Client Portfolio Manager

• Visión

Ocho economías emergentes que marcan la diferencia

En un mundo que cambia rápidamente, creemos que optimizar la selección de países de mercados emergentes puede impulsar el éxito y ayuda a fundamentar el marco de rentabilidad/riesgo para seleccionar las compañías en las que invertir. En este artículo vamos más allá de los titulares y destacamos los países en los que nos centramos hoy en día.

Autores/Autoras

Top keywords

Resumen

- La selección de países es vital para triunfar en el amplio universo de los mercados emergentes

- La selección de valores se basa en el análisis top-down de las dinámicas de regiones y países

- Por el momento nos interesan las perspectivas de Grecia, Corea del Sur, Vietnam, Indonesia, Sudáfrica, México, Emiratos Árabes Unidos (EAU) y Polonia

Los mercados emergentes (ME) han mostrado solidez a lo largo de 2025. De hecho, el índice de referencia de renta variable MSCI EM alcanzó a principios de septiembre su nivel más alto desde 2021. Como venimos sosteniendo, consideramos que esto es solo el principio para la renta variable de los ME, puesto que los inversores globales se están distanciando de los mercados desarrollados (MD), cuyo potencial de crecimiento se ve limitado por los elevados niveles de deuda y las desfavorables tendencias demográficas. La guerra comercial iniciada por EE.UU. está acelerando la concentración de los ME en el comercio intrarregional y fortaleciendo la influencia geopolítica de agrupaciones multinacionales, como la Asociación de Naciones del Sudeste Asiático (ASEAN)1 y el Consejo de Cooperación del Golfo (CCG)2 . A largo plazo, este desarrollo es positivo para los ME. Por último, la probable flexibilización de la política monetaria estadounidense y el interés a largo plazo de la administración de Trump en que el dólar estadounidense se debilite constituyen un cómodo telón de fondo para que los inversores globales aumenten gradualmente su ponderación en los activos de ME.

Al examinar la amplia gama de países en los que invertimos, nos centramos en los fundamentales macroeconómicos, como las tasas de crecimiento del PIB, la inflación, la estabilidad de la moneda y la solidez de la política fiscal. Esto se complementa con consideraciones ASG, como el contexto político y normativo, lo que incluye la estabilidad, los niveles de corrupción y la transparencia en materia de reglamentos. También prestamos especial atención a las tendencias demográficas y de consumo, las cuales influyen en el crecimiento de la demanda a largo plazo y en la asignación sectorial. Por último, tenemos en cuenta el tamaño y la liquidez del mercado, los cuales influyen en la facilidad de entrada y salida de las inversiones.

Desde una perspectiva macroeconómica, nos beneficiamos de las aportaciones del equipo EM Fixed Income de Robeco, que invierte en deuda de ME. En 2025, los ME se encuentran en una posición financiera mucho más sólida que en el pasado. Muchos han acumulado reservas, han mejorado sus cuentas corrientes y han reducido la carga de la deuda externa, con lo que han aumentado su resiliencia ante las perturbaciones externas y la volatilidad mundial. Los fundamentales generales del universo de los ME mejoran constantemente con el crecimiento y el desarrollo continuos de estas economías. Esto allana el camino para que cada vez más emisores de ME accedan a los mercados mundiales de capitales, lo que a su vez contribuye a un círculo virtuoso de estabilidad macroeconómica y crecimiento.

La importancia de la selección de países

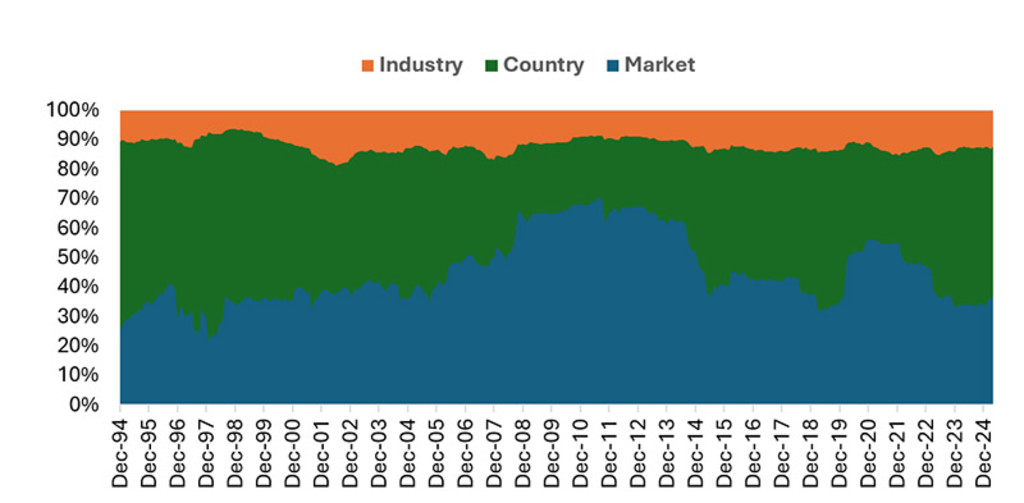

Siempre hemos considerado que la asignación por países es un motor clave de la rentabilidad, y esta opinión está respaldada por pruebas fehacientes. El gráfico muestra que, desde 1994, la asignación por países siempre ha contribuido significativamente a la volatilidad de la rentabilidad de los ME, y que esta contribución ha vuelto a aumentar en los últimos años. Dicha volatilidad implica que hay oportunidades de obtención de alfa3 que se pueden captar con la asignación activa por países.

Figure 1: Contributors to volatility of returns in emerging markets since 1994

Fuente: Robeco y Thomson Financial Datastream, equipo de estudio cuantitativo, desde diciembre de 1994 hasta abril de 2025.

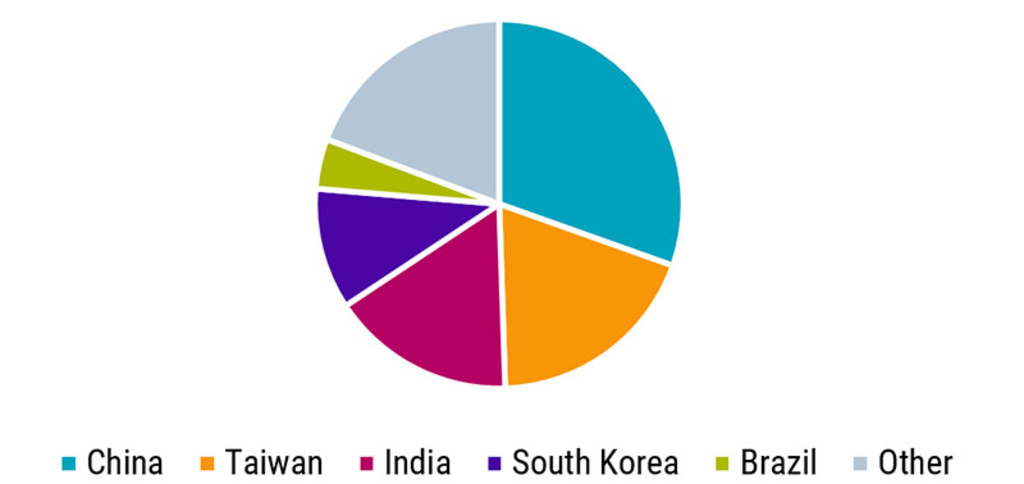

Utilizamos MSCI Emerging Markets Index como índice de referencia en nuestra estrategia estrella, Robeco Emerging Markets Equities, y en la estrategia de alta convicción, Robeco Emerging Stars Equities. El índice refleja el crecimiento pasado de las mayores economías emergentes, como China y la India, y es intrínsecamente retrospectivo. Dado que somos inversores activos e intentamos superar al índice, utilizamos la selección top-down de países como motor potencial de alfa. Esto significa que adoptamos exposiciones nulas, infraponderadas, igual de ponderadas o sobreponderadas a los 24 países del índice: Arabia Saudí, Brasil, Chile, China, Colombia, Corea del Sur, Egipto, Emiratos Árabes Unidos, Filipinas, Grecia, Hungría, India, Indonesia, Kuwait, Malasia, México, Perú, Polonia, Qatar, República Checa, Sudáfrica, Tailandia, Taiwán y Turquía. Y, lo que es más importante, también podemos incluir compañías de países que no sean uno de estos 24, lo cual es una fuente crucial de posible alfa tanto en 2025 como en el futuro.

Gráfico 2: Ponderaciones por país del MSCI Emerging Markets Index

Fuente: MSCI, 29 de agosto de 2025.

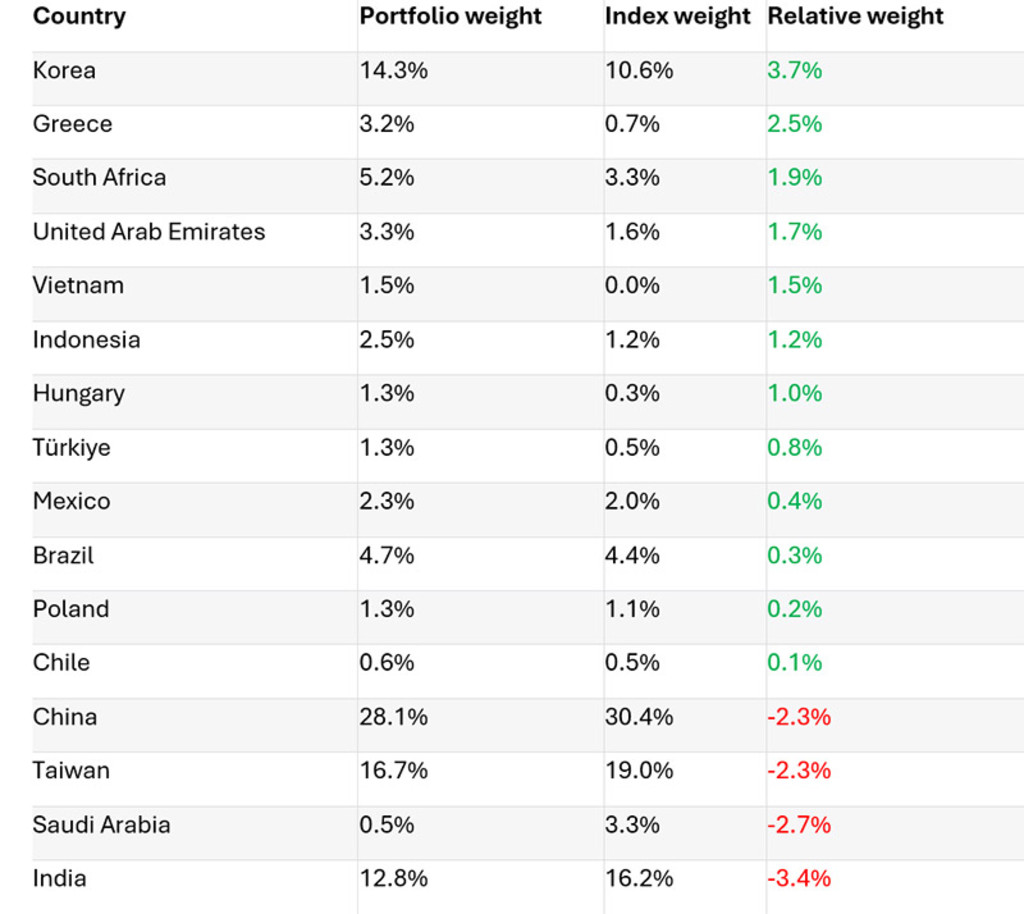

Las inversiones en compañías de distintos países, no solo de uno, contribuyen a reducir el riesgo de sufrir los efectos de problemas económicos, políticos o específicos de una compañía que afectan a un solo país. Mientras tanto, es positivo para nuestras carteras de ME evitar la exposición a países cuyos riesgos idiosincráticos consideramos elevados. A modo de ejemplo, la tabla 1 ilustra la asignación por países de la estrategia Robeco Emerging Market Equities a finales de agosto de 2025 en comparación con el índice.

Tabla 1: Asignación por países de la estrategia Robeco Emerging Market Equities con sobreponderaciones e infraponderaciones

Fuente: Robeco, MSCI. Cartera: Robeco Emerging Markets Equities. Índice: MSCI Emerging Markets. Datos de finales de agosto de 2025. A efectos meramente ilustrativos. Este es el panorama actual en la fecha arriba indicada y no garantiza la evolución futura. No debe suponerse que las inversiones en los países o sectores identificados hayan sido o vayan a ser rentables.

La tabla 1 no incluye los países en los que teníamos una exposición nula a finales de agosto, como Malasia y Filipinas.

Emerging Markets Equities D EUR

- performance ytd (31-3)

- 3,81%

- Performance 3y (31-3)

- 14,44%

- morningstar (31-3)

- SFDR (31-3)

- Article 8

- Pago de dividendos (31-3)

- No

Rentabilidades pasadas no garantizan resultados futuros. El valor de las inversiones puede fluctuar.Anualizado (para periodos superiores a un año). Las rentabilidades son netas de comisiones, basadas en los precios de transacción.

Ocho países emergentes que nos interesan hoy en día

El mundo se enfrenta en estos momentos a una incertidumbre económica considerable, tal vez incluso sin precedentes, y las repercusiones de las medidas proteccionistas aún no se perciben plenamente. Teniendo en cuenta este difícil contexto, hemos seleccionado ocho países del universo de ME en los que estamos sobreponderados y donde vemos oportunidades de cara al segundo semestre de 2025 y el futuro.

Grecia

La recuperación de Grecia tras la crisis de la deuda de la UE de 2012 ha sido lenta y constante, pero estamos descubriendo compañías que se están beneficiando de su resurgimiento macroeconómico. Los motores del crecimiento son el sólido consumo interno y las inversiones, impulsados por los proyectos del Fondo de Recuperación de la UE, y las exportaciones. El país también se está haciendo un hueco en el turismo, las energías renovables y el transporte marítimo, sectores en los que Grecia mantiene una ventaja competitiva respecto al resto del mundo.

Se espera que la inflación se modere entre 2025 y 2026, a pesar de la mejora del mercado laboral: la tasa de desempleo se sitúa por debajo del 9% y el crecimiento salarial favorece el poder adquisitivo interno.

Además, incluso tras un periodo de rentabilidad superior constante, las valoraciones de Grecia siguen siendo atractivas. Para los inversores, Grecia representa un caso inusual de recuperación impulsada por reformas dentro de los ME, pues es un país que ha pasado de estar al borde del impago a ostentar una relativa estabilidad macroeconómica, y que ahora tiene un potencial de crecimiento constante, aunque no sea espectacular. Sin embargo, no logra deshacerse de una vulnerabilidad: la ratio de endeudamiento público sigue siendo una de las más altas de Europa, lo que provoca que Grecia sea sensible a los cambios en los tipos de interés mundiales y en la confianza de los inversores.

Corea del Sur

Corea del Sur es un destacado ejemplo de éxito entre los ME, y su condición de líder en tecnología crucial para el desarrollo de la IA y los sectores de la electrificación y la defensa ha contribuido a la aparición de compañías de talla internacional. A pesar de ser muy sensible a la guerra comercial de la administración estadounidense, el sector corporativo coreano está prosperando y, en nuestra opinión, se beneficia de importantes impulsos estructurales. El principal de ellos es la iniciativa «Value-Up», que está forzando reformas de la gobernanza corporativa y dando alas a un importante valor oculto en las complejas estructuras de las compañías coreanas. Se trata de un tema que avanza lentamente, pero que, en nuestra opinión, está cobrando impulso.

Vietnam

Vietnam es un ME clásico que posee una población de 100 millones de habitantes (de los cuales, más del 60% tienen menos de 30 años), está en proceso de urbanización y ha experimentado un rápido crecimiento como exportador de productos manufacturados. Los inversores extranjeros se han mostrado cautos debido a su gobierno socialista y a un mercado de renta variable cuya liquidez es relativamente escasa, pero nos complace estar presentes e invertir en dicho país. Aunque la dinámica comercial con China y EE.UU. es difícil hoy en día, Vietnam siempre ha sabido mantener buenas relaciones con ambos países. La administración actual está supervisando una rápida reestructuración, más inversión extranjera directa (IED) y la construcción de infraestructuras, especialmente de carreteras y ferrocarriles.

La próxima década se presenta prometedora para Vietnam en términos de dinámica económica, así que estamos valorando algunas oportunidades en los sectores del consumo interno al servicio de la floreciente clase media, las finanzas, el sector inmobiliario y la tecnología, así como en sectores relacionados con las exportaciones. Creemos que tiene sentido invertir una pequeña parte de una cartera de ME en este país fuera del índice de referencia, teniendo en cuenta el riesgo asociado a las compañías en las que invertir, las valoraciones y unas fluctuaciones del mercado superiores a la media. Por último, Vietnam está haciendo progresos notables para su inclusión en el MSCI Emerging Markets (EM) Index, y se espera que entre en la MSCI EM Watch List a finales de 2025. Si se cumplen los criterios, su incorporación al MSCI EM Index podría producirse entre 2026 y 2028, así que este es otro motivo para que los inversores a largo plazo adopten cierta exposición a este país.

Indonesia

Los motores del crecimiento de Indonesia son el aumento del consumo privado, el gasto público en infraestructuras y las iniciativas de inversión, como el programa de vivienda «People-First Housing», así como la influencia cada vez mayor del fondo soberano Danantara. La inflación se mantiene relativamente baja y estable, entre el 2,3% y el 3%, lo que respalda el consumo y permitió al banco central recortar los tipos de interés a mediados de septiembre de 2025. La situación política ha sido tensa, dado que las personas con rentas más bajas siguen atravesando dificultades y se produjeron intensas protestas en agosto, lo cual preocupa a los inversores extranjeros. No obstante, más allá de los titulares, consideramos que Indonesia experimentará un rápido crecimiento y confiamos en nuestra posición sobreponderada.

Sudáfrica

Los inversores en ME siempre han estado muy pendientes de Sudáfrica por ser la economía más avanzada de África y tener una gran influencia en el ámbito panafricano. Sudáfrica, que desde 2024 tiene un gobierno de coalición centrista, fue uno de los países con mejores resultados en 2024. Además, algunos de sus problemas obvios, como los cortes periódicos de electricidad, parecen estar reduciéndose. En 2025 vuelve a formar parte de los ME, pero ya se perciben los beneficios de un estilo de gobierno más moderado. Entre los motores del crecimiento figuran las mejoras de las infraestructuras, la clara reducción de la escasez de energía y el auge de los precios de las materias primas industriales, que han respaldado a su sector minero. La reciente bajada de la inflación hasta cerca del 3% debería permitir al banco central mantener una postura acomodaticia e impulsar tanto el consumo interno como las infraestructuras públicas. Seguimos de cerca las compañías de pequeña capitalización que cotizan con múltiplos de beneficios de un solo dígito, las cuales ni siquiera están en el punto de mira de la mayoría de los inversores internacionales, para aumentar nuestra exposición sudafricana.

México

El destino económico de México depende de EE.UU. y viceversa. A pesar de las diferencias ideológicas entre las respectivas administraciones de Sheinbaum y Trump, es absolutamente vital que encuentren puntos en común. México parece haberse puesto del lado de Trump en la disputa comercial con China al imponer aranceles muy elevados a los automóviles chinos. Además, la cooperación en materia de seguridad parece constructiva. Consideramos que esta situación deja intactas las fortalezas de México previas a la era de Trump en cuanto a experiencia manufacturera y apertura a la inversión extranjera, mientras que la incertidumbre comercial allana el camino a la acumulación de posiciones en compañías excelentes con proximidad y acceso al mercado de consumo más grande del mundo.

Emiratos Árabes Unidos

EAU se han convertido en un nexo económico regional y mundial con un perfil similar al de Suiza y Singapur. Las mayores bolsas, que son la DFM de Dubái y la ADX de Abu Dhabi, cuentan con una importante participación de inversores institucionales extranjeros, y es probable que esta cifra siga aumentando dadas las crecientes entradas de IED y el sólido perfil de crecimiento del país. Los EAU, tradicionalmente subyugados a los cambios en los precios de la energía, han trascendido esta dinámica con el crecimiento de los servicios financieros, la logística, la tecnología, el sector inmobiliario y el turismo, los cuales amplían su base económica.

La renta variable de EAU presenta una atractiva combinación de alta rentabilidad por dividendos (4-7%), valoraciones atractivas e impulso derivado de reformas como la liberalización de la propiedad extranjera, la inclusión en índices y sólidos procesos de OPI. La resiliencia de la renta variable de EAU se ve reforzada por unos bancos rentables y bien capitalizados, lo que los hace atractivos para los inversores que buscan tanto ingresos como crecimiento a largo plazo. Los sectores no petroleros impulsan ahora la mayor parte del crecimiento, y se prevé que el PIB se acerque al 5% en 2025. La inflación se mantiene baja y estable, y el sistema bancario es sólido. El sector inmobiliario y el comercio aportan un impulso adicional, mientras que las importantes reservas fiscales proporcionan resiliencia.

Polonia

Polonia es la estrella del firmamento de la UE como líder del crecimiento del continente. Se espera que su economía, cercana al billón de USD, crezca un 3,3% en 2026 y un 3,2% en 2027, según los pronósticos de consenso de Bloomberg. La demanda interna de una población de 38 millones de habitantes con un alto nivel educativo y el rápido crecimiento del consumo privado siguen siendo grandes motores. Estos se ven favorecidos por el aumento de los salarios reales, las prestaciones sociales y el gasto fiscal, incluido el incremento de las inversiones públicas y en infraestructuras con el apoyo de inversores internacionales en deuda polaca y fondos de la UE. La fuga de cerebros de principios siglo XXI a otros países de la UE y al Reino Unido se ha revertido, con lo que Polonia se está convirtiendo en un mercado laboral fértil para compañías en crecimiento. Al igual que Corea del Sur, Polonia es una economía emergente con fundamentales y un alto nivel de vida que es la envidia de las economías «desarrolladas».

Conclusión

Para nuestras estrategias de ME, la asignación por países es un punto de partida en nuestro proceso de inversión. Consideramos que nuestro enfoque sistemático top-down respecto a las regiones y los países complementa nuestro análisis fundamental y cuantitativo a nivel de empresa, lo cual nos permite calibrar eficazmente el riesgo en todas nuestras carteras. La incertidumbre generada por la situación convulsa del comercio internacional provoca que el análisis por países cobre más importancia como fuente de alfa. También proporciona a las estrategias activas de Robeco en ME una ventaja competitiva, especialmente frente a la exposición a ME basada en inversiones pasivas en índices. Una exposición amplia a los ME puede generar resultados desiguales, mientras que una asignación selectiva (centrada en mercados con instituciones creíbles, demanda interna en auge y marcos políticos favorables) puede presentar auténticas oportunidades. En el entorno actual, los ME no representan un solo ámbito de inversión, sino un conjunto de caminos divergentes.

Estrategias de ME cuantitativas

Nuestras estrategias de mercados emergentes también se ofrecen con una gestión cuantitativa:

Notas al pie

1La ASEAN está formada por Brunéi, Camboya, Filipinas, Indonesia, Laos, Malasia, Myanmar, Singapur, Tailandia y Vietnam.

2El CCG está formado por Arabia Saudí, Bahréin, Emiratos Árabes Unidos, Kuwait, Omán y Qatar.

3Alfa se refiere al rendimiento excedente de una inversión respecto a un índice de referencia y sirve para medir la rentabilidad.