Client Portfolio Manager

Discover emerging opportunities

Discover emerging opportunities by investing in the diverse and fast-growing dynamics of emerging markets.

With key inputs for AI infrastructure and renewable energy primarily found within emerging economies in Latin America, Africa and Asia-Pacific, we think EM investors will be beneficiaries of the global race for resources.

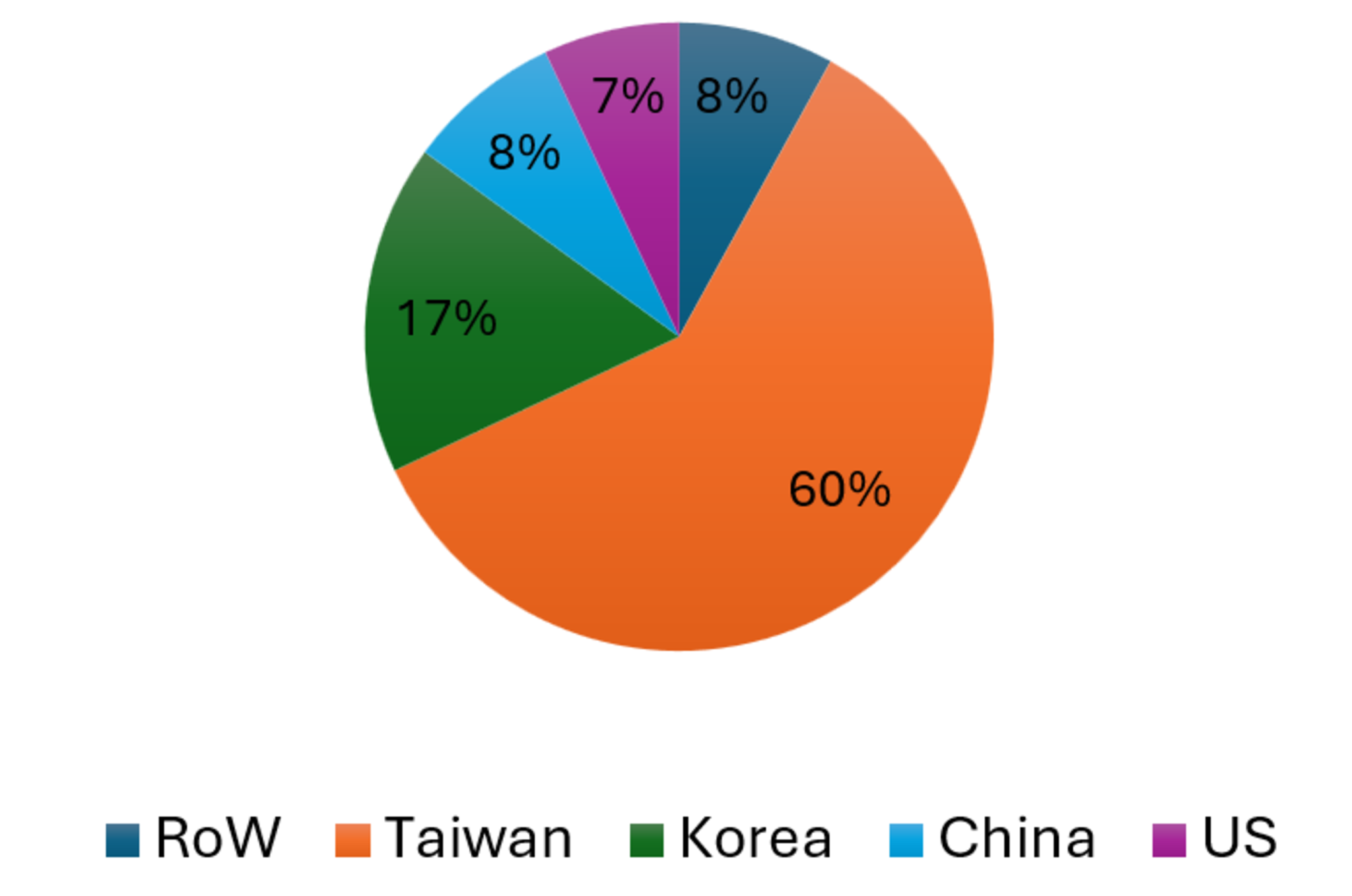

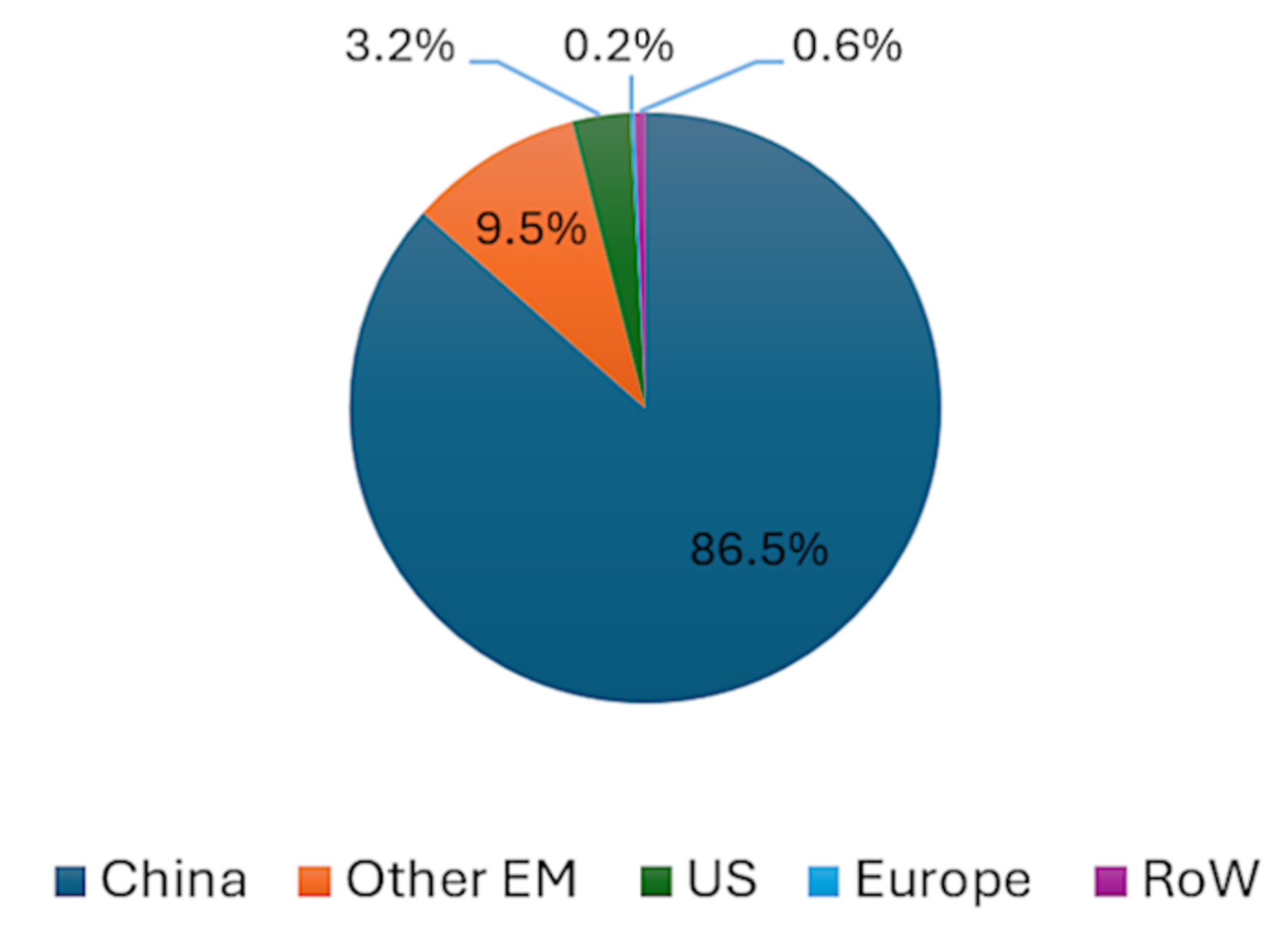

Emerging markets have moved into leadership positions in key technologies supporting the AI buildout, like semiconductor manufacturing (see Figure 1a), and the development and manufacture of renewable energy technologies like solar panels (see Figure 1b).

Source: TrendForce/Visual Capitalist (2024-2025 Estimates)

Source: StatRanker. PV module production for 2024

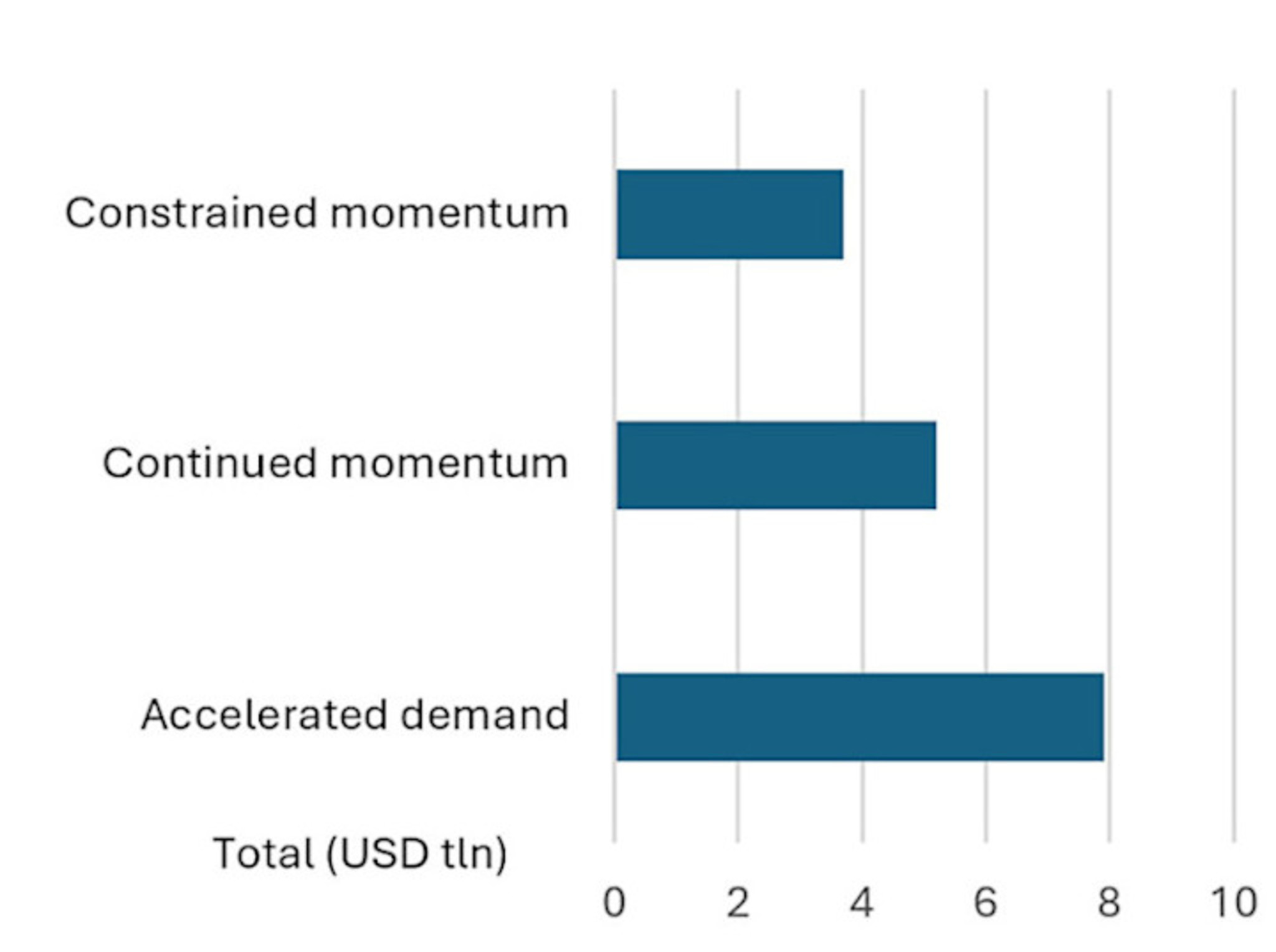

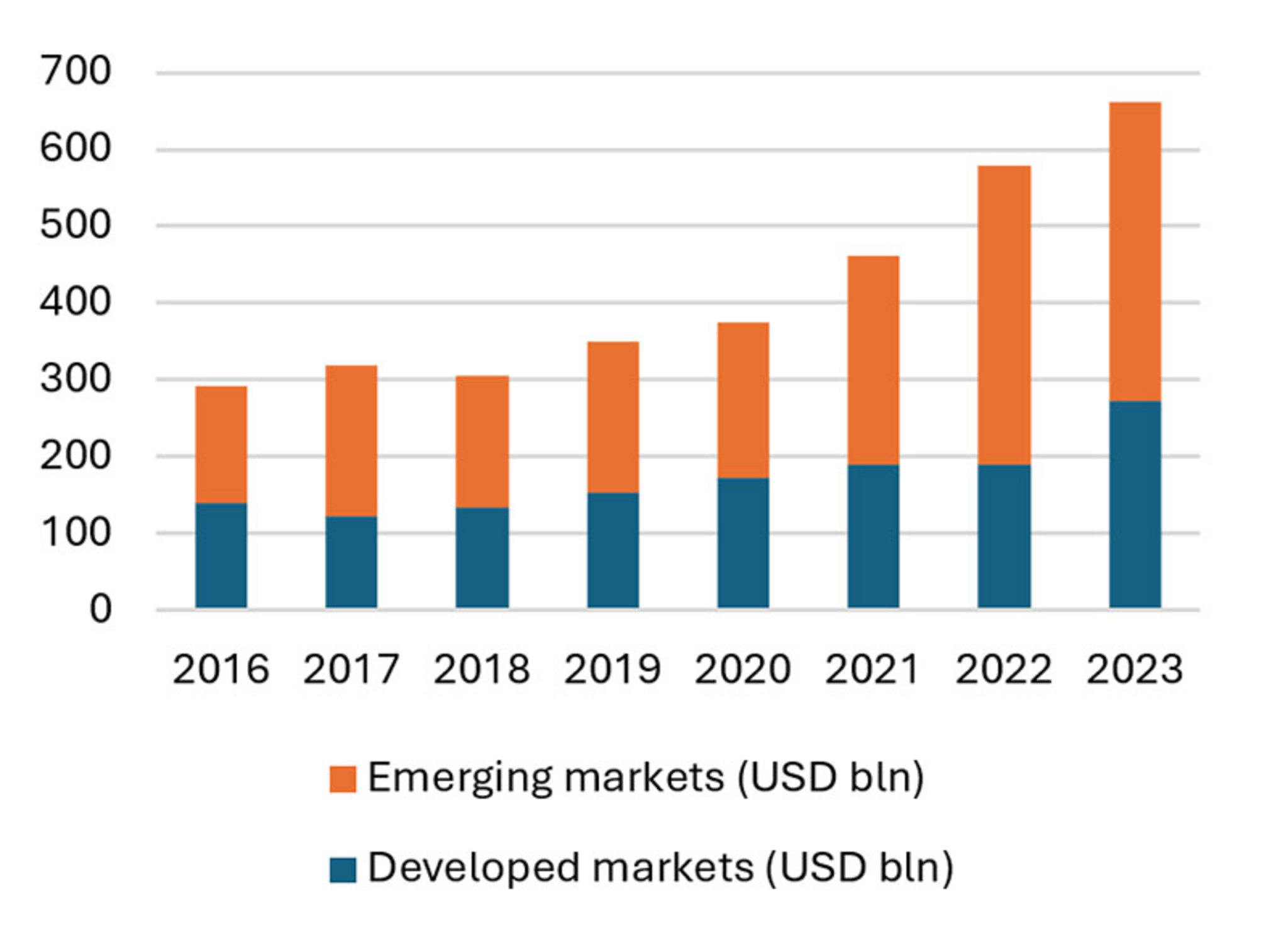

Both of these sectors are attracting vast amounts of capital expenditure in both developed and emerging markets, as Figures 2a and 2b show.

Source: McKinsey projections from April 2025 encompassing data center infrastructure, related IT equipment, and power generation capex to support data centers.

Source: BloombergNEF, Climate Investment Funds, World Bank, March 2025.

Discover emerging opportunities by investing in the diverse and fast-growing dynamics of emerging markets.

The two sectors are also inextricably linked. The AI revolution is contributing to rising electricity demand, which is in turn increasing demand for power generation sources, whether via fossil fuels, nuclear or renewables. The sudden jump in oil and LNG prices sparked by the Iran war in March 2026 has also illustrated the fragility of fossil fuel supply chains and is likely to further accelerate global investment in renewables, electrification and efficiency.

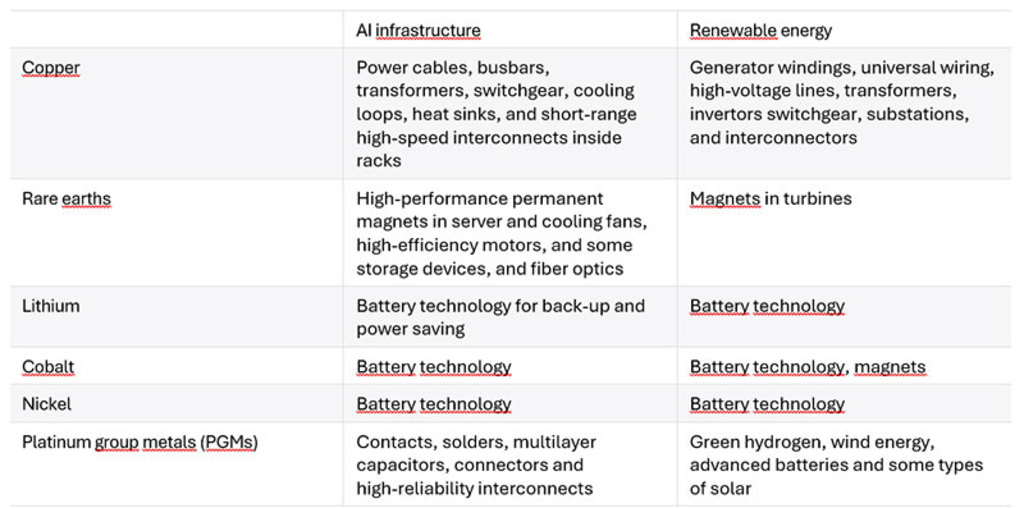

Moreover, the two trends are relying on many of the same mineral inputs to enable the infrastructure buildout (see Table 1), resulting in a surge in demand for these specific materials.

Sources: IEA, UN Task Force on Critical Energy Transition Minerals – December 2025, Artificial Intelligence and the Critical Minerals Crunch – FP Analytics, October 2025.

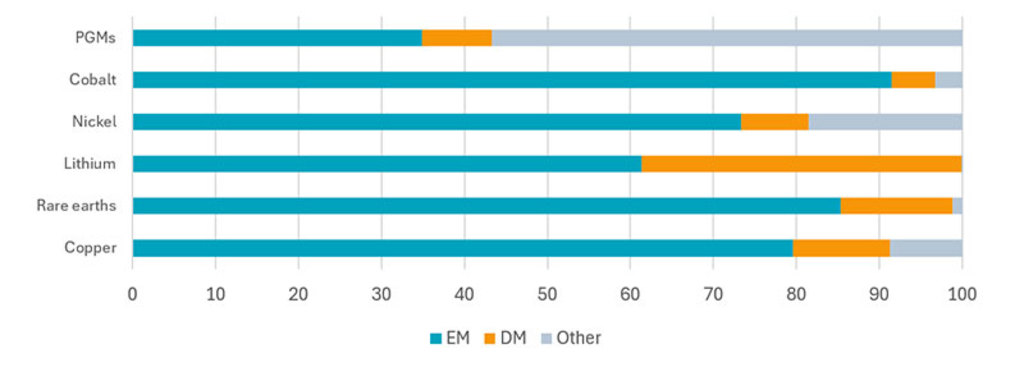

Of these key minerals, critical to both AI and the energy transition, a significant share of economically viable reserves and production is concentrated in emerging economies (see Figure 3).

Sources: IEA (2025), Global Critical Minerals Outlook 2025, IEA, Paris www.iea.org/reports/global-critical-minerals-outlook-2025, Licence: CC BY 4.0. ‘Other’ includes Russia and disputed resources

For example, South Africa remains the most reliable global source of PGMs. Chile, Zambia, Indonesia and the Democratic Republic of the Congo (DRC) supply the balance of global copper, while China dominates in rare earths mining and especially in processing. Indonesia is also the swing supplier in nickel, and the DRC dominates cobalt mining. The world’s largest lithium miner is a developed market (Australia), but the rest is produced in Chile, Argentina, China, and various African nations.

The location of these minerals has been given particular significance by the geopolitical tension between the US and China. Trade relations are worsening and the two global powers have established rival technology and military-industrial stacks. In particular, China has built a dominant position in metals and rare earths processing, outcompeting the steel and smelting sectors in the US and Europe, and leaving them dependent on China for the balance of refined supply in many key industrial inputs. This in turn has seen the US classify its mineral supply chain as a national security policy priority,1 rather than an issue that can be left to market forces.

In our view, this new environment is likely to elevate the value of emerging markets’ generous mineral endowment and also give emerging economies more leverage to capture value.

1 New Executive Order Ties U.S. Critical Minerals Security to Global Partnerships - Center for Strategic & International Studies – 15 January 2026

Receive our newsletter to dive deep into EM investment opportunities.