Strategist

• インサイト

What to do when safe havens turn into stormy waters

The traditional safe-haven asset of US Treasury bonds is not as safe as it once was, say Peter van der Welle, Laurens Swinkels and Martin van Vliet, in an excerpt of a special topic produced for our five-year outlook.

執筆者

Head of Solutions Research

Strategist

まとめ

- Safe-haven assets can withstand turbulence and keep their value over the long term

- US Treasuries’ safe-haven status has been steadily eroded by deficits and inflation

- Gold, defensive equities and fiat currencies like the Swiss franc are good alternatives

A safe-haven asset can retain or even gain value during market turbulence or stock market downturns. They are widely accepted and easy to sell, even during crisis periods, as they tend to be relatively insensitive to new information about whatever is causing the panic. In the long run, safe-haven assets keep their value in real terms.

Government debt has long been seen as a natural safe haven. However, investors have begun to question governments’ willingness or ability to pay back bondholders without causing high inflation, which reduces their safe-haven status. At other times, central bank policies keep interest rates below inflation, reducing their long-term store of value.

Several episodes in the past three years have cast further doubts. The Covid pandemic prompted governments to take unprecedented fiscal measures to counter the economic impact of lockdowns, causing deficits and government debt levels to reach new highs, raising concerns on debt sustainability.

The role of government bonds as a hedge against equity market volatility was further challenged in 2022, when they posted large negative returns during that year’s stock market falls, offering little diversification benefits. The UK Gilt market experienced its own crisis in September 2022 when the proposed budget of Liz Truss triggered a sell-off in the vast liability-driven investment market, leading to her resignation as prime minister.

More recently, French government bonds (OATs) came under pressure after President Macron called for snap elections in June 2024. This surprised bond markets and caused the yields on OATs to widen significantly versus German Bunds.

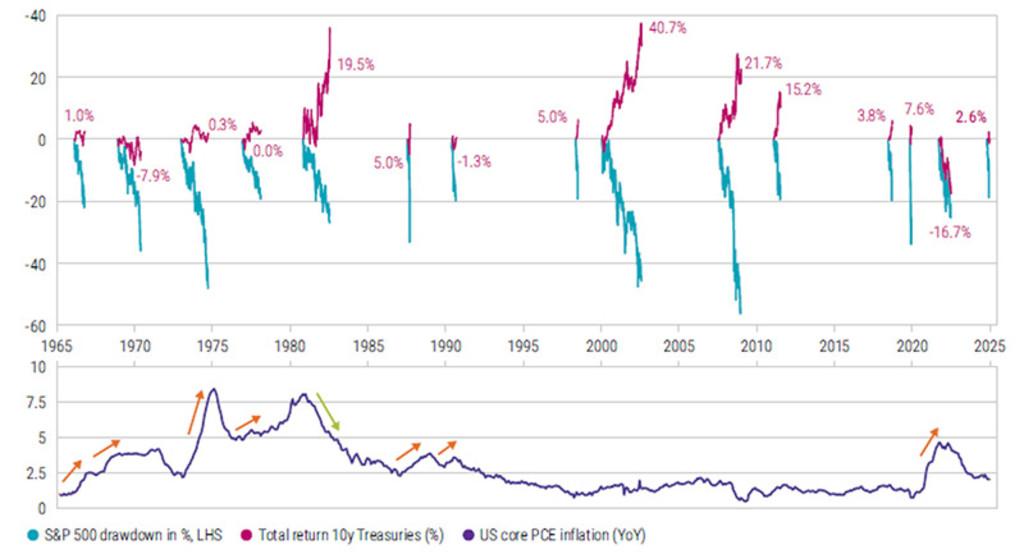

To assess whether the safe-haven status of US Treasuries has truly been compromised, we began by compiling an overview of historical equity market corrections exceeding 15% over the past 60 years. We then analyzed the performance of 10-year Treasuries during these corrections. Figure 1 below illustrates a total return of approximately 2.5% during the nearly 20% correction in the S&P 500 that began in February 2025 and ended on 9 April.

This 2.5% return stands in stark contrast to the high returns seen after the dotcom bust (2000/2001) and the Global Financial Crisis (2008/2009), when the Federal Reserve significantly lowered short-term interest rates. However, it is notably better than the 16.7% negative return in 2022, when the Fed aggressively raised rates in response to high inflation, and better than the returns during the 1960s and 1970s, when high or rapidly rising inflation caused similar issues.

Figure 1: Performance of 10-year Treasuries during S&P 500 corrections of at least 15%

Past results are no guarantee of future performance. The value of your investments may fluctuate. Source: Robeco, July 2025.

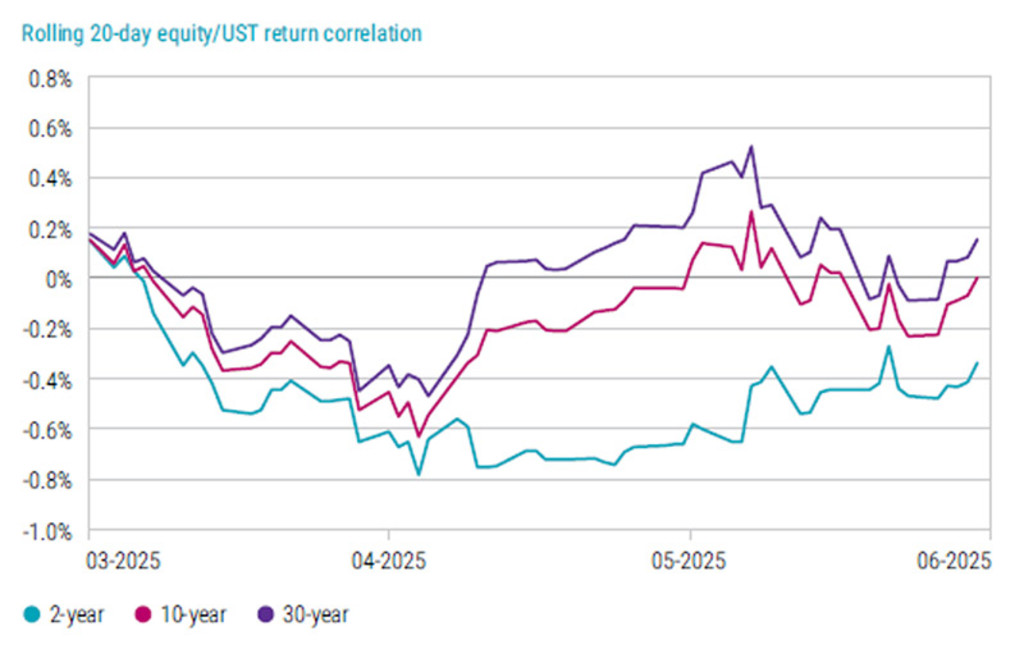

At first glance, 10-year Treasuries thus appear to have fulfilled their expected role: preserving capital or delivering a positive return during a significant equity market downturn. However, a closer look at the panic phase of the correction – late March to mid-April 2025 – reveals a different picture. During this period, 10- and 30-year bonds failed to perform their safe-haven function.

In fact, the correlation between equity and bond returns turned from negative to positive. Interestingly, the equity/bond correlation for 2-year Treasuries remained negative (see Figure 2 below), indicating that short-term bonds continued to act as safe havens. This is somewhat surprising, given that the trade tariffs announced in early April – though temporarily inflationary – would have been expected to impact shorter maturities more severely.

Figure 2: Correlation between US Treasuries and US equity markets

Past results are no guarantee of future performance. The value of your investments may fluctuate. Source: Robeco, June 2025.

最新のインサイトを受け取る

投資に関する最新情報や専門家の分析を盛り込んだニュースレター(英文)を定期的にお届けします。

Can other asset classes be safe havens?

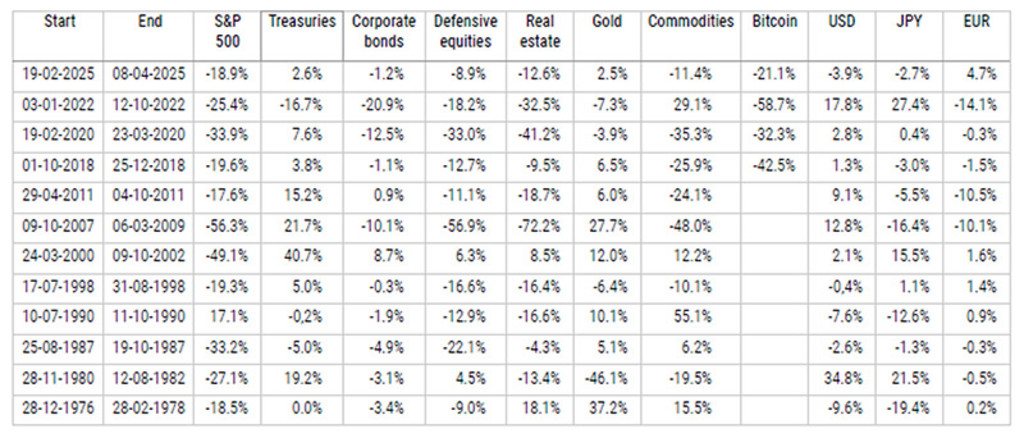

It’s not just US Treasuries that can act as a safe haven of course. Gold has been considered one for centuries. Other asset classes include highly rated corporate bonds, defensive equities and fiat currencies – but are they reliable? The table below shows asset class returns during major falls in the S&P 500 since the 1970s.

Table 1: Asset class returns during equity market corrections

Past results are no guarantee of future performance. The value of your investments may fluctuate. Source: Robeco, LSEG, June 2025.

Highly rated corporate bonds can sometimes have lower interest rates than government bonds but are not reliable safe havens. This is due to their small volume and sensitivity to changes in credit risk, which is in turn vulnerable to a changing macroeconomic landscape. Their liquidity tends to dry up during crisis periods, and so they may not be good stores of long-term value during times of financial repression.

Inflation-linked bonds protect against inflation but also tend to become less liquid during crises due to limited supply. They are however a relatively new asset class, and future scenarios with increased inflation risk may increase their safe-haven status, especially due to their long-term store of real value.

Defensive stocks that supply essential goods such as food, utilities, and health care have lower risk. Table 1 shows that defensive equities outperformed the general equity market during large drawdowns on average by more than 10%. They are less prone to long-term real value erosion than government debt or cash, and may therefore be a better store of value.

Turning to gold for millennia

And then there is gold, which has historically been used as a foundation for paper currency systems due to its rarity, durability, and ease of transaction. It has maintained its value over millennia; banks recognize gold as Tier 1 capital under Basel regulations. However, gold can be stolen and does not generate income, incurring storage costs instead.

Table 1 shows that during Global Financial Crisis, gold outperformed all other asset classes. Commodities, which are dominated by energy products such as oil, also tend to perform well during crash periods, such as in 2022 when the Russian invasion of Ukraine caused oil and gas prices to soar.

Finally, traditional currency markets such as the US dollar and Japanese yen perform well during equity drawdowns. Since its introduction, the euro has not been such a good safe haven as the other two currencies, but it outperformed in the last drawdown caused by the Trump tariffs. A stealth erosion of international USD reserve holdings has been ongoing for the last decade.

Taking a diversified approach

In conclusion, investors who are not able to predict the nature of the next crisis may need to take a diversified approach toward safe-haven assets. Since US Treasuries have gone from safe haven to stormy waters, German Bunds, defensive equities, gold, commodities, and fiat currencies may offer better protection during the next episode of market turbulence.

This article is an excerpt of a special topic in our five-year outlook.

Expected Returns 2026 - 2030

重要事項

当資料は情報提供を目的として、ロベコ・ジャパン株式会社(以下「当社」)が独自に作成、または当社のグループ会社(Robeco Institutional Asset Management B.V.およびその関連会社を含む)から提供された資料を当社が編集・翻訳したものです。資料中の個別の金融商品の売買の勧誘や推奨等を目的とするものではありません。記載された情報は十分信頼できるものであると考えておりますが、その正確性、完全性を保証するものではありません。意見や見通しはあくまで作成日における弊社の判断に基づくものであり、今後予告なしに変更されることがあります。運用状況、市場動向、意見等は、過去の一時点あるいは過去の一定期間についてのものであり、過去の実績は将来の運用成果を保証または示唆するものではありません。また、記載された投資方針・戦略等は全ての投資家の皆様に適合するとは限りません。当資料は法律、税務、会計面での助言の提供を意図するものではありません。 ご契約に際しては、必要に応じ専門家にご相談の上、最終的なご判断はお客様ご自身でなさるようお願い致します。 運用を行う資産の評価額は、組入有価証券等の価格、金融市場の相場や金利等の変動、及び組入有価証券の発行体の財務状況による信用力等の影響を受けて変動します。また、外貨建資産に投資する場合は為替変動の影響も受けます。運用によって生じた損益は、全て投資家の皆様に帰属します。したがって投資元本や一定の運用成果が保証されているものではなく、投資元本を上回る損失を被ることがあります。弊社が行う金融商品取引業に係る手数料または報酬は、締結される契約の種類や契約資産額により異なるため、当資料において記載せず別途ご提示させて頂く場合があります。具体的な手数料または報酬の金額・計算方法につきましては弊社担当者へお問合せください。 当資料及び記載されている情報、商品に関する権利は弊社に帰属します。したがって、弊社の書面による同意なくしてその全部もしくは一部を複製またはその他の方法で配布することはご遠慮ください。 商号等: ロベコ・ジャパン株式会社 金融商品取引業者 関東財務局長(金商)第2780号 加入協会: 一般社団法人 資産運用業協会