Portfolio manager, Boston Partners

• Insight

Defense and financials bring strong run for value strategy

Stock picking in defense and European financials has allowed the Robeco Boston Partners Global Premium Equities strategy to enjoy a strong run this year.

Authors

Summary

- Defense firms to benefit from ReArm Europe and NATO targets

- European banks have enjoyed good cash flow and interest margins

- Global Premium Equities remains overweight Europe and underweight US

The defense sector has outperformed the rest of the stock market since the beginning of 2025, with price-to-earnings multiples in the aerospace and defense industry rising from 23.8 times in December of 2024 to 27.6 times by the end of June. This success follows the reappraisal of defense spending in Europe after Russia invaded Ukraine, leading the EU to allocate EUR 800 billion in a ReArm Europe initiative in 2024.

ReArm Europe runs in tandem with President Trump’s calls for the 32 NATO members to increase defense spending to at least 2% of GDP, rising to 5% by 2035 under an agreement signed at the NATO summit in The Hague in June 2025.

From the sustainable investing perspective, the defense spectrum is subject to strict exclusions banning investments in controversial weapons like cluster bombs. However, mainstream defense investing has always been possible for the majority of Robeco’s strategies, so long as a company is not involved in severe ESG controversies.

Priced for perfection

“We’ve always had defense exposure in the strategy over the long term,” says Chris Hart, Portfolio Manager of Global Premium Equities since 2008. “Defense in Europe became a theme very quickly last year, and we had good exposure to the sector as this emerged, both in the US and in Europe.”

“All those stocks, in my view, have now become full value, or even expensive. They’re still pricing in a significant increase in European defense spending as a percentage of GDP. So, it will be interesting to see over the next several months how much of that comes to fruition; Spain is already balking at 5% of GDP.”

“I would say that across Europe and even in the US, Europe is priced for perfection in defense, while the US is fair to full value. I don’t really see significant opportunities in the defense industry entering the portfolio anytime soon.”

Rheinmetall reveille

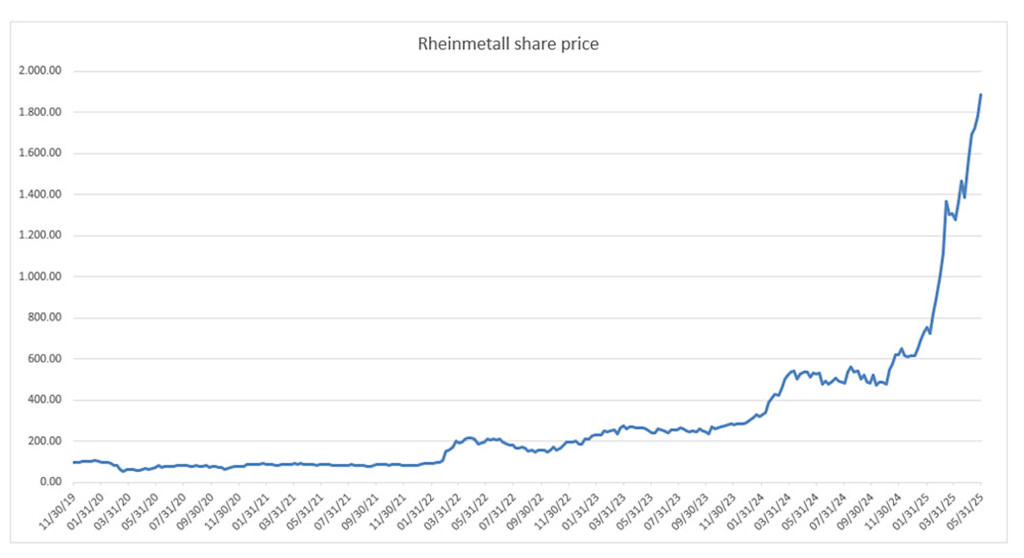

The top individual contributor in the defense space for the strategy was Rheinmetall. The German firm makes tanks, armored vehicles and ammunition alongside a significant civilian engineering and robotics business. The strategy first bought Rheinmetall stock in November 2019 at around USD 100 per share. The position added notably over the holding period, even prior to the Russia/Ukraine conflict.

“Rheinmetall was bought and added to over time because it offered great value, with consistent long-term free cash flow generation and a stabilizing mix of industrial and defense exposure,” Hart says.

The shares hit USD 200 in early 2022, USD 500 in early 2024, and USD 1,500 in early 2025, as the company saw massive spending commitments on contract wins from rising NATO defense spending rises.

Figure 1: The amazing rise of Rheinmetall’s share price

The value of your investments may fluctuate. Past results are no guarantee of future performance.

Source: Facstet, Robeco Boston Partners. Figures are in euros. All data to 31 May 2025.

Reaching a peak

“While much of the rise in the share price is deserved, it has now peaked, and is priced for not only continued spending increases, but for ongoing long-term conflicts which are not guaranteed,” Hart says.

“So we decided to sell the stock in the second quarter, as its price-to-earnings ratio has soared. It still reflects strong quality and momentum, but our approach will always remain price-sensitive.”

The stock’s sale made way for other new positions across the all-cap global universe that Hart selects securities from.

“Not many investors want to talk about names outside of the Magnificent Seven, but Rheinmetall has easily outpaced Nvidia in recent years,” he says. “Through our bottom-up stock picking, we aim to continue to fill our portfolios with underpriced businesses that can outperform, whether they are in the headlines or not.”

From tanks to banks

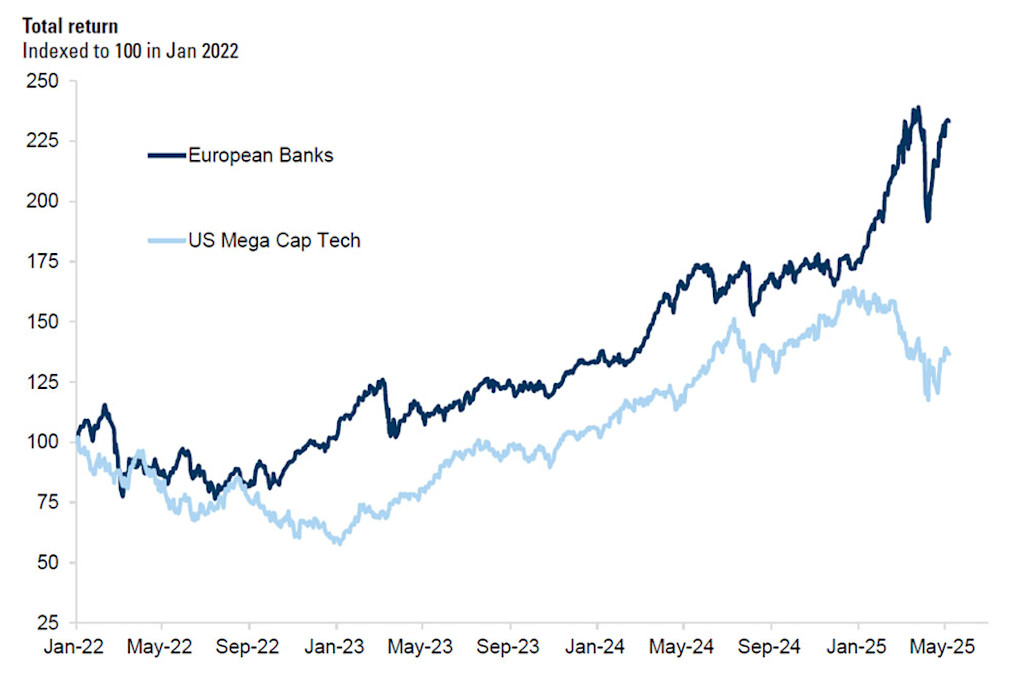

Another success story has been the once troubled European banks, which have also outperformed the general market for the past year thanks to strong cash flows, increasing profitability, strong balance sheets, and good prospects for future lending margins.

“We’re still significantly overweight European financials, but it wasn’t always like this due to regulatory overhangs that changed significantly over the last four to five years,” Hart says. The strategy historically has been underweight European financials for the majority of its existence.

“Today, they still provide a significant amount of value in the portfolio – not as much as they did say a year ago, but they’re still very interesting from the three circles perspective.”

Outpacing the mega-caps

“The banks that we own for the most part are in spread lending – traditional banks that earn the overwhelming majority of their net interest income from lending and not trading. They are very well positioned from a hedging perspective, regardless of what occurs with the yield curves going forward.”

Such has been the success of European banks that they have outpaced US mega-cap tech stocks since the middle of 2022, as seen in Figure 3 below:

Figure 2: European banks outpace US mega-cap tech stocks

Past results are no guarantee of future performance. The value of your investments may fluctuate.

Source: Datastream, Goldman Sachs Global Investment Research. All data to 31 May 2025.

Going through an air pocket

However, rates are now falling after the European Central Bank cut the base rate across the 20-nation eurozone to 2% from 2.25% on 5 June, citing fears of economic slowdown that a defense spending surge could theoretically exacerbate.

“We think this year is somewhat of an air pocket where interest margins might deteriorate somewhat as interest rates go down,” Hart says. “But we’ve done a lot of work on 2026 and 2027 numbers, and we still see net interest margins remaining very favorable going into 2027.”

“We see earnings based on low single-digit loan growth. There’s no signs of credit deterioration in Europe or the US; historically you get credit issues when you have excessive amount of lending.”

“But over the last six to seven years, there hasn’t been an excessive amount of loan growth, either in the US or in Europe. Lending is probably pretty stable and credit quality has not shown a significant deterioration.”

“Importantly, they also continue to return a significant amount of capital, both through share buybacks and dividends.”

For more on the value concept, tune into our podcast with Chris Hart.

Get the latest insights

Subscribe to our newsletter for investment updates and expert analysis.

Important information

The contents of this document have not been reviewed by the Securities and Futures Commission ("SFC") in Hong Kong. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice. This document has been distributed by Robeco Hong Kong Limited (‘Robeco’). Robeco is regulated by the SFC in Hong Kong. This document has been prepared on a confidential basis solely for the recipient and is for information purposes only. Any reproduction or distribution of this documentation, in whole or in part, or the disclosure of its contents, without the prior written consent of Robeco, is prohibited. By accepting this documentation, the recipient agrees to the foregoing This document is intended to provide the reader with information on Robeco’s specific capabilities, but does not constitute a recommendation to buy or sell certain securities or investment products. Investment decisions should only be based on the relevant prospectus and on thorough financial, fiscal and legal advice. Please refer to the relevant offering documents for details including the risk factors before making any investment decisions. The contents of this document are based upon sources of information believed to be reliable. This document is not intended for distribution to or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Investment Involves risks. Historical returns are provided for illustrative purposes only and do not necessarily reflect Robeco’s expectations for the future. The value of your investments may fluctuate. Past performance is no indication of current or future performance.