and even amount to a regime change.”

Do markets care?

Effects of the Trump-Fed clash on the markets have so far reflected a belief that the Fed will maintain its independence, but this confidence could be misplaced, Van der Welle says.

“At first glance, bond market volatility has remained remarkably well behaved, and the US 10-year yield remains 50 bps below its 13 January peak,” he says. “This might indicate that the market is confident that the Fed remains resilient, and its institutional safeguards against political pressure are holding.”

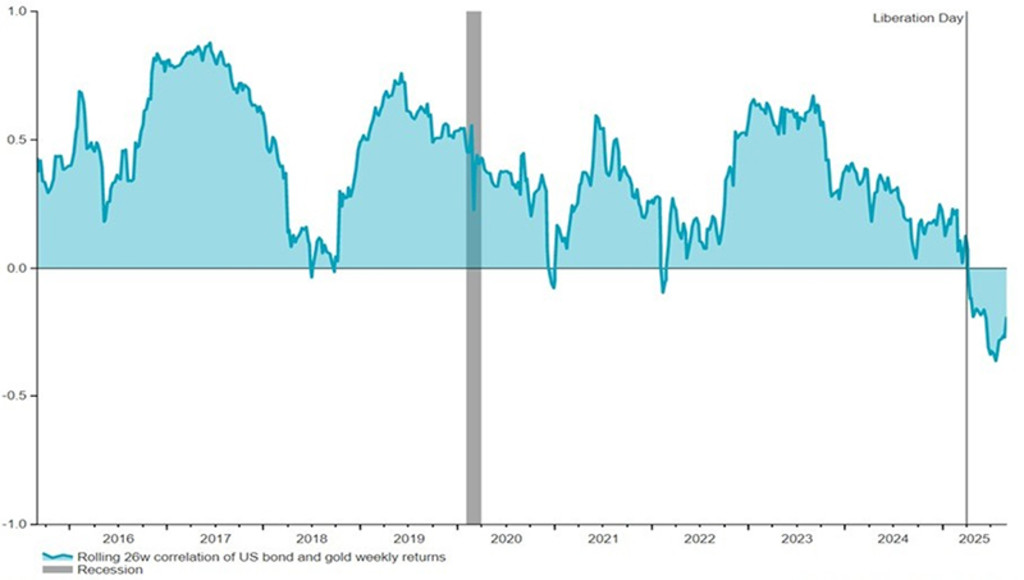

“Yet, a closer inspection unveils that there is something brewing. Since ‘Liberation Day’, the correlation between the 10-year Treasury bond and gold has turned negative. At the same time, the 2-year Treasury yield has declined while 5-year inflation swaps have edged higher; that’s an unusual constellation.”

“Also, the start of the Trump presidency has ushered in a dollar bear market. The depreciation of the dollar in 2025 could be indicative the FX market is recalibrating the probability of a fiscally led policy regime. Research shows that currencies tend to depreciate when the probability of higher future inflation is being discounted under fiscal dominance.”

Figure 1: The correlation between the 10-year Treasury and gold has become negative

Past results are no guarantee of future performance. The value of your investments may fluctuate.

Source: LSEG Datastream, Robeco, September 2025

最新のインサイトを受け取る

投資に関する最新情報や専門家の分析を盛り込んだニュースレター(英文)を定期的にお届けします。

Implications for asset allocation

So, what does this mean for asset allocation? The Investment Solutions team has analysed data going back to 2004 to see which assets benefit most or least from levels of central bank independence.

“A power play between the Fed and President Trump is not merely a theoretical concern; it brings along a notable return dispersion for global multi-asset allocators,” Van der Welle says.

“For instance, while US Treasuries are positively correlated with Fed independence, low-quality assets like Russell 2000 stocks and high yield bonds are negatively correlated. Clearly, an independent Fed is not a friend of small caps.”

“When central bank independence is robust, the term structure of interest rates tends to reflect economic fundamentals and well-anchored inflation expectations. Any erosion of independence could prompt investors to demand higher yields as compensation for inflation uncertainty, leading to steepening yield curves.”

Figure 2: The correlation between Fed independence and asset returns in the following 12 months

Past results are no guarantee of future performance. The value of your investments may fluctuate.

Source: LSEG Datastream, Robeco, September 2025

Flight into safe havens

As ever, the traditional safe haven of gold does benefit from any kind of uncertainty, while the allure of US Treasuries is declining. “When markets question central bank autonomy, currency volatility rises, often triggering capital flight to alternative safe assets,” Van der Welle says.

“While the Fed’s institutional strength makes capital flight look like a distant risk, the rally in gold coinciding with a dollar bear market in the year to date suggests the market is reassessing safe havens.”

“The pricing of risk assets, from US equities to global high yield bonds, depends heavily on expectations about monetary policy. Our research shows that assets that are lower in credit quality, like high yield and small caps, are outperformers in an environment of eroding Fed autonomy.”

“Among equity factors, the Quality factor has lagged Growth, Value and Momentum in 2025. These observations correlate with the prospect of artificially low interest rates under a lenient Fed. In turn, this may blunt risk perception, fuelling returns in low-quality segments of financial markets that are cheap and have lagged so far in this bull market.”

Three scenarios for assets

As for the likely outcome of the Fed-Trump power play, the Investment Solutions team sees three potential scenarios, each with an equal probability of about one-third.

Scenario 1: Independence is preserved: Expect US curve flattening, relative stability in the dollar and a more predictable risk environment. The correlation between gold and Treasuries becomes positive again. Small-cap outperformance reverses.

Scenario 2: Independence erodes: Expect US curve steepening, a deepening dollar bear market and a less predictable risk environment. The correlation between gold and Treasuries stays negative, and gold has further upside. Small-cap outperformance continues.

Scenario 3: Fully fledged fiscal dominance: The Fed proves to be loyal to President Trump’s wishes like it was to President Nixon in the early 1970s. US inflation risks become paramount. Hedging demand for inflation protection surges, benefitting real assets. A dollar bear market becomes secular in nature, benefiting assets in Europe and emerging markets.

The risk of under-reacting

“Given our findings, and the likelihood of the Fed-Trump power play staying in place, investors should take a scenario-driven approach to asset allocation,” Van der Welle says.

“While the odds of a further erosion of Fed independence have increased in our view, this is not a given.”

“Moreover, in the wake of disappointing non-farm payrolls, the market might brush aside the Fed independence debate in a scenario where the US labour market breaks, and the continued absence of tariff-induced inflation allows the Fed to cut rates without these cuts being seen as politically motivated.”

“Constant pressure on the Fed does erode its independence, but with markets underreacting to White House policy actions, the increased mispricing of risk in an environment where the Fed gives in to political pressure raises the odds of this bull market moving toward an exuberant phase.”

Risk of high inflation

While equity markets are seemingly unresponsive for now, the return of high inflation could pour cold water on the bull market at a later stage.

“Equity markets might continue to favor pressure on the Fed until realized inflation reaches the 3.5% to 4% level, where historically, equities tend to struggle, and the bond-equity correlation turns positive,” Van der Welle concludes.

重要事項

当資料は情報提供を目的として、ロベコ・ジャパン株式会社(以下「当社」)が独自に作成、または当社のグループ会社(Robeco Institutional Asset Management B.V.およびその関連会社を含む)から提供された資料を当社が編集・翻訳したものです。資料中の個別の金融商品の売買の勧誘や推奨等を目的とするものではありません。記載された情報は十分信頼できるものであると考えておりますが、その正確性、完全性を保証するものではありません。意見や見通しはあくまで作成日における弊社の判断に基づくものであり、今後予告なしに変更されることがあります。運用状況、市場動向、意見等は、過去の一時点あるいは過去の一定期間についてのものであり、過去の実績は将来の運用成果を保証または示唆するものではありません。また、記載された投資方針・戦略等は全ての投資家の皆様に適合するとは限りません。当資料は法律、税務、会計面での助言の提供を意図するものではありません。 ご契約に際しては、必要に応じ専門家にご相談の上、最終的なご判断はお客様ご自身でなさるようお願い致します。 運用を行う資産の評価額は、組入有価証券等の価格、金融市場の相場や金利等の変動、及び組入有価証券の発行体の財務状況による信用力等の影響を受けて変動します。また、外貨建資産に投資する場合は為替変動の影響も受けます。運用によって生じた損益は、全て投資家の皆様に帰属します。したがって投資元本や一定の運用成果が保証されているものではなく、投資元本を上回る損失を被ることがあります。弊社が行う金融商品取引業に係る手数料または報酬は、締結される契約の種類や契約資産額により異なるため、当資料において記載せず別途ご提示させて頂く場合があります。具体的な手数料または報酬の金額・計算方法につきましては弊社担当者へお問合せください。 当資料及び記載されている情報、商品に関する権利は弊社に帰属します。したがって、弊社の書面による同意なくしてその全部もしくは一部を複製またはその他の方法で配布することはご遠慮ください。 商号等: ロベコ・ジャパン株式会社 金融商品取引業者 関東財務局長(金商)第2780号 加入協会: 一般社団法人 資産運用業協会