Strategist

獲取最新市場觀點

訂閱我們的電子報,時刻把握投資資訊和專家分析。

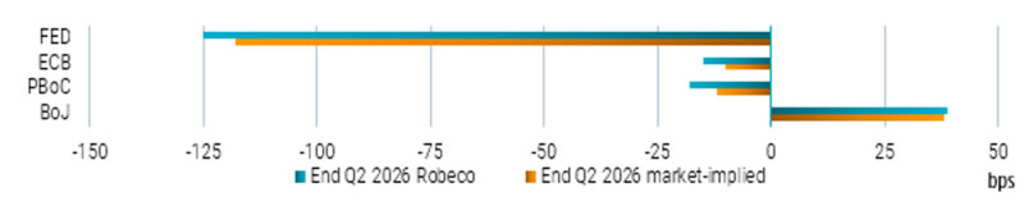

In this edition of the Central Bank Watcher, we explore what’s next for the Fed, ECB, PBoC, and BoJ, and how shifting policy trajectories are shaping yield curves worldwide.

There is a long-standing market belief that the ECB tends to follow the Fed with a delay. However, this assumption has proven inaccurate over the past 18 months. In fact, the ECB has been ahead of the Fed in easing monetary policy and has already returned to a neutral stance.

We suspect the Fed will soon follow the lead of the ECB on a rate-cutting path toward neutrality. Indeed, following the recent slowdown in job growth and significant downward revisions, expectations for rate cuts resuming on 17 September have now become the consensus. Nonetheless, we believe the Fed will be constrained in its ability to go ‘all-in’ on easing, given the inflation side of their mandate and despite the seemingly relentless political pressure. Historically, central banks that have yielded to pressure from their country’s leader on interest rate decisions have often faced the consequence of elevated inflation.

The ECB seems to be entering a prolonged pause in their rate cycle. In the press conference after the September ECB meeting President Lagarde expressed an optimistic view on economic conditions in the euro area, while signaling an end to the disinflation phase.

In China, the PBoC recently indicated a preference for holding rates steady. However, persistent issues in local government finances and the real estate sector, ongoing trade tensions, and the potential for a slowdown in credit growth suggest the PBoC’s rate-cutting cycle may not yet be complete.

In regards to the Bank of Japan, we are more hawkish relative to markets, mainly due to the fact that we believe the BoJ can increase its policy rate earlier than the market expects.

Source: Bloomberg, Robeco, based on money market futures and forwards, 12 September 2025

訂閱我們的電子報,時刻把握投資資訊和專家分析。

The contents of this document have not been reviewed by the Securities and Futures Commission ("SFC") in Hong Kong. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice. This document has been distributed by Robeco Hong Kong Limited (‘Robeco’). Robeco is regulated by the SFC in Hong Kong. This document has been prepared on a confidential basis solely for the recipient and is for information purposes only. Any reproduction or distribution of this documentation, in whole or in part, or the disclosure of its contents, without the prior written consent of Robeco, is prohibited. By accepting this documentation, the recipient agrees to the foregoing This document is intended to provide the reader with information on Robeco’s specific capabilities, but does not constitute a recommendation to buy or sell certain securities or investment products. Investment decisions should only be based on the relevant prospectus and on thorough financial, fiscal and legal advice. Please refer to the relevant offering documents for details including the risk factors before making any investment decisions. The contents of this document are based upon sources of information believed to be reliable. This document is not intended for distribution to or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Investment Involves risks. Historical returns are provided for illustrative purposes only and do not necessarily reflect Robeco’s expectations for the future. The value of your investments may fluctuate. Past performance is no indication of current or future performance.