Client Portfolio Manager

新興国がもたらす機会とは?

新興国の投資機会を深掘りするニュースレター(英文)に登録しましょう。

With key inputs for AI infrastructure and renewable energy primarily found within emerging economies in Latin America, Africa and Asia-Pacific, we think EM investors will be beneficiaries of the global race for resources.

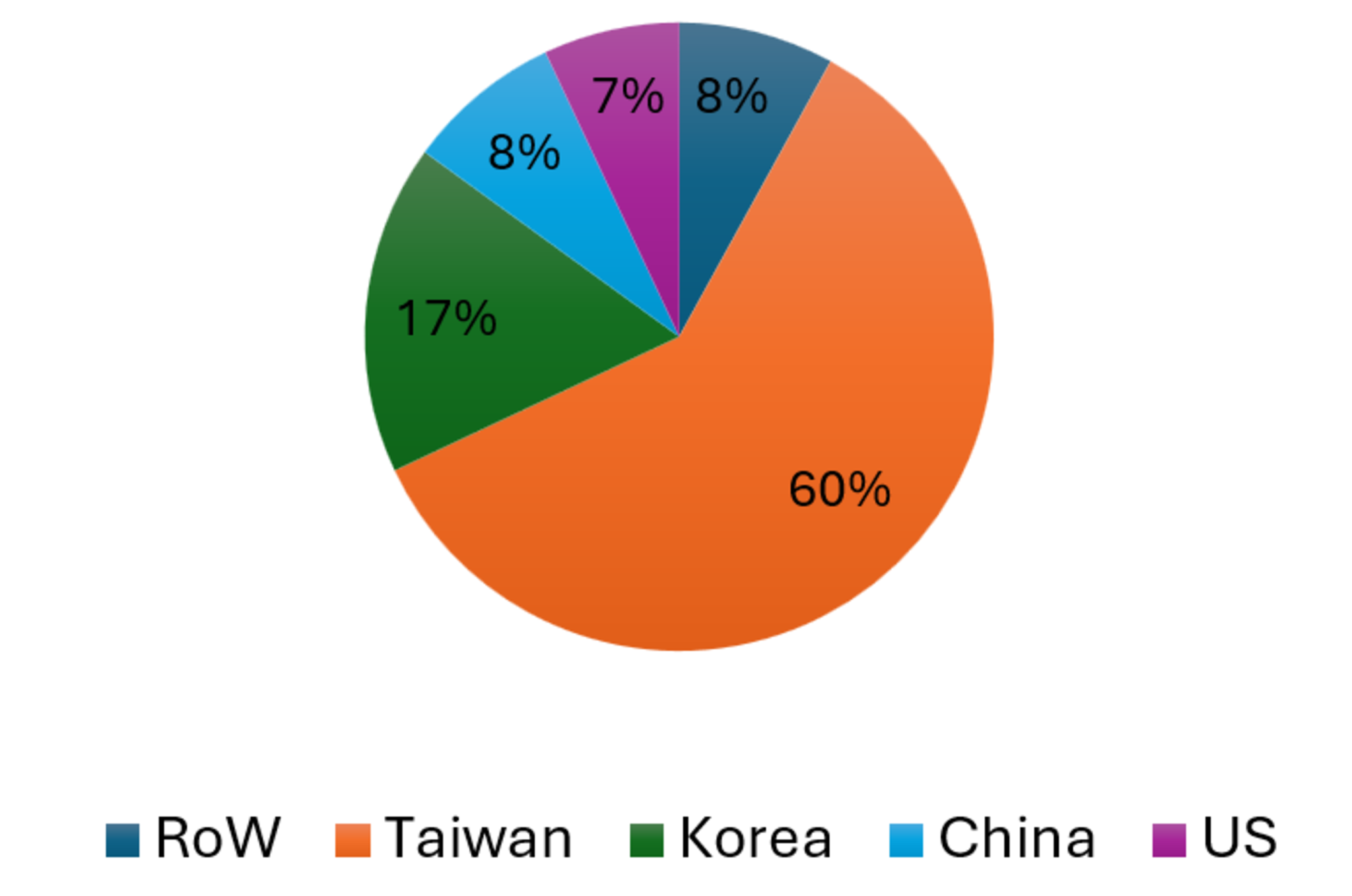

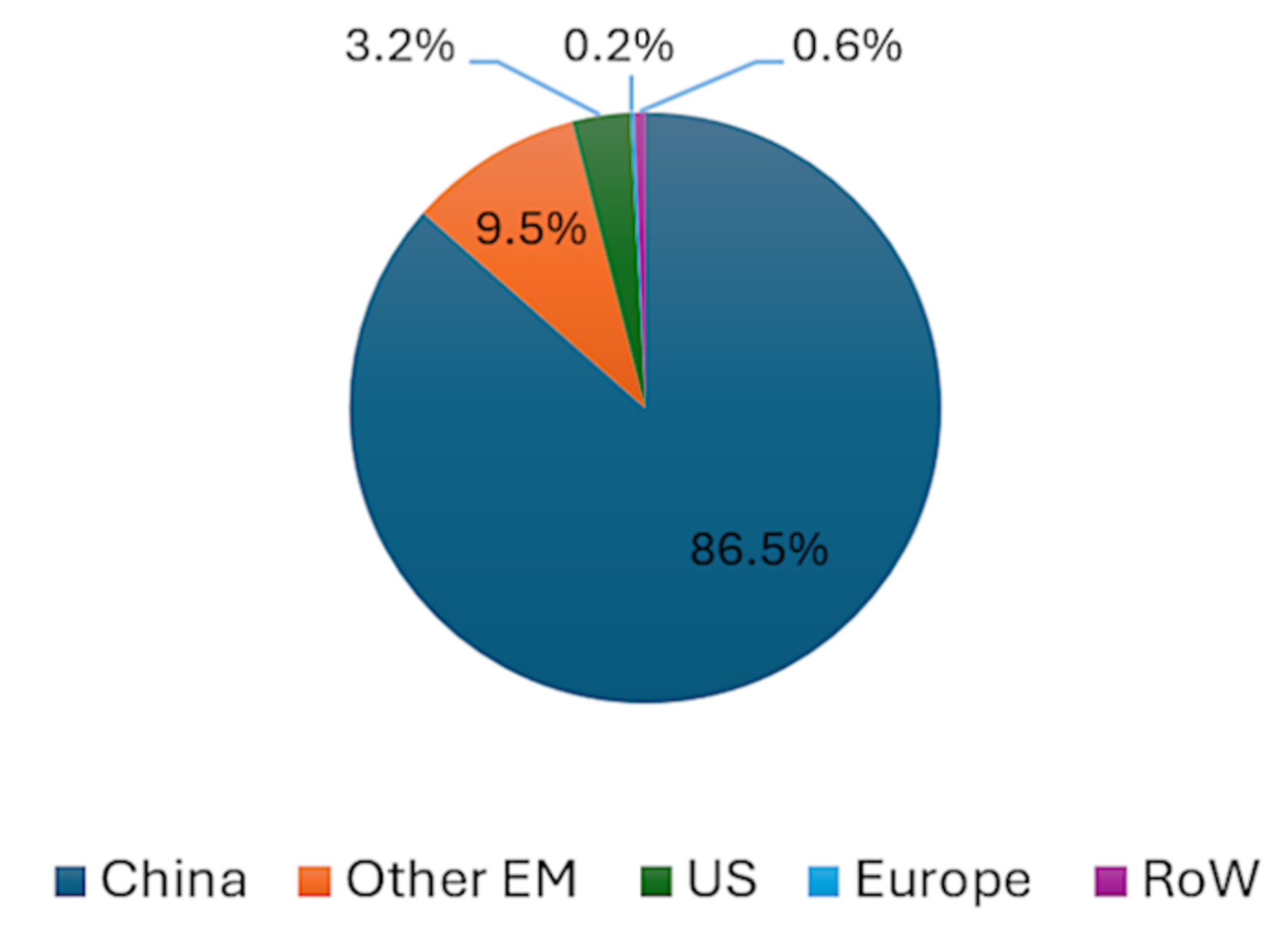

Emerging markets have moved into leadership positions in key technologies supporting the AI buildout, like semiconductor manufacturing (see Figure 1a), and the development and manufacture of renewable energy technologies like solar panels (see Figure 1b).

Source: TrendForce/Visual Capitalist (2024-2025 Estimates)

Source: StatRanker. PV module production for 2024

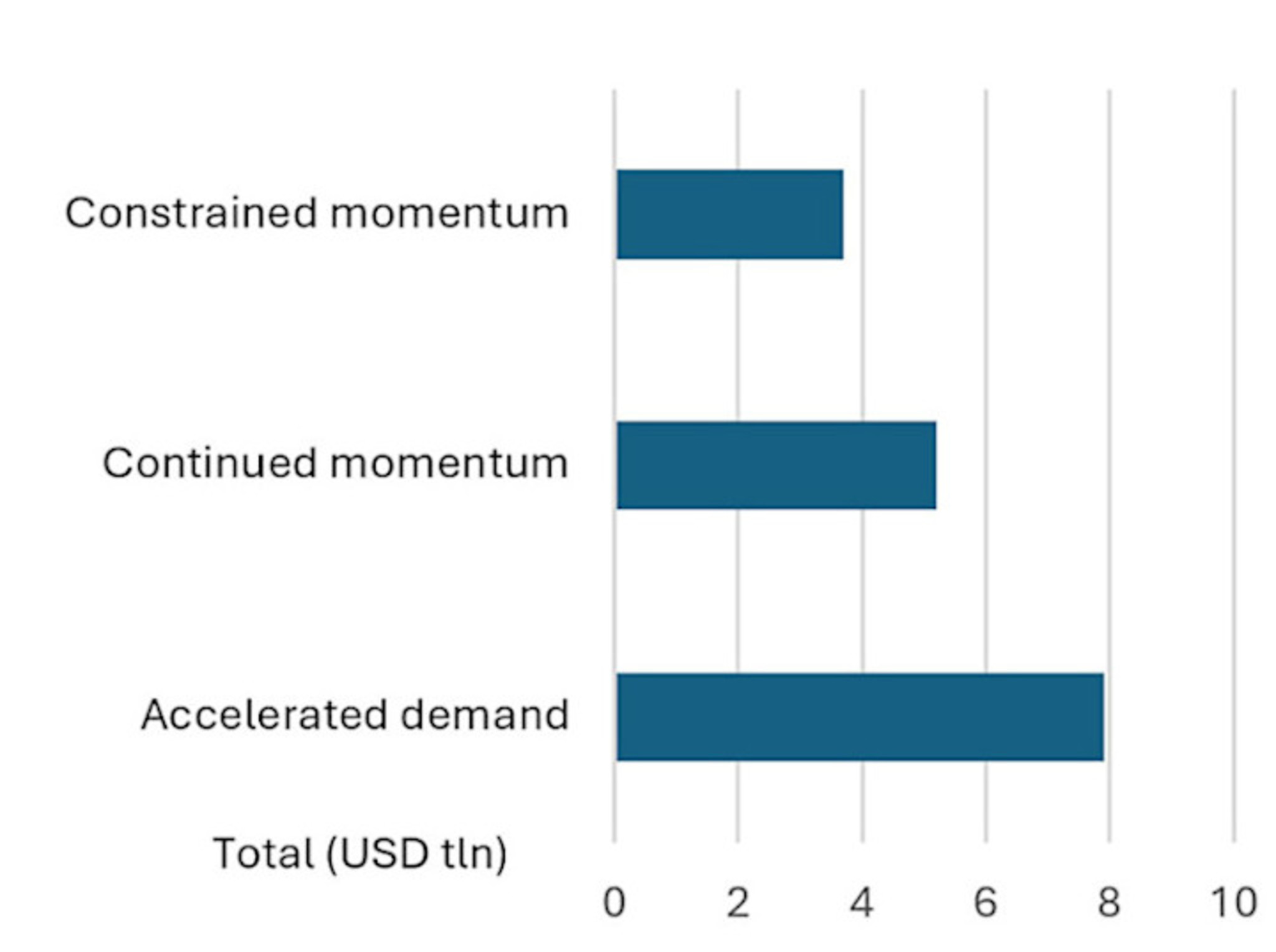

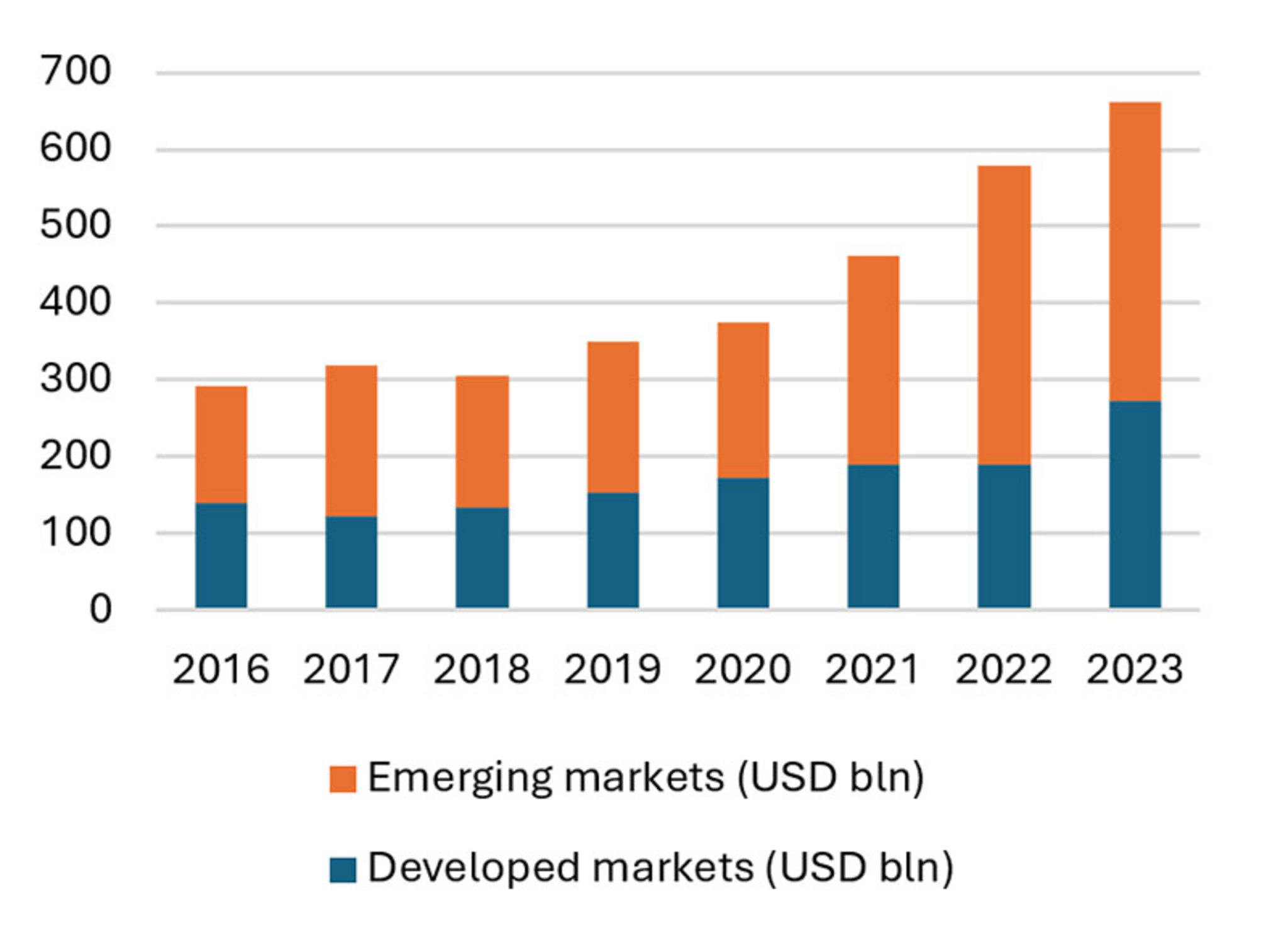

Both of these sectors are attracting vast amounts of capital expenditure in both developed and emerging markets, as Figures 2a and 2b show.

Source: McKinsey projections from April 2025 encompassing data center infrastructure, related IT equipment, and power generation capex to support data centers.

Source: BloombergNEF, Climate Investment Funds, World Bank, March 2025.

The two sectors are also inextricably linked. The AI revolution is contributing to rising electricity demand, which is in turn increasing demand for power generation sources, whether via fossil fuels, nuclear or renewables. The sudden jump in oil and LNG prices sparked by the Iran war in March 2026 has also illustrated the fragility of fossil fuel supply chains and is likely to further accelerate global investment in renewables, electrification and efficiency.

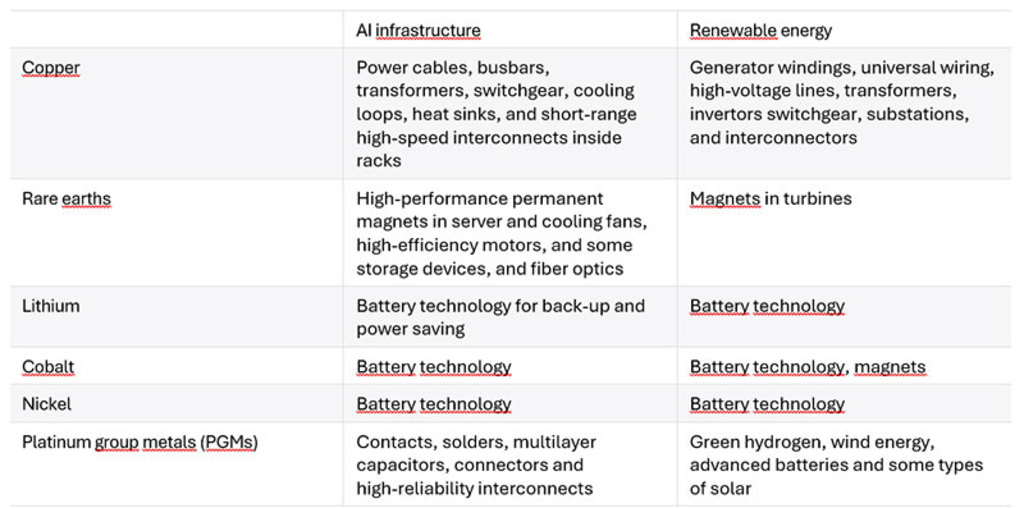

Moreover, the two trends are relying on many of the same mineral inputs to enable the infrastructure buildout (see Table 1), resulting in a surge in demand for these specific materials.

Sources: IEA, UN Task Force on Critical Energy Transition Minerals – December 2025, Artificial Intelligence and the Critical Minerals Crunch – FP Analytics, October 2025.

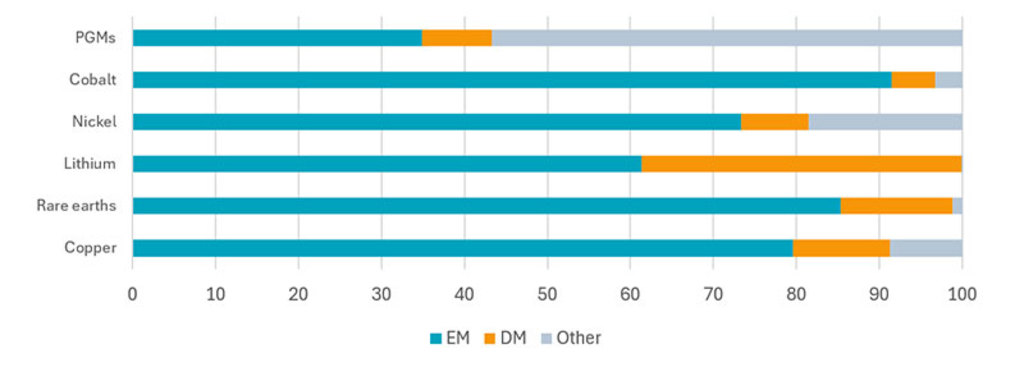

Of these key minerals, critical to both AI and the energy transition, a significant share of economically viable reserves and production is concentrated in emerging economies (see Figure 3).

Sources: IEA (2025), Global Critical Minerals Outlook 2025, IEA, Paris www.iea.org/reports/global-critical-minerals-outlook-2025, Licence: CC BY 4.0. ‘Other’ includes Russia and disputed resources

For example, South Africa remains the most reliable global source of PGMs. Chile, Zambia, Indonesia and the Democratic Republic of the Congo (DRC) supply the balance of global copper, while China dominates in rare earths mining and especially in processing. Indonesia is also the swing supplier in nickel, and the DRC dominates cobalt mining. The world’s largest lithium miner is a developed market (Australia), but the rest is produced in Chile, Argentina, China, and various African nations.

The location of these minerals has been given particular significance by the geopolitical tension between the US and China. Trade relations are worsening and the two global powers have established rival technology and military-industrial stacks. In particular, China has built a dominant position in metals and rare earths processing, outcompeting the steel and smelting sectors in the US and Europe, and leaving them dependent on China for the balance of refined supply in many key industrial inputs. This in turn has seen the US classify its mineral supply chain as a national security policy priority,1 rather than an issue that can be left to market forces.

In our view, this new environment is likely to elevate the value of emerging markets’ generous mineral endowment and also give emerging economies more leverage to capture value.

1 New Executive Order Ties U.S. Critical Minerals Security to Global Partnerships - Center for Strategic & International Studies – 15 January 2026

新興国の投資機会を深掘りするニュースレター(英文)に登録しましょう。

当資料は情報提供を目的として、ロベコ・ジャパン株式会社(以下「当社」)が独自に作成、または当社のグループ会社(Robeco Institutional Asset Management B.V.およびその関連会社を含む)から提供された資料を当社が編集・翻訳したものです。資料中の個別の金融商品の売買の勧誘や推奨等を目的とするものではありません。記載された情報は十分信頼できるものであると考えておりますが、その正確性、完全性を保証するものではありません。意見や見通しはあくまで作成日における弊社の判断に基づくものであり、今後予告なしに変更されることがあります。運用状況、市場動向、意見等は、過去の一時点あるいは過去の一定期間についてのものであり、過去の実績は将来の運用成果を保証または示唆するものではありません。また、記載された投資方針・戦略等は全ての投資家の皆様に適合するとは限りません。当資料は法律、税務、会計面での助言の提供を意図するものではありません。 ご契約に際しては、必要に応じ専門家にご相談の上、最終的なご判断はお客様ご自身でなさるようお願い致します。 運用を行う資産の評価額は、組入有価証券等の価格、金融市場の相場や金利等の変動、及び組入有価証券の発行体の財務状況による信用力等の影響を受けて変動します。また、外貨建資産に投資する場合は為替変動の影響も受けます。運用によって生じた損益は、全て投資家の皆様に帰属します。したがって投資元本や一定の運用成果が保証されているものではなく、投資元本を上回る損失を被ることがあります。弊社が行う金融商品取引業に係る手数料または報酬は、締結される契約の種類や契約資産額により異なるため、当資料において記載せず別途ご提示させて頂く場合があります。具体的な手数料または報酬の金額・計算方法につきましては弊社担当者へお問合せください。 当資料及び記載されている情報、商品に関する権利は弊社に帰属します。したがって、弊社の書面による同意なくしてその全部もしくは一部を複製またはその他の方法で配布することはご遠慮ください。 商号等: ロベコ・ジャパン株式会社 金融商品取引業者 関東財務局長(金商)第2780号 加入協会: 一般社団法人 資産運用業協会

重要なお知らせ 当社や当社役職員を装ったSNSアカウントやウェブサイト等を使った投資勧誘にご注意ください さらに表示