Head of Exchange Traded Funds

• インサイト

Six must-knows about active ETFs

Exchange-traded funds (ETFs) have rapidly become one of the most popular investment vehicles globally, thanks to their flexibility, transparency, and efficiency. Initially launched in the 1990s as a cost-effective way to gain passive exposure to market indices like the S&P 500, ETFs have since expanded significantly in scope and complexity.

Active ETFs, in particular, have emerged as a compelling option, blending the benefits of active investment management, such as the potential for superior returns, with the structural advantages of ETFs, including intraday tradability and enhanced liquidity.

Despite their increasing popularity, active ETFs are still sometimes less well understood than their mutual fund counterparts, and may face misconceptions stemming from their passive heritage. Investors exploring active ETFs often raise key questions about how these products function, their value proposition, and their potential role within a diversified investment portfolio. In this insight, we address some questions, clarifying how active ETFs work, their benefits, and how they can complement traditional investment vehicles.

Not anymore. Many investors still equate ETFs solely with passive strategies, largely due to their origin as index-tracking vehicles. Originally, ETFs were designed as exchange-traded products that could track major market indices and trade throughout the day like stocks. This innovation combined the broad exposure of mutual funds with the liquidity of listed securities, making ETFs an efficient tool for accessing market beta at low cost.

Passive ETFs became synonymous with low-cost, straightforward exposure to broad market indices. However, it's important to recognize that an ETF is fundamentally a wrapper – a versatile investment structure capable of and designed to house various investment strategies.

Active ETFs utilize the same ETF structure but differ significantly in their underlying investment approach. Unlike passive ETFs, active ETFs house active strategies: in other words, they reflect the deliberate investment decisions made by portfolio managers and/or advanced quantitative models. Like other active strategies, this approach aims to outperform standard benchmarks or manage specific risks more effectively. Consequently, active ETFs maintain the convenience, transparency, and intraday trading of passive ETFs, but add the potential benefits derived from active management insights.

2. Have active ETFs gained traction in Europe?

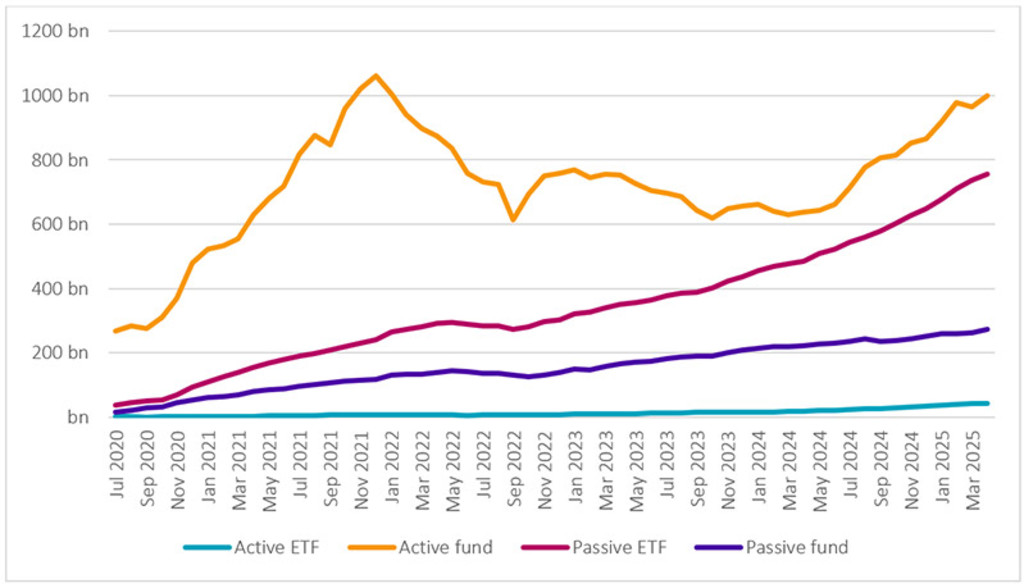

Although ETFs were pioneered and popularized in the US, the assumption that active ETFs remain primarily a US phenomenon is outdated. While the US market indeed remains larger and more mature, active ETFs are gaining significant momentum across Europe. Figure 1 below shows the growth of passive and active ETFs versus other funds over the last five years in the US, while Figure 2 shows the growth of their European counterparts.

Figure 1 | Passive and active flows in the US 2020-2025

Source: Broadridge

The European market for active ETFs is experiencing robust growth, driven by evolving regulatory frameworks, increasing demand from institutional investors and wholesale distributors, and growing investor education and awareness. Recent trends indicate, as can be seen in Figure 2 below, that European investors are increasingly appreciating the structural advantages of active ETFs, including enhanced transparency, liquidity, and the potential for alpha generation through active strategies. Rather than being a niche product, active ETFs in Europe now represent a vibrant and expanding segment of the investment landscape, with the proportion of investors allocating to active ETFs at 50% versus 21% a year ago.1 It’s increasingly clear that active ETFs offer substantial opportunities to investors who understand their potential.

Figure 2 | European and international passive and active flows 2020-2025

Source: Broadridge

3. Are active ETFs really active?

A common concern about active ETFs is whether they are truly active in their approach, or simply repackaged versions of passive strategies. Thanks to the evolution of ETF product design, the boundary between active and passive is becoming increasingly nuanced. Semi-transparent ETFs, rules-based strategies, or highly customized indices can all blur traditional definitions, actually providing more opportunities for investors.

At Robeco, we define active ETFs as those grounded in genuine active strategies designed to generate excess returns by responding to market signals, rather than simply mirroring a benchmark. This brings us to a related concern: do active ETFs inherently carry higher risk simply because they deviate from an index?

While active ETFs do diverge from index-based strategies, this divergence does not automatically translate into greater risk. In fact, they often provide enhanced diversification and better risk management compared with certain passive strategies, especially when benchmark indices become highly concentrated in a few megacap stocks.

For example, indices such as the S&P 500 can leave investors disproportionately exposed to the Magnificent Seven. Active ETFs employ comprehensive risk management frameworks and sophisticated analytical tools to mitigate such concentration risks. They can therefore deliver broader diversification and potentially lower volatility, aligning investment risk more effectively with investor objectives.

4. Can active ETFs really outperform after fees?

A common perception is that active managers rarely outperform their benchmarks after fees. So what about active ETFs? While this may be true for some traditional mutual funds, Robeco’s active ETFs are built on time-tested strategies with long track records of generating alpha net of costs. Our strategies are systematic and cost-disciplined, with careful attention paid to turnover and transaction efficiency.

Active ETFs provide enhanced transparency around costs compared to traditional mutual funds, making it easier for investors to clearly understand what they are paying for – namely, the intellectual property and strategic insights of the underlying investment approach, not the ETF wrapper itself. In other words, investors are primarily paying for the quality and effectiveness of the investment strategy embedded within the ETF. As a result, active ETFs offer investors cost-effective access to sophisticated active management insights.

By embedding active insights into a transparent, scalable ETF format, we aim to deliver strong performance relative to fees – not just activity for its own sake. Each strategy should be evaluated on its own merits, particularly the robustness of the investment process and the price being charged.

5. Are active ETFs less liquid than passive ETFs?

Investors often worry about liquidity in active ETFs, especially newer or smaller funds that show lower secondary-market trading volumes. However, ETF liquidity involves more than just visible trading volumes.

ETFs benefit from two layers of liquidity. Firstly, liquidity is derived from the ETF’s underlying holdings: stocks, bonds, or other assets the ETF owns. Secondly, ETFs themselves are tradable securities on secondary markets. Even when an ETF shows low daily trading volumes, authorized market participants (such as institutional trading desks) continuously facilitate liquidity by creating and redeeming ETF shares based on investor demand, enabling investors to trade instantly at quoted prices.

Consequently, the liquidity of an ETF is primarily determined by the liquidity of its underlying assets. This mechanism ensures that active ETFs remain as liquid as their underlying investments, regardless of their trading volume on exchanges.

6. Are ETFs primarily for short-term, tactical trading?

The ability to trade ETFs intraday, similar to stocks, often leads investors to assume ETFs cater mainly to short-term, tactical trading strategies. However, intraday liquidity provides flexibility rather than prescribing short-term use.

ETFs are equally effective for long-term strategic allocation purposes. Investors can use intraday liquidity to enter or exit investments precisely when desired, a significant advantage during volatile market conditions or specific events. Yet, this does not necessitate frequent trading. Active ETFs in particular lend themselves well to both strategic and tactical investment approaches, offering investors a versatile tool that can adapt to various investment horizons – whether immediate, medium-term, or as a core component of long-term portfolio strategies.

Conclusion

Active ETFs represent an essential evolution in the investment landscape. Combining the structural efficiency, liquidity, and transparency of traditional ETFs with active management’s potential for superior returns and risk management, active ETFs offer compelling advantages for investors seeking enhanced portfolio solutions. By grasping the basics and understanding the nuances, investors can confidently integrate active ETFs into their diversified portfolios.

At Robeco, our commitment to innovation and rigorous investment discipline positions our active ETFs as valuable, reliable tools – built on well-established strategies – for achieving investor objectives, now and in the future.

Footnote

1 According to market research conducted by Research in Finance, see ‘Active ETFs adopted by half of European fund buyers: research’ July 2025 (igniteseurope.com).

クオンツ運用の価値を探求

最先端クオンツ戦略の情報やインサイトを定期的にお届けします。

重要事項

当資料は情報提供を目的として、ロベコ・ジャパン株式会社(以下「当社」)が独自に作成、または当社のグループ会社(Robeco Institutional Asset Management B.V.およびその関連会社を含む)から提供された資料を当社が編集・翻訳したものです。資料中の個別の金融商品の売買の勧誘や推奨等を目的とするものではありません。記載された情報は十分信頼できるものであると考えておりますが、その正確性、完全性を保証するものではありません。意見や見通しはあくまで作成日における弊社の判断に基づくものであり、今後予告なしに変更されることがあります。運用状況、市場動向、意見等は、過去の一時点あるいは過去の一定期間についてのものであり、過去の実績は将来の運用成果を保証または示唆するものではありません。また、記載された投資方針・戦略等は全ての投資家の皆様に適合するとは限りません。当資料は法律、税務、会計面での助言の提供を意図するものではありません。 ご契約に際しては、必要に応じ専門家にご相談の上、最終的なご判断はお客様ご自身でなさるようお願い致します。 運用を行う資産の評価額は、組入有価証券等の価格、金融市場の相場や金利等の変動、及び組入有価証券の発行体の財務状況による信用力等の影響を受けて変動します。また、外貨建資産に投資する場合は為替変動の影響も受けます。運用によって生じた損益は、全て投資家の皆様に帰属します。したがって投資元本や一定の運用成果が保証されているものではなく、投資元本を上回る損失を被ることがあります。弊社が行う金融商品取引業に係る手数料または報酬は、締結される契約の種類や契約資産額により異なるため、当資料において記載せず別途ご提示させて頂く場合があります。具体的な手数料または報酬の金額・計算方法につきましては弊社担当者へお問合せください。 当資料及び記載されている情報、商品に関する権利は弊社に帰属します。したがって、弊社の書面による同意なくしてその全部もしくは一部を複製またはその他の方法で配布することはご遠慮ください。 商号等: ロベコ・ジャパン株式会社 金融商品取引業者 関東財務局長(金商)第2780号 加入協会: 一般社団法人 資産運用業協会