Researcher

• インサイト

Using artificial intelligence for selecting small-cap stocks

Amid an ever-changing economic environment, small-cap equities present an equity sub-asset class that historically attracted flows in global large-cap market environments. In this insight of our special topic as part of our 5-year Expected Returns, our quant researchers Tobias Hoogteijling, Vera Roersma and Matthias Hanauer talk about how small caps are coming back into the spotlight.

まとめ

- Small-cap indices represent a more diversified, cheaper universe

- Sparse analyst coverage means a fertile ground for quant

- AI and machine learning can offer alpha by capturing complex relationships

Small-cap stocks are publicly traded companies with market capitalizations typically ranging between USD 250 million and USD 10 billion.1 Small caps are an integral part of the global equity market portfolio, and many consider explicit allocation to them. “This is especially the case in today’s markets, where mega-cap tech stocks dominate large-cap indices, which also trade at elevated valuations,” says Hanauer. In contrast, small-cap indices comprise a much wider and more diversified mix of stocks, trading at a discount of approximately 20% compared to large caps.

The small-cap universe presents attractive alpha opportunities for investors who know where to find them, but also sizable challenges due to its broad and heterogeneous nature. Human analysts can only cover a limited number of names, and the more niche nature of small-cap firms makes specialization more difficult. 2

Sparse coverage means alpha opportunities

For example, on average, each small-cap stock is currently covered by about eight analysts, compared to 19 for large-cap stocks.3 Although fundamental managers might struggle to cover the investable small-cap universe, it fits naturally into a quantitative approach, as the cost of developing a quantitative model does not increase with the investable universe’s size. Conversely, as Roersma points out, quantitative strategies actually benefit from the universe’s breadth, from which they can systematically exploit a broad set of opportunities.

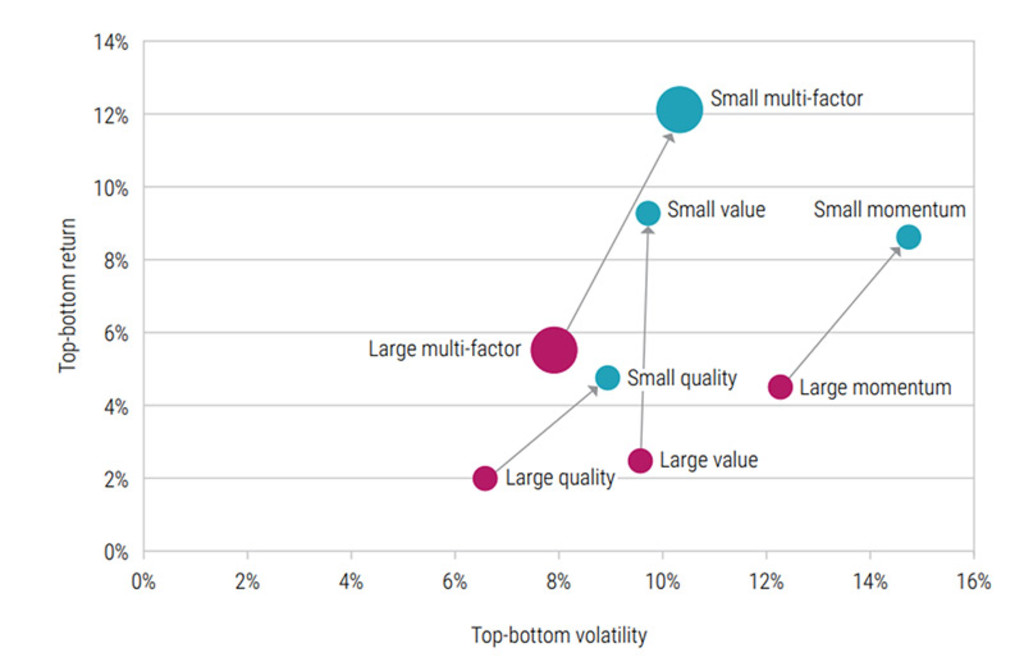

The small-cap universe’s size, diversity and complexity make it difficult for analysts and fundamental investors to cover it thoroughly. Its resulting market inefficiency and mispricing, however, can create larger opportunities to generate alpha. This greater degree of mispricing can be observed empirically, for example, by analyzing hypothetical top-minus-bottom portfolios based on well-known stock market factors such as value, momentum, and quality. Figure 1 illustrates that the annualized factor premiums and their corresponding volatilities are higher in the small-cap space than in the large-cap space.

Figure 1: Top-minus-bottom factor premiums in small-cap and large-cap space

The performance shown is hypothetical, based on theoretical models and assumptions, and is no guarantee for future results. Source: Robeco. The graph reports the annualized returns and volatilities for ‘small’ and ‘large’ cap factors. Factor returns are the return spreads between the top and bottom factor quintile portfolios. Portfolios are equal-weighted and rebalanced monthly. The investment universe consists of the constituents of the MSCI World (‘large’) and MSCI World Small Cap (‘small’) indices. The generic factors are Value (book/price, forward earnings/price), Quality (ROE, debt/assets), and Momentum (12–1 month price momentum). The composite factor is an equally weighted average of Value, Momentum, and Quality. The sample period spans from January 2000 to April 2025.

Predicting stock returns with machine learning

To model such stock market dynamics, we turn to machine learning (ML), a subcategory of AI. In this specific case, says Hoogteijling, we are interested in modeling which stocks are likely to yield high returns (and thus are potential buy candidates) and vice versa. One key advantage of ML techniques is their flexibility in capturing data patterns. In a simpler, traditional approach, one would often assume that relationships are linear. However, not all real-life relationships can be linearly approximated. ML algorithms such as random forests and neural networks4 do not impose such a strict functional form, but instead can be more freely shaped depending on the data given to the model. 5

クオンツ運用の価値を探求

最先端クオンツ戦略の情報やインサイトを定期的にお届けします。

Performance of stock selection models

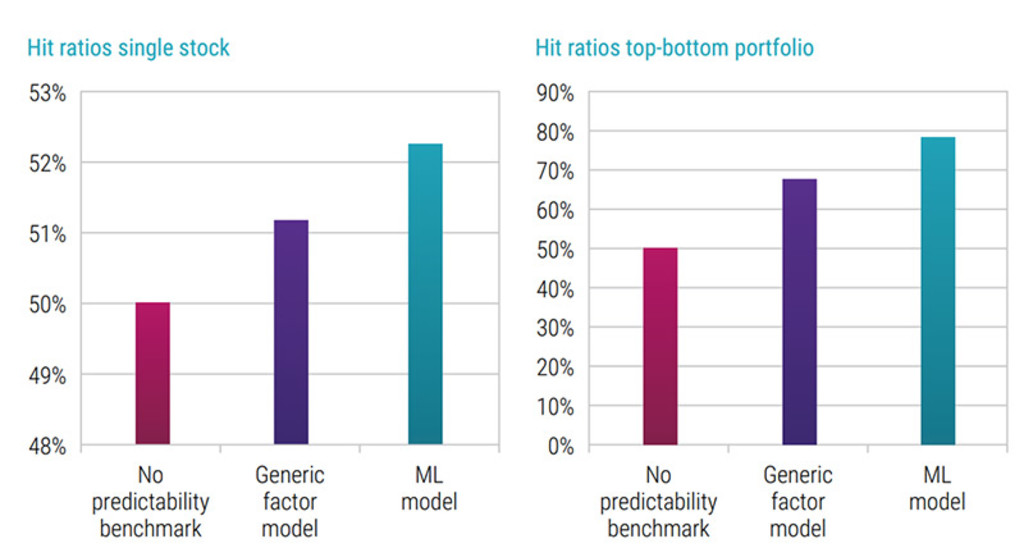

To assess the performance of these ML models – in other words, whether they can accurately predict whether stocks will outperform or underperform – we conduct a historical simulation study classifying the top and bottom half of stocks’ predicted returns. Then, we investigate to what extent the various models can correctly predict these two halves. If a model had no predictive power, about half of the stocks would be correctly predicted.

As illustrated in Figure 2, we find that both a generic factor model and an ML model outperform the ‘no predictability’ benchmark in terms of model accuracy. Furthermore, the ML model outperforms the generic value-quality-momentum factor model. Although stock-specific predictability of around 51-52% might seem low, small but consistent advantages can translate into long-term success. These stock-specific hit ratios translate into portfolio hit ratios of 68% and 78% for long-short quintile portfolios based on monthly returns, when sorted by generic and ML model predictions, respectively. These numbers highlight how even a slight improvement in predictive accuracy can lead to substantially better portfolio outcomes. 6

Figure 2: Average percentage of stocks accurately classified

The performance shown is hypothetical, based on theoretical models and assumptions, and is no guarantee for future results. Source: Robeco. The figure on the left shows the time series’ average percentage of stocks correctly classified as being in the top half or bottom half of stocks in terms of next month returns, in a historical simulation study. The figure on the right shows the hit ratio of monthly long-short quantile portfolio returns, sorted based on predicted returns. The considered universes are the constituents of the MSCI World Small Cap Index over the period December 2000 to April 2025. The generic factor model consists of generic Value (book/price and forward earnings/price), Quality (ROE and debt/assets) and Momentum (12-1 month price momentum) factors.

Conclusion

In recent years, AI has shifted from hype to practical application, with machine learning in particular showing real promise for quantitative investing. Small-cap equities, with their breadth, inefficiencies, and limited coverage, offer especially fertile ground for these techniques.

Yet, as Hoogteijling explains, AI is not a silver bullet: success depends on careful model selection, interpretation, and explainability. When used with skill and discipline, however, machine learning can be a powerful addition to the quant investor’s toolkit, and a source of enduring edge in small-cap markets.

This article is an excerpt of a special topic in our five-year outlook.

Footnotes

1 As of the end of April 2025, based on the market capitalization numbers for the constituents of the MSCI World Small Cap Index, winsorized at the top and bottom 2.5%.

2 As of the end of April 2025, based on four bottom-up-calculated multiples (price-to-book, forward price-to-earnings, price-to-earnings, and price-to-dividend) for the MSCI World and MSCI World Small Cap indices.

3 Source: IBES.

4 A neural network is a type of ML model that learns to recognize patterns, inspired by how the human brain processes information. A random forest is a group of simple decision-making models (called decision trees) that work together to make more accurate choices than just one tree on its own.

5 For a broader view of the different applications of ML in asset management, we refer to Blitz et al. (2023) and Chen and Zhou (2023).

6 The performance shown is hypothetical, based on theoretical models and assumptions, and is no guarantee for future results.

Expected Returns 2026 - 2030

重要事項

当資料は情報提供を目的として、ロベコ・ジャパン株式会社(以下「当社」)が独自に作成、または当社のグループ会社(Robeco Institutional Asset Management B.V.およびその関連会社を含む)から提供された資料を当社が編集・翻訳したものです。資料中の個別の金融商品の売買の勧誘や推奨等を目的とするものではありません。記載された情報は十分信頼できるものであると考えておりますが、その正確性、完全性を保証するものではありません。意見や見通しはあくまで作成日における弊社の判断に基づくものであり、今後予告なしに変更されることがあります。運用状況、市場動向、意見等は、過去の一時点あるいは過去の一定期間についてのものであり、過去の実績は将来の運用成果を保証または示唆するものではありません。また、記載された投資方針・戦略等は全ての投資家の皆様に適合するとは限りません。当資料は法律、税務、会計面での助言の提供を意図するものではありません。 ご契約に際しては、必要に応じ専門家にご相談の上、最終的なご判断はお客様ご自身でなさるようお願い致します。 運用を行う資産の評価額は、組入有価証券等の価格、金融市場の相場や金利等の変動、及び組入有価証券の発行体の財務状況による信用力等の影響を受けて変動します。また、外貨建資産に投資する場合は為替変動の影響も受けます。運用によって生じた損益は、全て投資家の皆様に帰属します。したがって投資元本や一定の運用成果が保証されているものではなく、投資元本を上回る損失を被ることがあります。弊社が行う金融商品取引業に係る手数料または報酬は、締結される契約の種類や契約資産額により異なるため、当資料において記載せず別途ご提示させて頂く場合があります。具体的な手数料または報酬の金額・計算方法につきましては弊社担当者へお問合せください。 当資料及び記載されている情報、商品に関する権利は弊社に帰属します。したがって、弊社の書面による同意なくしてその全部もしくは一部を複製またはその他の方法で配布することはご遠慮ください。 商号等: ロベコ・ジャパン株式会社 金融商品取引業者 関東財務局長(金商)第2780号 加入協会: 一般社団法人 資産運用業協会