Strategist

• Monthly outlook

The share buyback’s rise sees the dividend’s demise

Share buybacks have replaced the traditional dividend as the most popular means of returning capital to investors, says Robeco’s Investment Solutions team.

Authors

Client Portfolio Manager

Top keywords

Summary

- Share buybacks have become the preferred method of returning capital

- Relief after planned withholding tax in US ‘Big Beautiful Bill’ was scrapped

- Flows seen moving from credit to equity income as bond yields fall

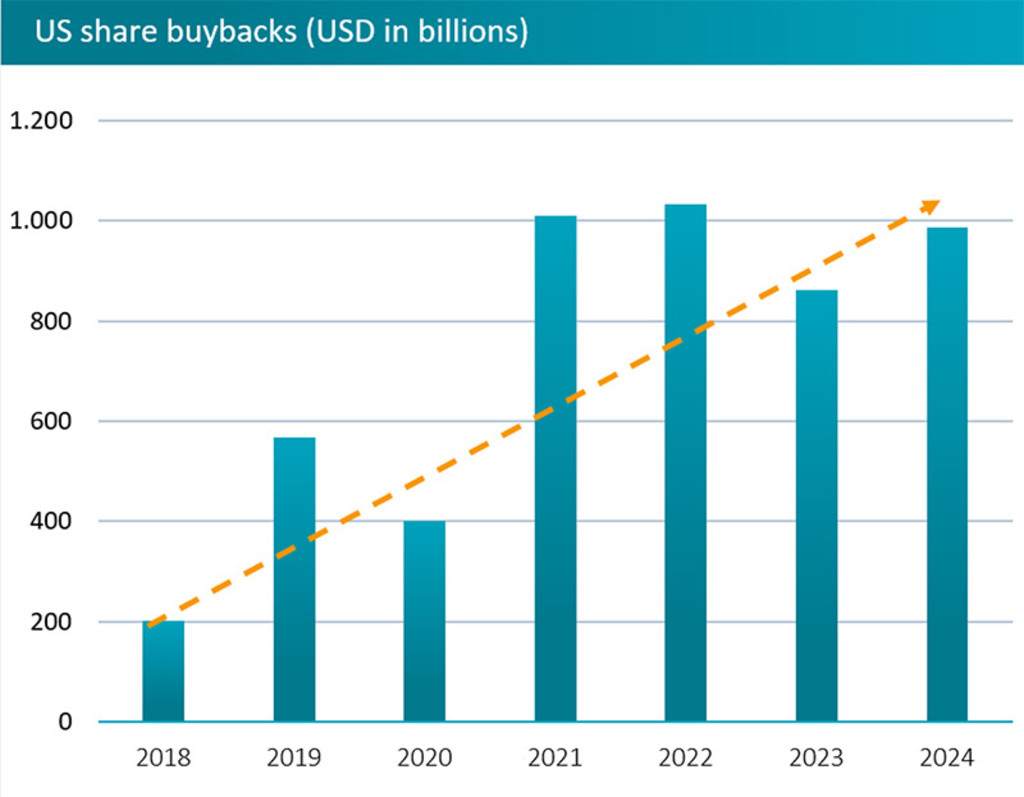

Share buybacks have risen in value to reach USD 1 trillion a year in the US since 2021, serving the twin purpose of saving the need for recurring cash payouts through dividends while artificially raising earnings per share and the share price itself at the same time. They also have tax advantages in certain jurisdictions.

Annual dividends have been paid as a percentage of shareholdings as the more traditional means of distributing a company’s profits for centuries, the first known payout being made by the Dutch East India Company in 1602. They are often viewed as a symbol of a company’s health, where cuts in the payout indicate that the firm was struggling to make profits, and are seen as inflexible.

“At a structural level, companies have broadly increased their preference for share buybacks since 2008,” says Jonathan Arthur, Client Portfolio Manager with Robeco Investment Solutions. “This is partly because share buyback programs are more flexible and often have finite timelines. It also puts less pressure on management teams from the uncertainty associated with other options such as investment or M&A.”

“There is typically a very negative price reaction to any cut in the dividend – so companies are less willing to raise dividends after periods of strong earnings.”

“The ratio between dividend yields and share buybacks can be dependent on individual country tax regimes. In the US, share buybacks are generally considered more tax-efficient than dividends because of how they are taxed.”

Source: Robeco, Bloomberg, July 2025.

Outside the US, share buybacks have also increased in Japan and Europe. They accelerated in Japan after the Tokyo Stock Exchange announced in March 2023 that companies should do more to improve their return of capital to shareholders, resulting in average payout ratios rising from 57.1% in 2023 to 67.4% in 2024.

“We may now expect higher dividends and higher share buybacks in Japan if this focus on capital efficiency continues,” Arthur says. “But the better value is arguably in Europe. One of the conclusions from our capital market assumptions in our five-year Expected Returns outlook is that European equities offer more attractive relative valuations versus other developed markets.”

“More modest European valuations have supported a growth in share buyback programs in Europe. If European companies believe their share prices are structurally undervalued against other regions, it may make sense for them to continue to deploy their excess cash to buybacks.”

“For now, buybacks have been concentrated in banks and energy companies, but this may start to spread to other sectors, as we see a more disciplined approach to capital allocation in Europe.”

5-year Expected Returns 2026-2030

The Stale Renaissance

Big beautiful policy change

Meanwhile, investors have breathed a sigh of relief that a planned withholding tax on dividends paid to foreign investors contained in the ‘Big Beautiful Bill’ was scrapped. Members of the US Congress balked at the prospects of encouraging even more capital flows from the US if it had been enacted.

“After the weaponization of the dollar at the start of the war in Ukraine and Trump’s aggressive tariff policy, US exceptionalism is under the spotlight like never before,” says Peter van der Welle, strategist for the Investment Solutions team.

“Some investors have already started voting with their feet, as highlighted by a decrease in US foreign direct investment and a fall in the number of foreign holders of US equities.”

“A dividend withholding tax for international investors as proposed under Section 899 of the ‘Big Beautiful Bill’ would have made US stocks less attractive, and negatively impacted our longer-term returns expectations for US equities. The section was removed as one of many compromises as it went through Congress, which was wary of encouraging a structural shift away from US assets.”

“The quite sudden repeal of this so-called ‘revenge tax’ underlines the importance of investors not overreacting to initial Trump policy proposals, since they have a tendency to be watered down or scrapped, and are ultimately becoming less material.”

Dividends versus bond coupons

With the withholding tax threat gone, investors will likely continue to switch from bond yields to the regular income still offered by dividends, Arthur says. While dividends tend to consistently go up, bond yields have been going down due to interest rate cuts.

“For investors seeking a regular cash payout (such as retirees), both bond coupons and dividends are seen as appealing,” Arthur says. “As interest rates and interest rate expectations have started to fall, we see the migration from credit to equity income as shown by fund flows over the past 18 months.”

“At this stage of the market cycle, income overlay strategies such as using covered call options to take advantage of future price rises are starting to look more attractive. In periods of higher volatility, and if premiums look attractive enough, we will look for tactical opportunities to sell call options within our income strategies. While this does reduce upside, it can enhance income, offer more stable return distributions and provide some downside protection.”

Get the latest insights

Subscribe to our newsletter for investment updates and expert analysis.