April 24, 2026

SFDR 2.0 – All you need to know

The EU’s Sustainable Finance Disclosure Regulation (SFDR) is getting a major update. Known as SFDR 2.0, as it follows the sweeping regulation that was first implemented in 2021, it will affect all asset managers operating within the 27-nation union once it is implemented.

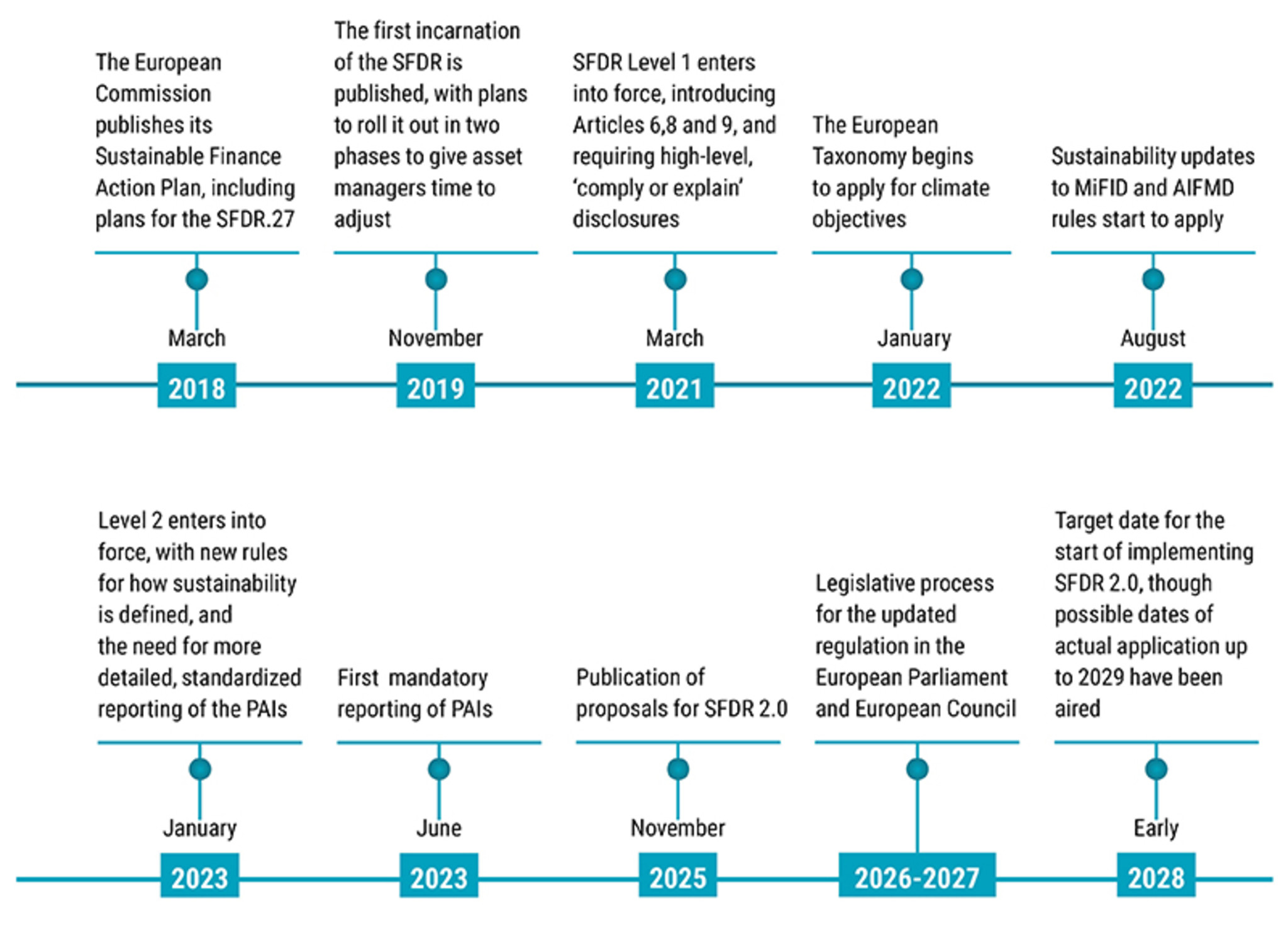

The proposal for SFDR 2.0 was published by the European Commission in November 2025 and will now need to go through the full EU legislative process before coming into force. The earliest possible application date is expected to be around the beginning of 2029, but this will depend on how quickly the negotiations go.

The likely timeline is shown below. However, it should be noted that the regulatory trajectory is long, politically sensitive, and subject to intense scrutiny from within the EU. It is therefore not guaranteed that the current proposal will remain in its present form, or that it will be enacted at all.

Figure 1: SFDR 2.0 projected timeline

Source: EU, Robeco, 2026.

The introduction of labels

The SFDR classification into articles was originally meant to define transparency rules for sustainable and ESG funds. But they have de facto been (mis)used by the market as categorizations for the level of sustainability in an investment fund. SFDR 2.0 intends to remedy this.

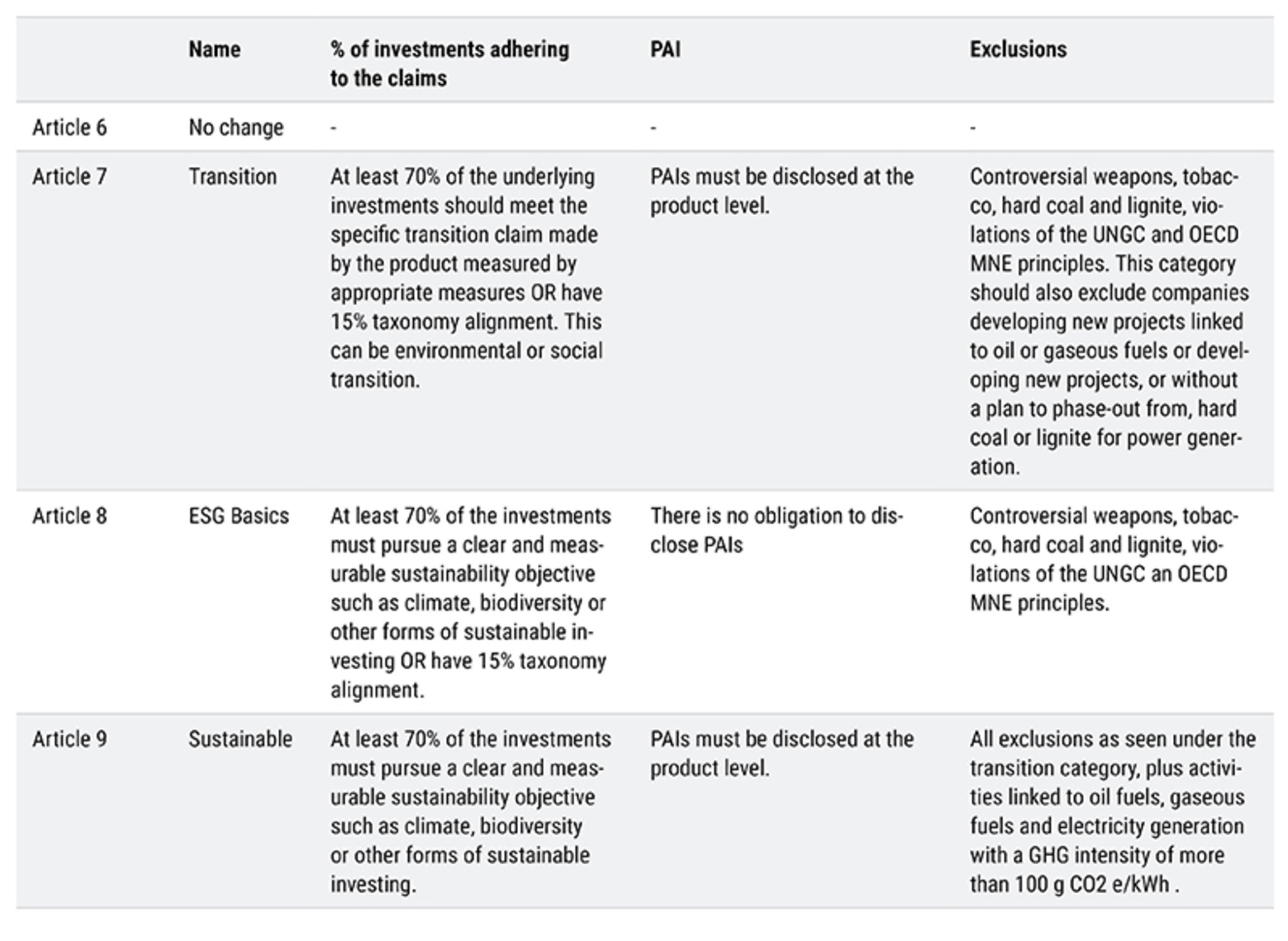

The revised regulation introduces a new product categorization system with three labels, ’ESG Basics’, ‘Transition’ and ‘Sustainable’. The Basic category will replace Article 8 requirements while Sustainable will replace Article 9, and a new Article 7 will be introduced for the Transition bucket. Article 6 for no use of ESG stays the same. Each category comes with a set of eligibility criteria, including minimum investment commitments and mandatory exclusions, outlined in the table below.

More flexibility and less reporting

Another major change is that the need to report the Principal Adverse Impact (PAI) indicators will be removed at the company level and significantly simplified at the fund level. PAIs were introduced in the original SFDR to require investors to calculate the impact that their investments in companies had on the wider world – the ‘double materiality’ principle. But they are complex and often difficult to reliably report.

Disclosure templates will also become shorter and easier to understand, with fewer indicators and simplified consumer facing information.

SFDR 2.0 also removes the prior definition of ‘sustainable investment’, as opinion still widely differs among asset managers as to what this actually means, while keeping the underlying concepts in place through the criteria applicable per label. Overall, SFDR 2.0 aims to reduce complexity, cut the reporting burden, and enhance clarity and trust in sustainability related claims.

The new Article 7 for transition funds

The new Article 7 category will be introduced for funds which invest in companies in transition to a more sustainable business model, such as by decarbonizing or cutting their emissions. Socially progressive transitions are also covered by the new category. Its introduction answers criticism in the original regulation that there was not a specific category for these type of funds. Investing in things that are already sustainable does make the world better, but targeting those that are transitioning towards more sustainable practices actually can make the world even better, and faster.

Technically, Article 7 already exists, but does not refer to fund classification. Instead, it houses the PAI criteria for application across the other Articles. Under SFDR 2.0, it becomes the new Transition bucket.

Thresholds for sustainability

What counts as being sustainable has long been the subject of debate among investors, and the content of a fund that needs to meet often fluctuating criteria was not addressed in the original SFDR. To try to make things clearer, the European Securities and Markets Authority (ESMA) published new guidelines in June 2024.

ESMA said that funds using sustainability-related terminology in their marketing or branding must use at least 80% of their underlying investments in companies to pursue the environmental or social sustainable investment claims in accordance with the investment strategy. This can be decarbonizing or cutting emissions, which can be measured according to standard metrics such as Scope 1,2 and 3 emissions, and can include not only environmental but also social objectives. In the UK, the threshold was set at 70%. SFDR 2.0 follows the UK example and sets it at 70% contribution threshold for all the new ESG Basics, Transition and Sustainable categories.

Exclusions per classification

The current SFDR doesn't explicitly require any exclusions, although Article 8 funds can only invest in companies that follow ‘good governance’, which effectively means excluding the companies that don’t. Article 9 funds require 90% of the underlying investments to be sustainable, where the investee company contributes to a measurable sustainability objective (such as climate) and follows the principle that the investment ‘does no significant harm’ (DNSH) to any other objective. The DNSH practice also effectively leads to the application of exclusions.

SFDR 2.0 tightens the rules for all investment products, as it introduces mandatory exclusions for all three ESG Basics, Transition and Sustainable buckets, the strictest of which will apply to the Article 7 Transition and Article 9 Sustainable categories. The proposed thresholds for these are shown in the table.

What about Article 6?

The basic principles behind Article 6 (zero intended sustainability, but sustainability risk incorporation) remain broadly the same. The classification can be used though by asset managers who want to offer funds that deliberately do not try to pursue ESG goals, or which target sectors subject to exclusions, such as ‘sin stocks’ offering exposure to tobacco companies, for example. Funds extensively using derivatives – assets whose value is based on the value of an underlying asset, and so are not direct owners – also are usually categorized as Article 6.

Robeco’s approach

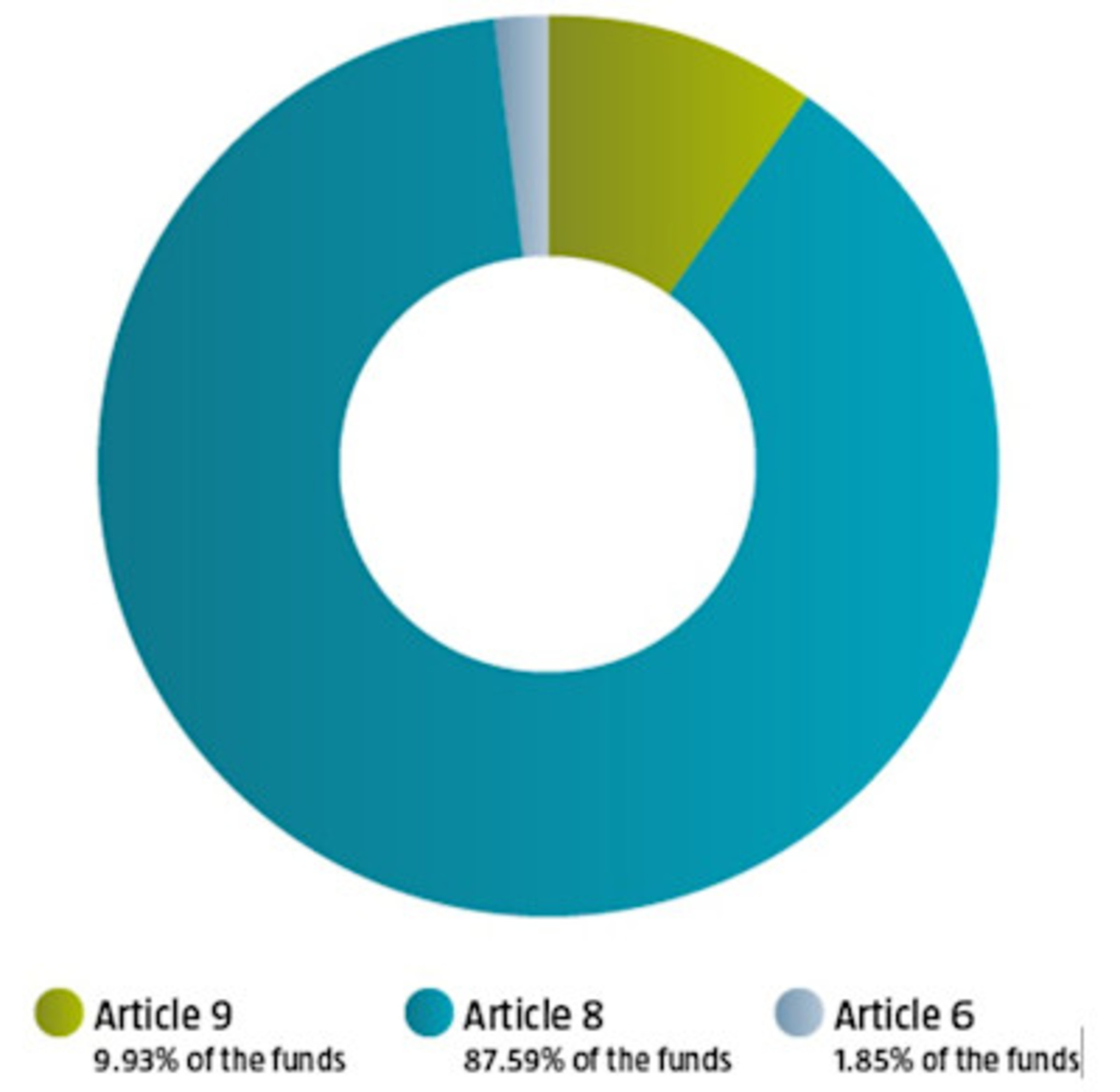

Until SFDR 2.0 comes into force around the beginning of 2029, the existing regime continues to apply. Robeco’s current mix of Article 6,8 and 9 funds is as follows:

Article 6 – 1.9%

Article 8 – 87.6%

Article 9 – 9.9%

Source: Robeco, March 2026

Our view on the proposal

SFDR 2.0 aims to reduce complexity, cut the reporting burden, and enhance clarity and trust in sustainability related claims. We believe the proposal will succeed in most of these elements in the long run. Most importantly, setting credible standards for the sustainability classification of funds. However, in the near future, the proposal will require asset managers to undertake substantial update processes, following the considerable efforts already made at the time of the initial SFDR implementation.

In our view the most important point of attention is the lack of a fully level playing field between categorized products and non-categorized products. Asset managers that manage sustainability-related funds (Articles 7,8 and 9) will continue to face more extensive reporting obligations than managers of funds without sustainability characteristics.

Given that one of the aims of the legislation is to facilitate capital flows towards sustainable investments, this might be the biggest criticism to be placed on this proposal. To achieve this goal, it would be wise to set similar reporting requirements on sustainability characteristics for all funds.