Portfolio Manager

¿Qué oportunidades ofrecen los ME?

Reciba nuestro newsletter para profundizar en las oportunidades de inversión en ME.

High yields, shifting capital flows, and structural tailwinds are putting emerging market debt back on the agenda. But should investors favor local or hard currency bonds in the search for income and resilience?

Emerging markets are back in focus, outperforming developed markets and increasingly benefiting from structural shifts in the global economy. This has renewed interest in EM debt: local currency bonds have been buoyed by high carry and a weaker dollar, while hard currency debt has drawn flows with high yields and strong fundamentals.

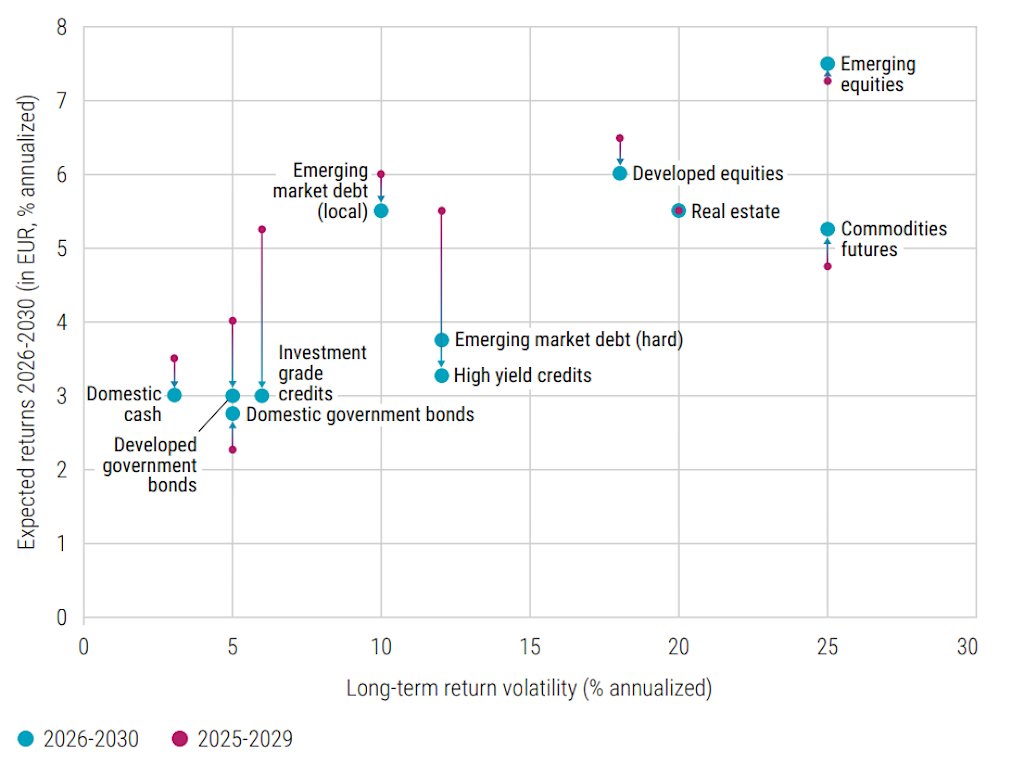

Robeco’s five-year expected returns suggest the attractiveness of EMD is not just cyclical but structural, with projected long-term base case returns of 6.25% for local currency and 4.50% for hard currency EMD annually – levels that surpass those of other fixed income asset classes.1 Yet emerging market debt is far from straightforward, each moving to different global and local rhythms of rates, spreads and FX.

So, what should investors choose?

We staged a mock ‘battle of perspectives’ between our local currency Portfolio Manager, Richard Briggs (RB) and our hard currency Portfolio Managers Nicholas Sauer (NS), asking them how they would respond to a series of real-world scenarios.

RB: In a dollar weakening cycle, local EMD tends to be strongly supported because the asset class is highly FX-focused and the dollar is the main driver. A global growth slowdown can also be positive for local markets, as it pushes central banks toward easing, which supports local bond returns.

Carry remains significant in local currency debt. While it can be eroded by FX weakness, in the current environment of either a stable or weaker dollar, investors can capture both carry and spot FX returns. Longer term, the dollar still looks overvalued: even with this year’s weakness, it remains much stronger than in the early 2010s, suggesting scope for further depreciation.

Ultimately, the key drivers for EM FX are financial flows and trade flows. While trade tensions remain an issue, signs of reallocation away from US assets suggest a supportive environment for local EMD.

NS: The current environment is conducive for EM hard currency returns. A slowing US economy is usually associated with the Fed cutting rates, and because EM hard currency bonds are denominated in US dollars, they trade off the US yield curve and benefit directly when US yields move lower.

While a weaker dollar does not impact dollar-denominated assets directly, it does improve EM fundamentals, which in turn supports tighter spreads – another positive for EM hard currency returns. Yields are also attractive: at around 7.7%, they sit in the 76th percentile historically. That income provides solid support for expected returns, with additional upside possible if spreads tighten further or US yields decline further.

Reciba nuestro newsletter para profundizar en las oportunidades de inversión en ME.

RB: Local currency markets can experience drawdowns, but one of their key advantages is liquidity. Even in times of stress, local government bond markets typically remain open and tradeable, with local banks providing liquidity. That makes it easier for investors to transact compared to some credit markets, where liquidity can dry up.

Another benefit is diversification. Local bonds are less correlated with other fixed income assets because of their FX component, providing exposure across multiple regions and currencies rather than just the US dollar. While risk-adjusted returns in local have looked weaker over a longer period, that has created room for a rebound – and indeed, this year local currency debt has been one of the best-performing global asset classes. For investors seeking diversification and consistent liquidity, local bonds can play a vital role, especially when other fixed income asset classes face challenges.

NS: For a client prioritizing easy exit and low drawdowns, hard currency EM debt offers a strong case. Default risk in EM is currently limited: we have just come through a cycle of sovereign stress, and balance sheets are now much cleaner and stronger both historically and relative to DM.

On the volatility side, hard currency bonds have historically been far more stable than local currency. This is because spreads and yields in hard currency bonds tend to be negatively correlated, which helps keep overall yields relatively steady. Today’s yield of around 8% also provides a meaningful cushion: with that level of income and an average duration of seven years, the asset class can absorb a rise of more than 1% in yields before returns turn negative. All told, hard currency screens well for investors seeking lower volatility, solid risk-adjusted returns, and reliable liquidity.

Capital at risk: Returns are geometric and annualized. The scenarios presented are not an exact indicator. They are an estimate of future performance based on current market conditions and evidence from the past on how the value of this investment varies. Expected returns will vary dependent on market performance.

Source: Robeco. September 2025. Vertical axis shows the expected geometric annualized returns for a euro investor over 2026-2030 and 2025-2029. The horizontal axis is a proxy for the long-term volatility of each asset class.

RB: For investors reducing US exposure, local currency EMD offers several angles. Compared to EM equities, local debt provides FX exposure but with typically smaller drawdowns, as bonds tend to outperform in slower growth environments. The country mix also differs as local benchmarks have much less China exposure than EM equity indices, which improves diversification.

For investors moving out of US investment grade credit, EM local bonds offer useful duration exposure with different dynamics than hard currency debt. They can outperform in certain rate environments, while also providing diversification benefits for those reallocating from high yield, as local markets are less correlated with global credit.

NS: Hard currency behaves like a credit asset class, correlating more closely with US and European IG and HY markets. For investors wanting a more straightforward fixed income exposure, with generally lower volatility and default risk, hard currency is the natural fit. Yields remain attractive, and with cleaner EM balance sheets after the recent default cycle, the fundamental risk profile of hard currency looks much improved. For many fixed income allocators, hard currency provides the most direct and comparable alternative to US credit.

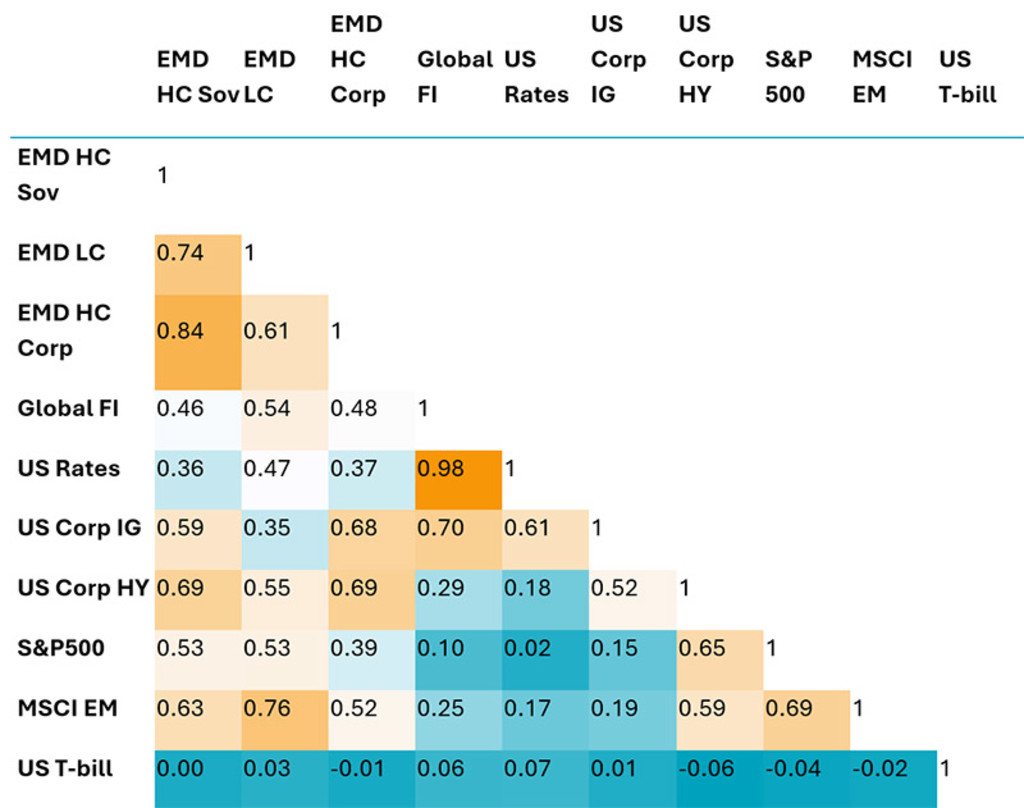

Source: Bloomberg, J.P. Morgan, MSCI, S&P, Robeco. EMD HC Sov: JPM EMBI Global Diversified Index, EMD LC: JPM GBI-EM Global Diversified Index, EMD HC Corp: JPM CEMBI Index, Global FI: Bloomberg Global Aggregate Index, US Rates: Bloomberg Global Aggregate - Treasuries Index, US Corp IG: Bloomberg US Corporate Bond Index, US Corp HY: Bloomberg US Corporate High Yield Bond Index, MSCI EM: MSCI Emerging Markets, US T-bill: Bloomberg US Treasury Bills: 1-3 Months Index. April 2025.

RB: Most recent flows into local EMD have gone into passive ETFs, but the performance gap is telling. ETFs have generally underperformed active funds, even against the weaker quartile of managers. The reason is simple, the local universe is extremely diverse. You have countries like China yielding 1.5%, Brazil around 13–14%, and Turkey in the 30s. An active manager can actively manage those exposures dynamically depending on both local and global macro factors.

Active funds also have more tools at their disposal: separating FX from bond exposure, using forwards and swaps to adjust hedges, or positioning along different parts of the curve. Importantly, active managers can access frontier markets that are not in the benchmark, places like Egypt or Nigeria which are often uncorrelated and carry-rich. While riskier, these positions can significantly enhance returns if carefully selected, and passive ETFs simply don’t take this into account.

NS: In hard currency, passive ETFs also tend to underperform. They closely track benchmarks but almost always with a small drag, so they end up delivering slightly worse risk/return. On top of that, ETFs often use modified benchmarks with higher minimum bond sizes to ensure liquidity, which means smaller, higher-yielding issues are excluded. That not only reduces potential return but can also increase volatility.

Active management can do much more like select corporate bonds, access frontier sovereigns, and exploit relative value opportunities outside the index. Historically, this has meant that passive hard currency strategies show Sharpe ratios around 20% lower than active. The main reason flows have gone to ETFs is convenience – it’s easier for allocators to buy something simple and liquid with low tracking error. But for anyone looking for genuine performance and risk-adjusted returns, active hard currency strategies offer far more.

1See table 5.5, page 122: 5-year Expected Returns: The Stale Renaissance