インデックス責任者

• インサイト

A liquid alternative to private equity investments

Private equity has become one of the fastest-growing asset classes, but it remains costly and illiquid. Can investors capture its return potential through listed markets instead? In new research, Joop Huij and Georgi Kyosev suggest that replicating private equity exposures in public equities offers a compelling liquid alternative.

執筆者

PhD, Portfolio Manager Sustainable Index Solutions

主なキーワード

まとめ

- Private equity has historically delivered strong returns, but comes with challenges.

- Factor exposures explain much of private equity’s performance

- Robeco’s liquid alternative delivers private equity-like returns with greater flexibility

Over the past decade, private equity assets under management have surged from USD 2 trillion in 2014 to more than USD 9 trillion by mid-2024. Pension funds and endowments have raised allocations significantly, inspired by models such as Yale’s, where exposure to venture capital, buyouts, and private real estate often reaches 29%.

The two dominant strategies are leveraged buyouts and venture capital. Buyouts focus on smaller firms at attractive valuations, often highly leveraged and with profitability challenges. Venture capital backs young, high-growth firms with substantial R&D spending, typically at higher valuations.

Private equity investors generally enjoy closer alignment with management than public shareholders, Huij and Kyosev explain, reducing agency costs such as excessive pay or empire building. This alignment, combined with the ability to restructure companies and implement operational improvements, explains much of private equity’s appeal.

Returns and challenges

Private equity has delivered annualized returns of around 15% since 1991, a premium of roughly 6% compared to global public markets. Buyout strategies saw peaks of 8% in the late 1990s and mid-2000s, while venture capital delivered annual premiums as high as 25% before the dotcom crash. Beyond returns, diversification benefits stem from leverage, strategic barriers to entry, and active ownership.

However, as Huij and Kyosev point out, investors must contend with several challenges:

Dry powder: Committed but undeployed capital still incurs fees.

High costs: Management fees of around 2% and performance carry of 20% are common.

Liquidity constraints: Exits through IPOs or private sales are uncertain and time-consuming.

Sustainability data gaps: Limited reporting makes it difficult to track portfolio-level impact.

最新のインサイトを受け取る

投資に関する最新情報や専門家の分析を盛り込んだニュースレター(英文)を定期的にお届けします。

Can public markets replicate private equity?

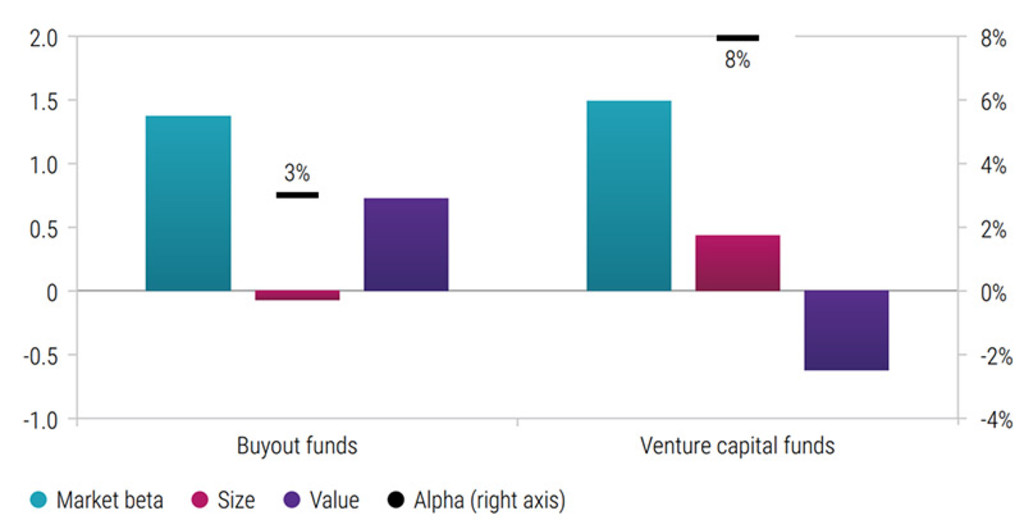

Extensive research suggests that private equity returns largely reflect exposure to public equity factors. Buyout funds typically show high market beta and a tilt toward value, while venture capital exhibits high market exposure and a strong growth tilt.

Even after adjusting for factor exposures, residual alpha remains – about 3% annually for buyouts and 8% for venture capital. Nonetheless, Huij and Kyosev argue that replication strategies targeting these exposures in public equities can approximate private equity-like returns, with the added benefits of liquidity, lower costs, and transparency.

Figure 1: Exposures of private equity

Past performance is no guarantee for future returns. The value of your investment may fluctuate. Source: Robeco (June 2025 and Ang et al (2014).

Robeco’s liquid alternative

Building on its systematic investing expertise and active ownership capabilities, Robeco has developed a liquid strategy to replicate private equity characteristics in public equities. The process involves first defining the universe, starting with over 10,000 companies, screened for liquidity. Then factor tilts are applied. Buyout proxies emphasize leverage and share buybacks, while venture capital proxies focus on earnings growth and R&D.

Portfolio construction follows, during which weights are optimized to mirror private equity exposures. Sustainability is integrated by applying proprietary SDG scores and engagement insights to improve governance and climate alignment.

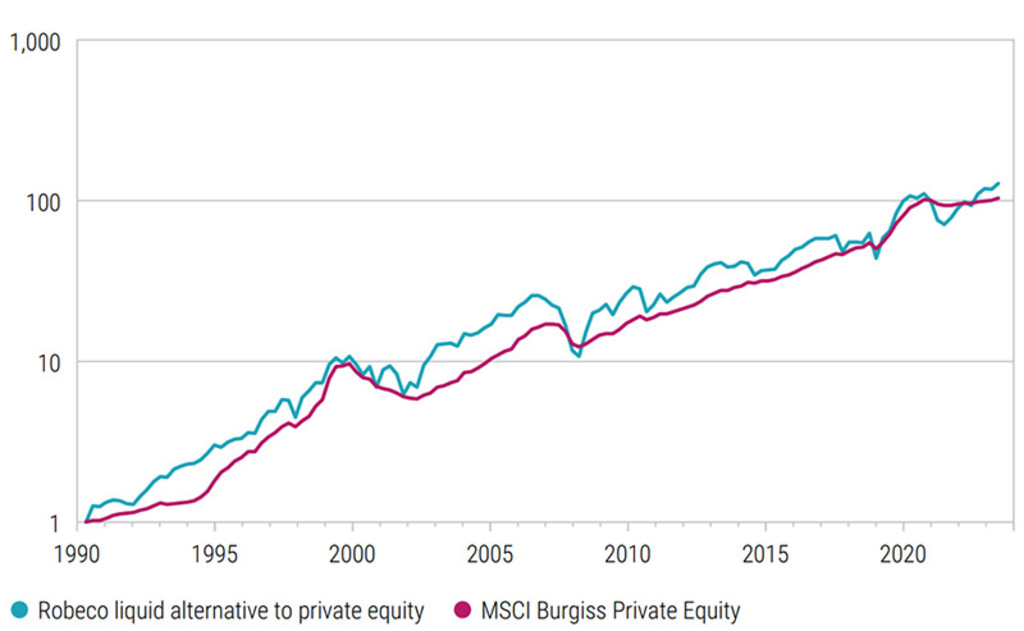

As Huij and Kyosev demonstrate, this systematic approach has delivered simulated performance broadly in line with the MSCI Burgiss private equity benchmark. While reported private equity returns appear smoother due to infrequent NAV updates, research shows that ‘unsmoothed’ results exhibit volatilities closer to those of Robeco’s replicating strategy.

Figure 2: Cumulative returns in portfolio simulations

Simulated past performance is no guarantee of future results. For illustrative purposes only. Source: Robeco, based on portfolio simulation, cumulative return in USD, gross dividends reinvested, Developed markets, Q1 1991-Q3 2024, logarithmic scale. MSCI Burgiss returns are based on MSCI Global Private Equity Closed-End Fund Index (Unfrozen; USD). The performance shown is based on a simulated and hypothetical (back-tested) data and may suffer from the benefit of hindsight. Although Robeco is prudent in its assumptions for simulations, no representation is made that the index will achieve results similar to those shown and actual performance results may deviate significantly.

Sustainability and engagement benefits

Public markets provide a broad investment pool and rich sustainability data, enabling portfolios to be tilted toward positive SDG alignment while underweighting negatively scored companies. This aligns particularly well with venture-style exposure to innovative firms.

Robeco’s strategy also emphasizes active ownership. Engagement with portfolio companies addresses sustainability, governance, and human capital – reflecting the close involvement typical in private equity but applied within listed markets.

Conclusion

Private equity offers attractive return potential but is costly, illiquid, and often lacking in sustainability transparency. Replication in public equities enables investors to capture much of the premium while improving liquidity, lowering fees, and integrating sustainability.

Robeco’s innovative research aims to capture the full alpha by combining academic knowledge, portfolio construction expertise, and proprietary voting and engagement data. The goal is to deliver private equity-like returns but with the benefits of public equity – high liquidity, lower costs, and sustainability integration.

This article is an excerpt of a special topic in our five-year outlook.

Expected Returns 2026 - 2030

重要事項

当資料は情報提供を目的として、ロベコ・ジャパン株式会社(以下「当社」)が独自に作成、または当社のグループ会社(Robeco Institutional Asset Management B.V.およびその関連会社を含む)から提供された資料を当社が編集・翻訳したものです。資料中の個別の金融商品の売買の勧誘や推奨等を目的とするものではありません。記載された情報は十分信頼できるものであると考えておりますが、その正確性、完全性を保証するものではありません。意見や見通しはあくまで作成日における弊社の判断に基づくものであり、今後予告なしに変更されることがあります。運用状況、市場動向、意見等は、過去の一時点あるいは過去の一定期間についてのものであり、過去の実績は将来の運用成果を保証または示唆するものではありません。また、記載された投資方針・戦略等は全ての投資家の皆様に適合するとは限りません。当資料は法律、税務、会計面での助言の提供を意図するものではありません。 ご契約に際しては、必要に応じ専門家にご相談の上、最終的なご判断はお客様ご自身でなさるようお願い致します。 運用を行う資産の評価額は、組入有価証券等の価格、金融市場の相場や金利等の変動、及び組入有価証券の発行体の財務状況による信用力等の影響を受けて変動します。また、外貨建資産に投資する場合は為替変動の影響も受けます。運用によって生じた損益は、全て投資家の皆様に帰属します。したがって投資元本や一定の運用成果が保証されているものではなく、投資元本を上回る損失を被ることがあります。弊社が行う金融商品取引業に係る手数料または報酬は、締結される契約の種類や契約資産額により異なるため、当資料において記載せず別途ご提示させて頂く場合があります。具体的な手数料または報酬の金額・計算方法につきましては弊社担当者へお問合せください。 当資料及び記載されている情報、商品に関する権利は弊社に帰属します。したがって、弊社の書面による同意なくしてその全部もしくは一部を複製またはその他の方法で配布することはご遠慮ください。 商号等: ロベコ・ジャパン株式会社 金融商品取引業者 関東財務局長(金商)第2780号 加入協会: 一般社団法人 資産運用業協会