Senior Equity Analyst

• Insight

Europe’s overlooked AI enablers and adopters

AI headlines focus on US-dominated AI models and huge data center builds but that is not the whole story. Europe is quietly constructing and applying the technologies that make AI work. From semiconductor tools and power systems to information technology services and enterprise software, European companies are enabling the AI shift and adopting it in practical ways that create value.

Authors

Top keywords

Summary

- The global AI opportunity is vast but monetization is still uncertain

- High profile AI beneficiaries may not have the highest return potential

- European companies are key beneficiaries both on the enabler and adopter side

The release of the chatbot ChatGPT by OpenAI in late 2022 was an inflection point for AI adoption. Even though modern large language models had already emerged toward the end of last decade and AI applications had been developed and used much earlier than that, ChatGPT enabled interactive natural language conversations for wide audiences. Since then, AI adoption has gone parabolic and the commercial opportunity has started to materialize.

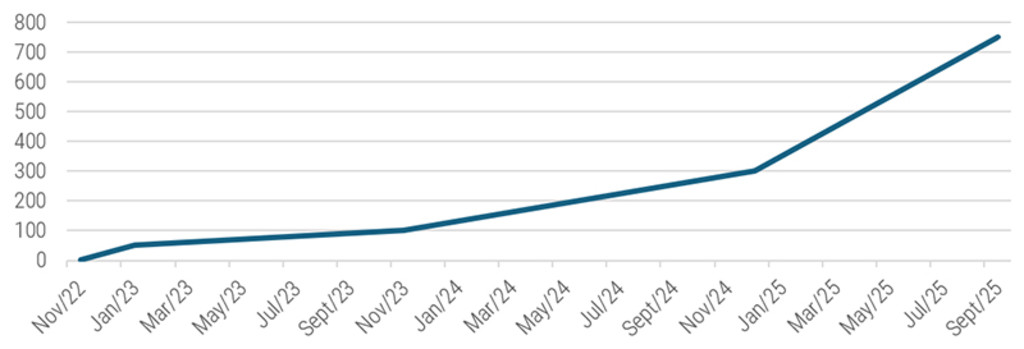

The most popular chatbot ChatGPT reached 1 million weekly active users (WAU) within one month and grew that number to 100 million one year after release. Exponential growth continued over the subsequent years and by July 2025 the chatbot had more than 700 million total WAU. Considering that rival AI models, similar to GPT, have also been launched in the past five years, the scale of AI adoption in this short period of time is incredible.

Figure 1: ChatGPT user growth since launch (WAU in mln)

Source: How People Use ChatGPT (NBER Working Paper Series), September 2025.

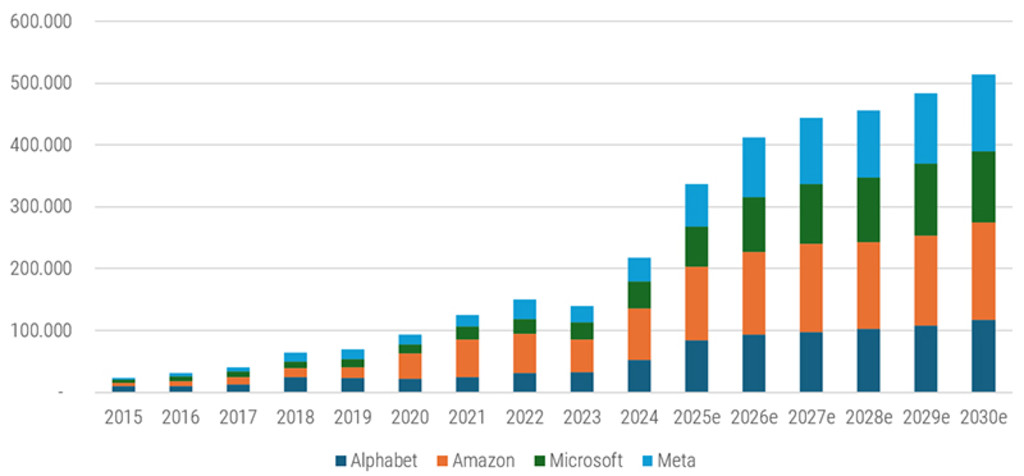

To support high demand for AI solutions, investments into AI infrastructure, both computing power and AI models, have been massive over the past three years and are continuing to rise. It is expected that the four US hyperscalers1 with biggest capex plans Alphabet, Amazon, Microsoft and Meta alone will spend more than USD 350 billion this year and increase their capital expenditure to more than USD 400 billion in 2026. Aggregate spending of the US hyperscalers is expected to reach more than USD 3 trillion over the next four years.

Figure 2: Big Four US hyperscaler capex (USD bln)

The companies mentioned on this chart are for illustrative purposes only. No inference can be made on the future development of the company. This is not a buy, sell, or hold recommendation.

Source: Bloomberg, 15 October 2025.

However, it is uncertain that these large investments in infrastructure will eventually pay off. Dispersion of estimates for the revenue potential of AI model providers, such as Gemini, ChatGPT or Claude are high because both pricing and volumes are difficult to evaluate. Citigroup estimates more than USD 750 billion in revenue by 2030, pointing toward exponential growth.

Europe isn’t missing out, it’s just less visible

It is no secret that IT infrastructure expansion for AI and the development of AI models are being dominated by US companies, while European players are broadly missing in the top ranks. According to the famous “Draghi Report” published in September 2024, around 70% of foundational AI models have been developed in the US since the transformer model architecture (which brought the breakthrough of large language AI models) was invented in 2017. And just the three US hyperscalers account for over two-thirds of the global cloud market.

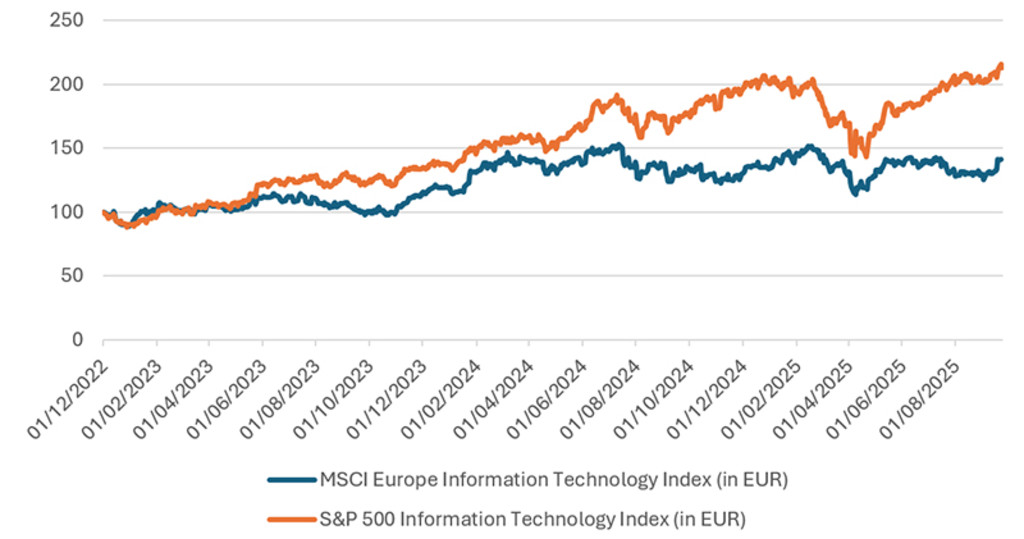

However, Europe is not commercially missing out on AI. European AI beneficiaries don’t share the profile of US hyperscalers but they are benefiting from the enormous amount of capital invested into AI. The much stronger performance of the US IT sector since the release of ChatGPT in late 2022 versus European peers (see Figure 3) is somewhat misleading. Undoubtedly, the breadth of the US IT sector is higher versus Europe, but the strong outperformance is driven by a few highly weighted companies (e.g. Nvidia or Microsoft). And the more than 40% total return of the MXEU Information Technology Index indicates that Europe also hosts many AI winners in its technology sector.

Figure 3: Europe’s tech equities have lagged US peers since late 2022 when ChatGPT was released

Past performance is no guarantee of future results. The value of your investments may fluctuate.

Source: Bloomberg, MSCI, S&P Global, September 2025.

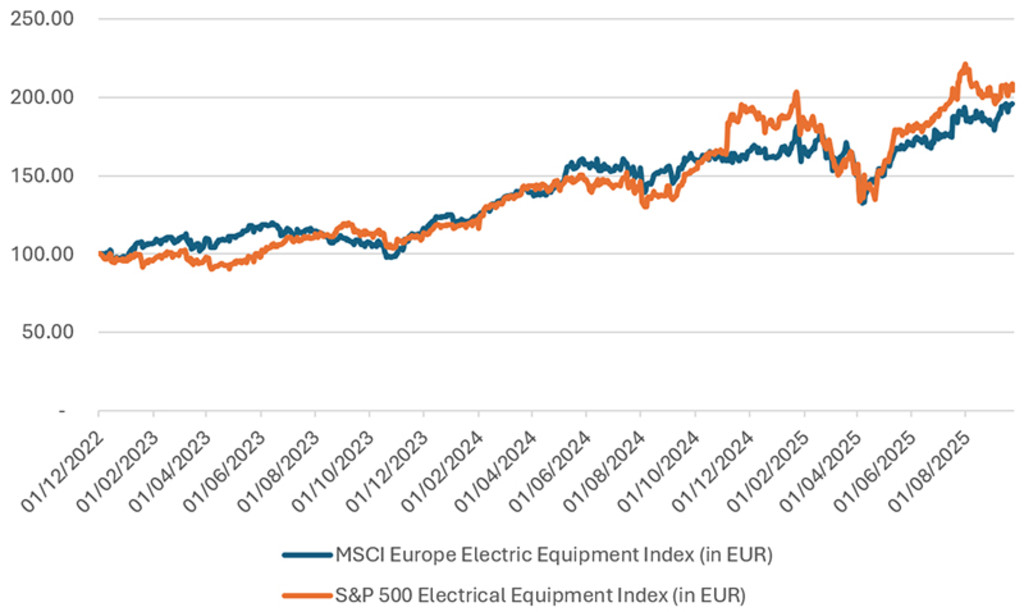

In powering data centers, Europe is more or less at par with US companies. Stock prices of electronic equipment companies on both sides of the Atlantic surged by a similar amount to the US IT sector due to strong AI-related demand (see Figure 4).

Figure 4: Electrical equipment equities have matched US peers as the AI infrastructure buildout ramps up

Past performance is no guarantee of future results. The value of your investments may fluctuate.

Source: MSCI, S&P Global, September 2025.

Enablers and adopters across Europe

To illustrate how European companies benefit from the AI ecosystem we differentiate between AI enablers and AI adopters (see Figure 5). However, in many cases, especially in the information technology and industrial sectors, companies are enablers and adopters at the same time.

The AI enablers include companies which contribute to the AI hardware infrastructure and AI enabling software & services providers. The former provide the hardware infrastructure needed for the high computing demand of AI models and AI applications. Along the value chain this includes not only data center operators, such as the hyperscalers but also semiconductors manufacturers and semiconductor equipment providers, power & cooling solutions providers or communication equipment providers. The latter develop solutions for their clients, which integrate AI into clients’ business processes and products.

The AI adopters are differentiating themselves by proactively integrating AI solutions to enhance their products or services, or to optimize business processes to increase productivity and improve their cost structure.

Figure 5: The AI investment landscape is split with the focus starting to move toward adopters

These are not buy, sell, or hold recommendations. Holdings are subject to change and shown for illustrative purposes only. Future inclusion of these securities in the strategy is not guaranteed, nor can their future performance be predicted.

Source: Alger, Robeco September 2025.

On the enabler side European companies are not as prominent as US peers such as Nvidia and the other well-known mega cap technology companies. However, there are many companies2 and sectors which benefit strongly along the value chain. With ASML, ASM International and Be Semiconductors, Europe houses three leading semiconductor equipment companies. In addition, companies such as Schneider Electric, Halma and Belimo have seen their earnings grow considerably due to data center infrastructure investing. Energy solution providers, such as Siemens Energy, have also benefited, making sure that the power-hungry data centers are fed. Europe’s many leading companies within the renewable energy value chain are also likely to be indirect beneficiaries as pressure for sustainable energy sourcing will increase.

In AI adoption, many European companies are also leading. SAP, for example, is emerging as both a leading enabler and adopter. Companies such as Relx or Wolters Kluwer, which have integrated AI solutions into their product offerings are also potential AI beneficiaries. Early or fast adopters of AI solutions within their own operations achieve a competitive advantage over their peers through lowering production costs or through more efficient and effective innovation. Retail is a good example for cost and sales optimization through AI while Europe’s large pharma sector can use AI to help accelerate the pace of innovation. Finally, AI can help European companies to lower the manufacturing cost gap versus Asian and US peers, as considerably higher costs for labor can be substituted by AI.

European Stars Equities D USD

- performance ytd (31-3)

- -5.40%

- Performance 3y (31-3)

- 8.67%

- morningstar (31-3)

- SFDR (31-3)

- Article 8

- Dividend Paying (31-3)

- No

Past performance is no guarantee of future results. The value of the investments may fluctuate. Annualized (for periods longer than one year). Performances are net of fees and based on transaction prices.

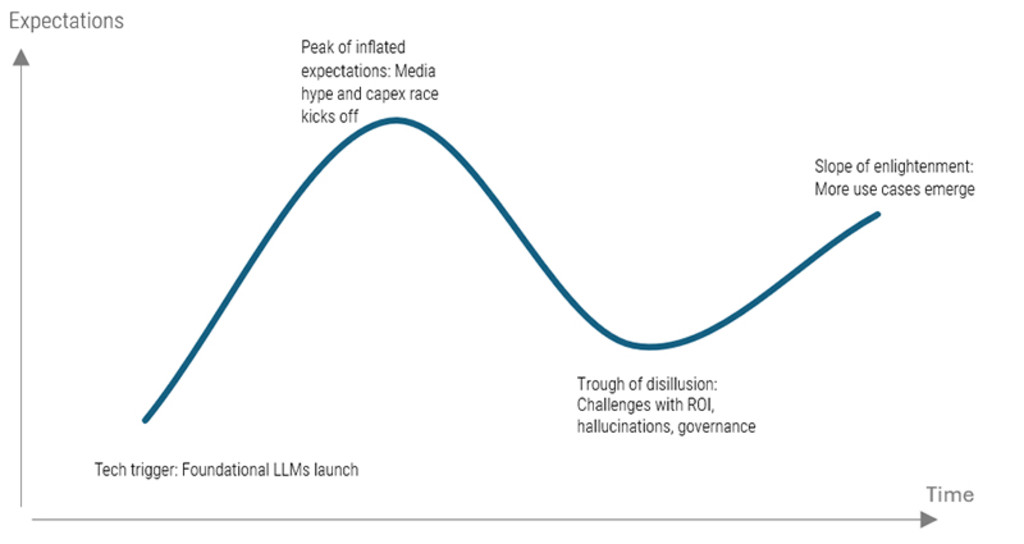

The hype cycle and why timing matters

However, as with every major shift in technology, perceived winners can turn into incremental losers if the transition is not managed appropriately. Therefore, assessing the idiosyncratic aspects of every company is essential.

AI will be here to stay, but the adoption curve will not be straight. According to industry experts, AI adoption is currently in the ‘peak of inflated expectations’ phase and entering into the ‘disillusion phase’ as early adopters see limitations of AI benefits. This means there is plenty of opportunity ahead, but at some point a digestion period, after heavy early investments, is likely. The statement by Alphabet CEO Sundar Pichai that “…the risk of underinvesting is dramatically greater than the risk of overinvesting…” (Q2 2024 earnings call) implies that a slowdown after an initial strong spending phase is rational to think of.

Figure 6: The AI hype cycle

Source: Gartner, Robeco.

Conclusion

There are plenty of AI beneficiaries in Europe along the value chain, even though they might not be as visible as their US peers. Investing in those companies offers great longer-term opportunities, albeit, with short-term risk of a digestion period after initial heavy investments in AI have been made. Through this potential period of AI overcapacity, European AI exposed companies, which do not have to bear the depreciation risks of the enormous upfront capital expenditure could offer better return potential than for example US data center capacity providers.

AI will go through phases of hype and consolidation, but its long-term trajectory is clear. European companies, whether as enablers or adopters, are well positioned to capture value. Their role is less visible than that of US mega-caps, but no less essential. That is one reason why we believe today is a compelling time to allocate to European equities. Through our European Stars strategy, investors gain access to high-quality European companies that stand to benefit from the AI transformation, combining structural growth potential with strong fundamentals and attractive valuations.