Client Portfolio Manager

• Insight

Quant chart: Same manager, different alpha

Allocating to one manager across developed and emerging markets can still provide meaningful diversification of active return.

Summary

Asset owners often allocate to multiple managers to diversify sources of active return. That logic is sound: if one manager underperforms, another may offset it, especially when their investment styles, processes, or opportunity sets differ.

But diversification doesn’t only exist between managers. It can also exist within a single manager, when a comparable investment philosophy is applied across different market universes.

This raises an important question around portfolio construction: if an investor allocates to the same manager in developed markets (DM) and emerging markets (EM), are they simply doubling up on the same source of alpha – or can they still achieve meaningful diversification?

Our analysis suggests they can. Even when the same manager runs comparable strategies in both DM and EM, the alpha generated in those portfolios tends to be only weakly correlated. In other words, the same manager does not necessarily mean the same return pattern.

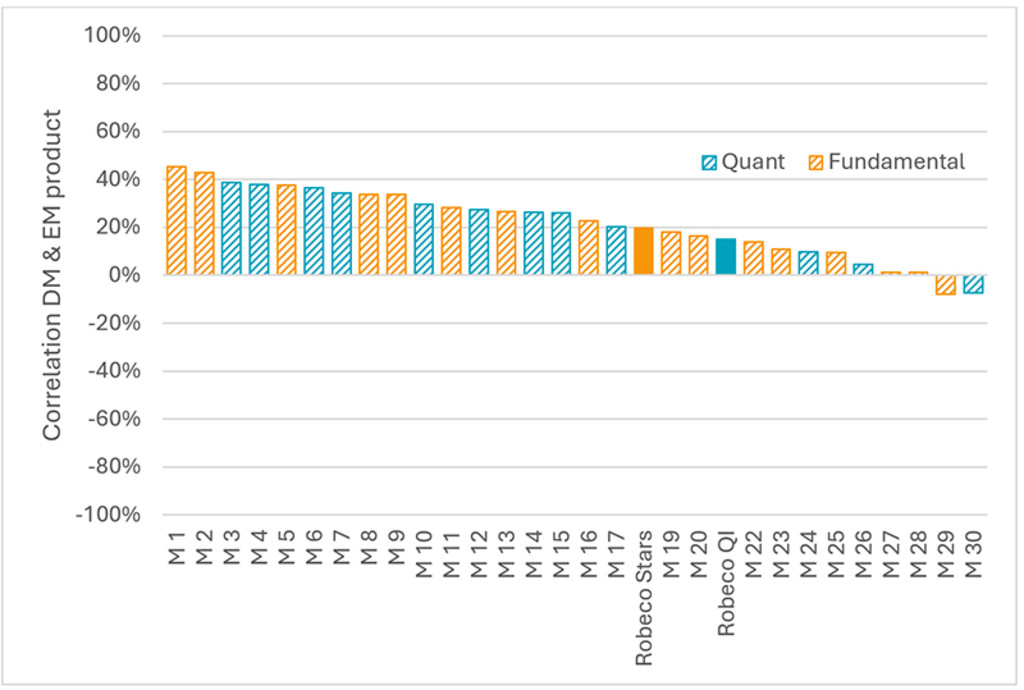

Using eVestment data, we examine whether comparable DM and EM strategies from the same asset manager deliver similar alpha. We analyze 30 managers, covering both quantitative strategies (e.g. Robeco QI DM Enhanced Indexing versus Robeco QI EM Enhanced Indexing) and fundamental strategies (e.g. Robeco Global Stars versus Robeco EM Stars). For each DM–EM pair, we compute the alpha correlation using the maximum available overlapping history between 2005 and 2025.

Figure 1 | Alpha correlation between EM and DM products per manager

Past performance does not guarantee future results. The value of your investments may fluctuate.

Source: Robeco, eVestment, 2005-2025. For illustrative purposes only.

Quant Charts

The results show that the average alpha correlation across managers is approximately 0.2, with correlations ranging from close to 0.0 to around 0.4. This indicates some commonality, but limited overlap in alpha generation. Importantly, the pattern is similar for both quant and fundamental managers.

That finding is intuitive once we consider the underlying opportunity sets. DM and EM equity markets differ materially in market structure, liquidity, sector composition, analyst coverage, governance regimes, and the way information is incorporated into prices. As a result, even when a manager applies a similar philosophy or research framework across both universes, the actual sources of excess return are often not the same.

For quant strategies, investment signals may remain conceptually consistent across markets, but their strength, persistence, and implementation can vary significantly. For fundamental strategies, company selection opportunities, market inefficiencies, and macro sensitivities also differ. The result is that active returns can follow meaningfully different paths across DM and EM, even under one investment house.

Low alpha correlation also suggests that periods of underperformance may not coincide. In practice, this means a manager’s DM and EM strategies may experience drawdowns at different times and for different reasons. For asset owners, that can help smooth the overall experience of active returns across a broader equity allocation.

Diversification without fragmentation

This matters because many asset owners face a trade-off between diversification and complexity. Adding more managers can broaden return sources, but it can also increase governance burden, due diligence requirements, reporting complexity, and the risk of unintended inconsistencies across portfolios.

Allocating to one manager across multiple universes may offer a different route: operational simplicity without necessarily giving up diversification of alpha. Where relevant, this can also support greater consistency in portfolio design, e.g. in the treatment of sustainability preferences or climate objectives, while still allowing the active return profile to differ across markets.

This may be particularly relevant for asset owners considering broader global equity structures, including combinations of DM and EM within an overall ACWI-oriented allocation.

Bottom line: same manager does not mean same alpha

Even when the investment process and the manager are the same, DM and EM strategies tend to generate largely distinct alpha. Allocating across universes can therefore provide meaningful diversification, without the need to change managers or philosophies.

For asset owners, that means manager consolidation does not automatically imply return concentration. In some cases, a single manager relationship can offer a combination of diversified active return streams, implementation consistency, and lower operational complexity.