Client Portfolio Manager

• Insight

Innovation where it matters: generating alpha while maintaining disciplined control

For much of the past decade, developed market equities have rewarded investors for staying invested and, at times, for staying simple. But today’s market environment looks very different. For those seeking to improve on passive exposure without materially changing the overall risk profile, or for those aiming for higher alpha while remaining benchmark-conscious, quantitative investing can offer a compelling answer. But only if the process itself continues to evolve.

Authors

Client Portfolio Manager

Summary

- Risk is back: concentration, volatility, regime shifts reshaping equity investing

- How signals are refined and implemented shapes quantitative strategy outcomes

- Our quantitative platform aims to generate alpha while maintaining strong risk discipline

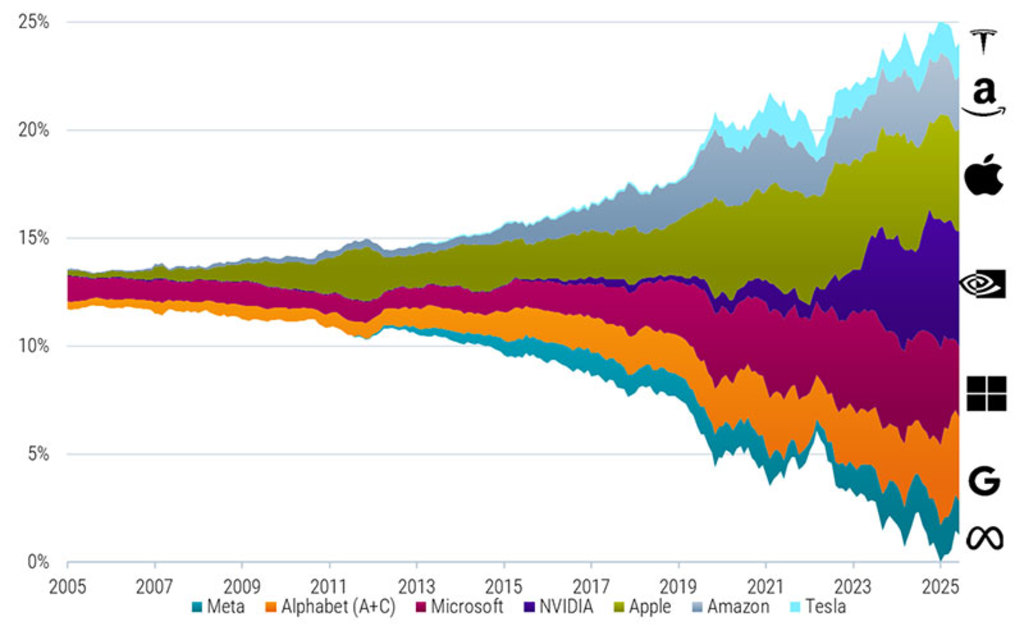

Risk has moved back to the center of equity investing. Investors today are navigating a market shaped by geopolitical tensions, policy uncertainty, and deglobalization pressures. The composition of equity markets has become more concentrated, shaped by the extraordinary rise of a relatively small group of dominant technology stocks – one version1 being the Magnificent Seven as shown in Figure 1 below.

Figure 1 – Weight of Magnificent Seven stocks in the MSCI World Index

Source: Robeco, LSEG. The figure shows the cumulative weight of the Magnificent Seven stocks in global developed markets. The Magnificent Seven comprise Alphabet (A & C shares), Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla. Global developed markets are represented by the MSCI World Index. The sample period covers October 2005 to March 2026. The companies shown in this graph are for illustrative purposes only. No inference can be made on the future development of the company. This is not a buy, sell, or hold recommendation

The result is a market environment in which volatility is likely to remain elevated and concentration risk harder to ignore. In an era defined by both opportunity and fragility, remaining invested in equities still matters – but so does how that equity exposure is built.

Investors still need equity exposure, but they want it with much clearer risk control than during the previous era of abundant liquidity and simpler market narratives. In such an environment, investors face a difficult balancing act, and that challenge is increasingly central for institutional investors.

For those seeking to improve on passive strategies without materially changing the overall risk profile, or for those aiming for higher alpha while remaining benchmark-conscious, quantitative investing can offer a compelling answer. In an environment where the range of possible outcomes has widened, the combination of adaptability and discipline becomes especially valuable.

From factors to signals: why quantitative investing had to evolve

The case for systematic investing today is not just a case for rules. It is also a case for continuous innovation. The early factor models developed in academic finance changed the way investors understand returns. These original frameworks, such as those associated with Fama and French, helped establish the idea that certain persistent company characteristics – including value, momentum and profitability – can help explain why some stocks outperform over time.

But, as our recent podcast discussion around the Fama-French framework makes clear, simple, static definitions have struggled to keep pace with changes in market structure, competition and data availability. Especially in the US market, they have become less effective over time. That does not mean the economic intuition behind factors has disappeared, but that harvesting return drivers in live portfolios has become more demanding. In other words, while the insights remain foundational, the way leading quantitative managers implement them has had to change significantly.

One reason is that broad factor definitions are often too blunt for real-world investing. Two managers may both claim exposure to ‘quality’ or ‘momentum’, for example, while using very different underlying definitions, data inputs and portfolio construction methods. The label may sound familiar, but the investment outcome can be materially different.

In that context, the question is not whether value, momentum or quality still work in the abstract. The more relevant question is whether a manager has continued to innovate in terms of how those ideas are captured and implemented. Quantitative managers might increasingly think less in terms of ‘factors’ and more in terms of ‘signals’: the specific, investable building blocks used to refine factors, identify opportunities, and construct portfolios.

Indeed, the edge lies not in the label, but in the implementation. That is precisely where end-to-end innovation becomes important: not only how alpha signals are identified, but also how portfolios are constructed, risk-managed and implemented.

Discover the value of quant

Subscribe for cutting-edge quant strategies and insights.

Alpha generation starts with stock selection

At the heart of Robeco’s quantitative equity strategies lies the stock selection model, built around a diversified set of alpha signals. Diversification across return drivers matters because it helps improve alpha resilience: markets do not reward every style at the same time. For example, value can lag for extended periods; momentum can reverse sharply, and quality can become expensive. A broader signal set can help reduce dependence on any single market regime.

Better signal design can also improve alpha quality. Refining how return drivers are measured – for example by improving how valuation is assessed, broadening analyst revision signals, or incorporating selected short-term and textual insights – can help distinguish between generic exposures and more investable sources of alpha. Over time, these refinements can materially affect outcomes.

Portfolio construction matters just as much

But even a strong stock selection model is only part of the story. In practice, many of the biggest differences between quantitative strategies emerge not from which stocks are liked on paper, but from how those preferences are implemented in the portfolio. This is especially true in today’s environment, where investors are increasingly focused on downside resilience, concentration risk, implementation efficiency and unintended exposures.

Portfolio construction is where alpha ambition is balanced against risk reality. At Robeco, this means using proprietary portfolio construction algorithms designed to target strong model exposure while controlling turnover, managing dynamic risks and taking implementation costs into account.

These capabilities matter because every basis point counts, particularly in strategies where risk budgets are deliberately managed. A good idea implemented inefficiently can easily lose much of its value in live investing. Conversely, better portfolio construction can improve the conversion of research insight into realized returns. That is why the distinction between research alpha and implemented alpha is so important. For investors, the question is not simply whether a signal works in theory, but whether it can be captured robustly after costs, within a real portfolio, and through different market conditions.

Two ways to apply the same philosophy

This end-to-end framework underpins both Robeco’s Enhanced Indexing and Active Quant developed market strategies – but in different ways, depending on investor objectives. For investors who want to stay close to the benchmark in overall risk terms, our Enhanced Indexing strategies aim to improve on passive exposure through disciplined stock selection and implementation. For investors willing to accept a broader tracking error budget in pursuit of higher alpha, our Active Quant strategies apply the same underlying philosophy in a more expressive way.

In quantitative investing, innovation can sometimes be misunderstood as a race toward ever-greater complexity. But that is not the goal. At Robeco, innovation is not about making the process more opaque. It is about making it more effective. The objective remains consistent: to deliver alpha in a way that is investable, disciplined and risk-aware.

Footnote

1 The composition of dominant index constituents evolves over time and may differ by definition; labels such as ‘FAANG’ or ‘Magnificent Seven’ are illustrative and not static.

Find breadth beyond Big Tech

Capture broader, diversified opportunities in developed markets by looking beyond Big Tech with disciplined, selective investing.