Head of Investments China

• Insight

China signals policy stability amid hopes of trade resolution

Policymakers view the first half of the year as having delivered satisfactory results in both GDP growth and trade negotiations. As a result, they have held off on short-term stimulus measures, ahead of detailing the 15th Five-Year Plan in October, which will prioritize long-term strategies aimed at addressing structural challenges.

Authors

Client Portfolio Manager

Top keywords

Summary

- China equity markets looking beyond trade negotiations

- Easy liquidity keeps sentiment positive

- July Politburo meeting signals patience and policy consistency

China’s 24-person Politburo reconfirmed its supportive fiscal and monetary policy approach in its July 2025 meeting but there was no new stimulus to excite equity investors. Instead, the focus was on continuity and long-term structural reforms. We remained constructive on Chinese equities believing that the worst of the trade negotiations with the US is over with market sentiment remaining firm, helped by relatively easy liquidity.

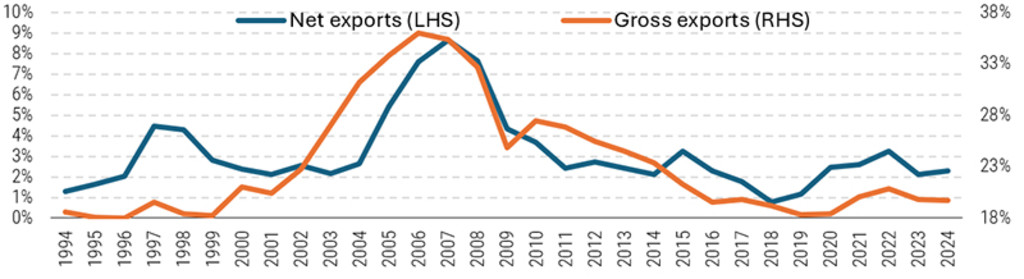

China’s unyielding stance in April when the US tariffs were initially announced has paid dividends with the tension gradually being dialed down since. Moreover, China clearly has leverage in the negotiations which the EU and Japan appear to lack despite their traditional status as US allies. Chinese and US officials agreed on 29 July to seek an extension of their 90-day tariff truce with growing optimism over a longer term agreement. The assured attitude of investors reflects the long-term reduction in the importance of trade to the Chinese economy (see Figure 1) as well the hope that opportunities for trade within Asia-Pacific, as well as EMEA countries and Latin America, will offset any reduction in exports to the US.

Figure 1: China exports as a percentage of GDP

Source: Robeco, CEIC, NBS. To end 2024

No stimulus silver bullet but opportunities ahead

The Politburo meeting has passed with a broad continuation of the existing policy mix and without any extra stimulus as H12025 economic targets were largely achieved. Nevertheless we see some clear opportunities in the emphasis put on specific policy areas. The post-meeting summary reaffirmed its commitment to supporting capital markets and liquidity is plentiful, reflected in increasing trading volumes.

Boosting consumption remains key but requires long-term reform

The Politburo also affirmed the necessity of boosting domestic consumption but only made limited policy commitments including improved social welfare measures, such as newborn subsidies, reflecting a gradual shift toward economic rebalancing and welfare enhancement. Existing policies like consumer goods trade-in initiatives will continue. The announcement of the Fourth Plenum in October highlights preparations for the 15th Five-Year Plan and more extensive policy action to boost consumption in the longer run is expected then.

Chinese Equities D USD

- performance ytd (31-3)

- -3.76%

- Performance 3y (31-3)

- 4.27%

- morningstar (31-3)

- SFDR (31-3)

- Article 8

- Dividend Paying (31-3)

- No

Past performance is no guarantee of future results. The value of the investments may fluctuate. Annualized (for periods longer than one year). Performances are net of fees and based on transaction prices.

Measured tone on anti-involution

The Politburo also restated its focus put on breaking the cycle of ‘involution’, the disorderly competitive activity in specific sectors. The anti-involution policies include revision of competition regulation, reduction or elimination of subsidies in sectors with overcapacity, and intervention in specific sectors to enable consolidation. That being said, policy makers also toned down the expectation of supply side reform 2.0, asking for a more market driven approach, to avoid price volatility.

Conclusion

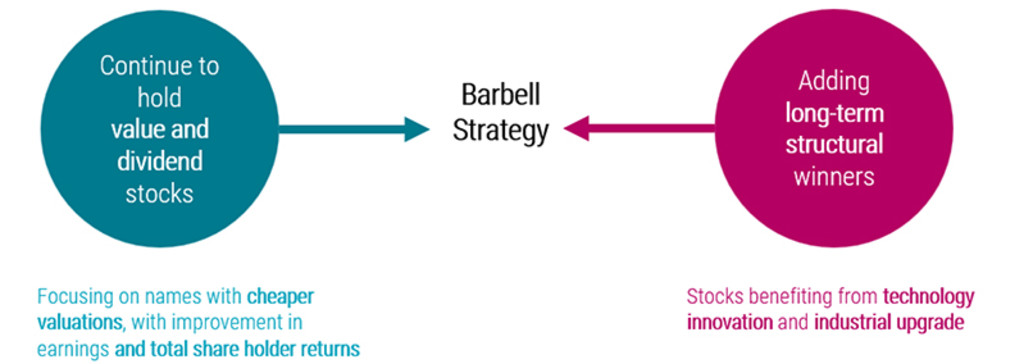

Ahead of the October 2025 meeting, the market will focus on the 15th Five-Year Plan from policymakers rather than short-term stimulus measures. As a result, we aim to position our portfolio toward structural winners in technology and innovation, aligning with long-term strategic priorities. Notwithstanding any final resolution to the trade negotiations with the US, corporate earnings revisions are likely to play a critical role in sustaining the current positive market sentiment through October. Given the persistence of deflationary risks, we will continue to hold value stocks with potential for earnings revisions and improving total shareholder returns as the other side of our barbell strategy during this period.

Get the latest insights

Subscribe to our newsletter for investment updates and expert analysis.