Portfolio Manager

まとめ

- Japan success brings persistent Korea valuation discount into focus

- South Korea resolved to act on governance with elections looming

- Action will unlock value and underpin investor confidence in this key EM economy

The Korean stock market discount phenomenon is characterized by Korean-listed companies trading at a consistent discount to international counterparts. The disparity exists even when the earnings per share (EPS) and book value per share (BPS) of these companies are comparable.

A comparison of the price-to-book ratio (PBR) across different regions, including Korea, offers insight into the reality of this issue.

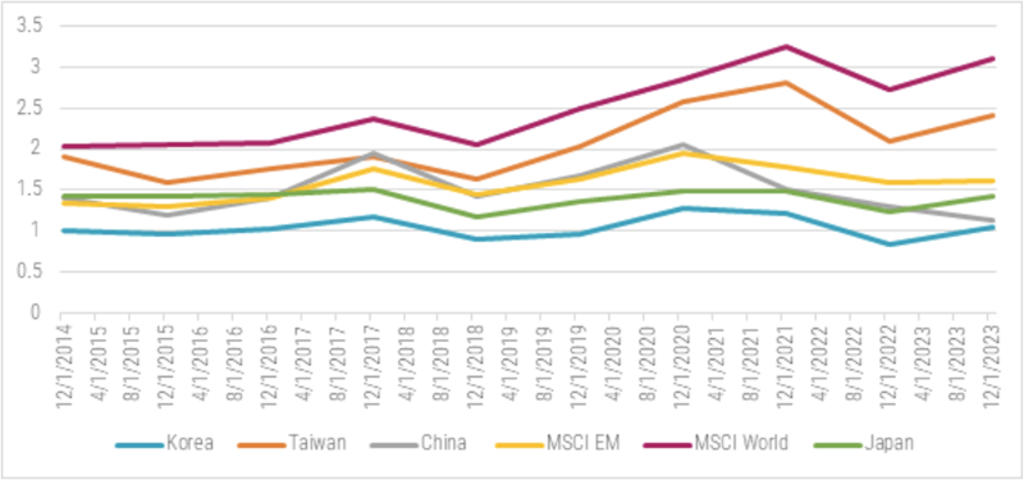

Figure 1: PBR - Korea vs peers and indices

Source: Bloomberg, MSCI, 1 January 2024.

Between 2014 and 2023, the PBR of Korean companies was merely 58% of the average of advanced countries’ indices and 34% of the emerging markets’ average illustrating the existence of the Korea discount.1 At the end of 2023, the MSCI Korea Index traded at a PBR of 1.1 times, in contrast to the MSCI Taiwan Index at 2.4 times and the MSCI Japan Index at 1.4 times. Korea has also traded at a P/E discount. Between 2014 and 2023, the MSCI Korea Index’s average P/E ratio was 12.2, according to Bloomberg, a 19% discount to Taiwan and a 28% discount to Japan over the same period.

Korea discount explanations

The frequently cited reason for the ‘Korea discount’ is geopolitical risk. However, this perspective seems incredible. According to Global Firepower, South Korea ranks fifth in military strength in the world, and is a key ally of the number one ranked US. Moreover Taiwan, widely considered as militarily vulnerable as South Korea, doesn’t seem to be subject to the same discount.

The role of ‘Chaebol’ firms, such as Samsung, LG, and Hyundai, in contributing to the Korea discount is also debated. These firms are predominantly managed by families across generations, raising concerns about family-centric governance and minority shareholder expropriation risks. Historically, numerous Chaebol family heads have faced legal challenges related to succession issues. However, research indicates that since 2007, the discount applied to Chaebol firms has been significantly lower compared to other Korean companies.2

What, then, are the real reasons behind the Korea discount? Empirical research by the KCMI3 sheds light on this. Analyzing data from 45 major stock markets, they identified key factors such as low shareholder return policies (including dividends and buybacks), a low return on equity (ROE), and limited growth potential. At a seminar in November 2022, the Financial Services Commission, Korea Exchange, and Capital Research presented data showing South Korea’s dividend payout ratio in 2021 was 19%, the lowest among its global counterparts. Taiwan, by comparison, had a much higher rate of 55%, followed by the UK at 48%, Germany at 41%, France at 39%, and the US at 37%. China also surpassed South Korea, with a dividend payout ratio of 35%.

The ‘Value-Up’ proposal and other solutions

To enhance shareholder returns in Korean companies, various strategies are under consideration. The Korean financial regulator is evaluating a proposal to identify and challenge companies with a PBR of less than one. Known as the Value-Up proposal, key elements will include the publication of investment metrics like PBR and ROE for listed companies. Additionally, these companies will be recommended to disclose their plans for improving corporate value. This approach mirrors the Tokyo Stock Exchange’s April 2023 initiative, which subsequently contributed to the Nikkei 225 index reaching a new record high.

President Yoon has taken a proactive stance on stock market issues, advocating for a short-selling ban and emphasizing the need for societal consensus to reduce the burden of excessive inheritance taxation in Korea, which significantly affects business decision-making. In Korea, inheritance taxes, ranging from 50% to 60%, significantly affect Chaebol families, eroding their ownership stakes over generations and influencing their preference for maintaining control, rather than maximizing shareholder value.

Problematic demographics

With this April’s general election for the National Assembly, Korea’s legislative body, the issue of the Korean discount might become a significant agenda item. Approximately 12 million stock investors, about a quarter of the electorate, could influence this focus. The reform of the national pension system is also intricately linked to this issue. With Korea’s birth rate being one of the lowest among OECD countries, there is an urgent need for society to consider reforms aimed at ensuring the sustainability of the pension system. Improving the performance of the Korean equity market is one of the key issues under consideration for this reform.

The South Korean financial authorities have introduced the concept of implementing the Value-Up program but have clarified that its enforcement will not be mandatory. The policy to increase shareholder returns in South Korea seems to be led by the private sector, primarily composed of academia and financial market stakeholders. On 6 February, Chairman Rhee of South Korea’s Corporate Governance Forum sent an open letter to the government’s financial authorities titled, ‘Without ending the Korea discount, there is no future for youth.’4 In this letter, he cited Hyundai Motor, Samsung Electronics, LG Electronics, LG Chem, and KB Financial as prime examples of companies affected by the Korea discount. As the title of Chairman Rhee’s letter suggests, Korean society appears to agree that without financial market reform, there is no future for the younger generation.

We believe that South Korean society will embrace a long-term roadmap to resolve the Korea discount and make consistent efforts toward this goal. Robeco’s fundamental emerging markets equities strategies are all currently overweight Korea, which is a stable and attractive economy exposed to key investment themes including green energy, tech and AI. We expect the steps taken to eliminate the Korea discount to also vindicate our overweight positioning.

Footnotes

1Bloomberg L.P.(2024), MSCI indexes annual valuation data, between 2014 to 2023, Bloomberg Professional, [Accessed February 7, 2024].

2R Ducret, D Isakov, 2020, The Korea Discount and Chaebols, Pacific Basin Finance Journal

3J.S. Kim, S.H. Kang, 2023, Analysis of the Causes of the Korea Discount, Korea Capital Market Institute

4Namuh Rhee, Feb 2023, Without ending the Korea Discount, the youth has no future, Korea Corporate Governance Forum

重要事項

当資料は情報提供を目的として、ロベコ・ジャパン株式会社(以下「当社」)が独自に作成、または当社のグループ会社(Robeco Institutional Asset Management B.V.およびその関連会社を含む)から提供された資料を当社が編集・翻訳したものです。資料中の個別の金融商品の売買の勧誘や推奨等を目的とするものではありません。記載された情報は十分信頼できるものであると考えておりますが、その正確性、完全性を保証するものではありません。意見や見通しはあくまで作成日における弊社の判断に基づくものであり、今後予告なしに変更されることがあります。運用状況、市場動向、意見等は、過去の一時点あるいは過去の一定期間についてのものであり、過去の実績は将来の運用成果を保証または示唆するものではありません。また、記載された投資方針・戦略等は全ての投資家の皆様に適合するとは限りません。当資料は法律、税務、会計面での助言の提供を意図するものではありません。 ご契約に際しては、必要に応じ専門家にご相談の上、最終的なご判断はお客様ご自身でなさるようお願い致します。 運用を行う資産の評価額は、組入有価証券等の価格、金融市場の相場や金利等の変動、及び組入有価証券の発行体の財務状況による信用力等の影響を受けて変動します。また、外貨建資産に投資する場合は為替変動の影響も受けます。運用によって生じた損益は、全て投資家の皆様に帰属します。したがって投資元本や一定の運用成果が保証されているものではなく、投資元本を上回る損失を被ることがあります。弊社が行う金融商品取引業に係る手数料または報酬は、締結される契約の種類や契約資産額により異なるため、当資料において記載せず別途ご提示させて頂く場合があります。具体的な手数料または報酬の金額・計算方法につきましては弊社担当者へお問合せください。 当資料及び記載されている情報、商品に関する権利は弊社に帰属します。したがって、弊社の書面による同意なくしてその全部もしくは一部を複製またはその他の方法で配布することはご遠慮ください。 商号等: ロベコ・ジャパン株式会社 金融商品取引業者 関東財務局長(金商)第2780号 加入協会: 一般社団法人 資産運用業協会