Head of Multi Asset & Equity Solutions, Co-Head Investment Solutions

• Monthly outlook

Financials – riding the wave or getting washed away?

Financial companies are set to benefit from a wave of tailwinds, though stock picking is essential to find the best opportunities, Robeco’s active investors say.

Authors

Portfolio Manager

Summary

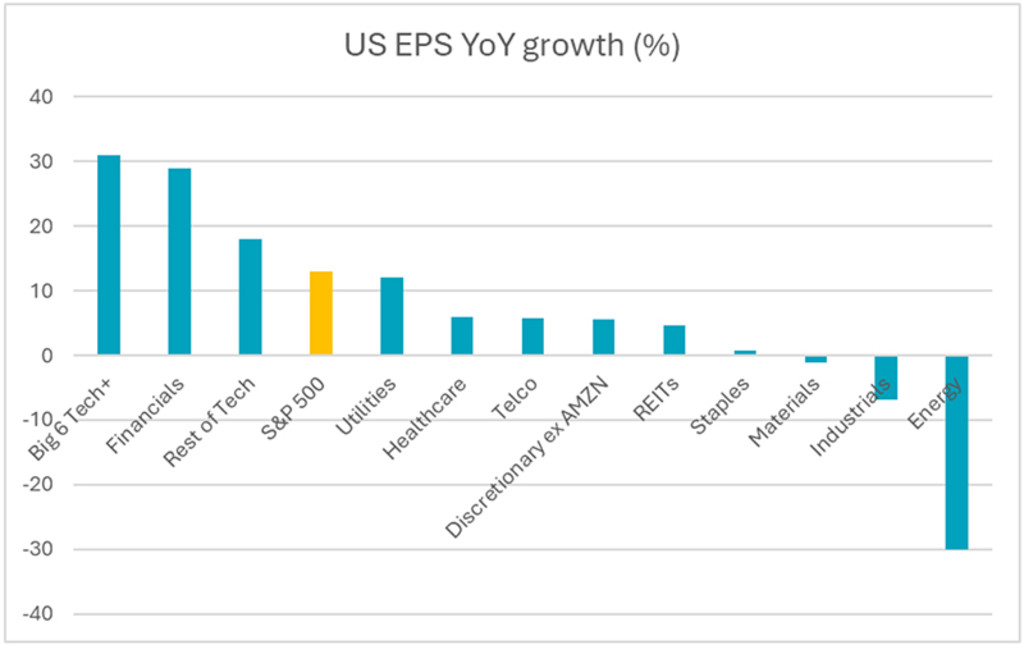

- Banks have the second-best earnings growth behind Big Tech

- Fintech and an M&A consolidation wave set to benefit the sector

- Cuts to regulation and red tape likely to benefit the US vs. Europe

Banks have beaten the main benchmarks this year, with US financials becoming the second-best earners behind the Big Tech firms. And the best may be yet to come, as innovative financial technology continues to mold the future of finance, the US banking sector faces a string of mergers, and European financials begin to deliver positive performance, our multi-asset and fintech investment teams say.

“The financial sector is currently benefiting from several positive factors,” says Colin Graham, Head of Robeco Sustainable Multi-Asset strategies. “Interest rates and economic activity are expected to remain higher for longer, which supports the profitability of financial institutions.”

“US financials have been delivering earnings, and while they are behind Big Tech, they are still clearly ahead of the S&P 500. Not surprisingly, we have seen a significant rally in the debt and equity sectors over the last 12 months. One note of caution is that we think much of the good news is priced in, and so is no longer ‘cheap’ relative to history at an index level, though active management can still find the best picks within the sector and relative to others.”

“Looking forward, capital markets are becoming more active, with a strong pipeline of M&A deals and initial public offerings (IPOs), through deregulation promised in the US across industries and within the banking sector. Europe remains a laggard here and is unlikely to benefit from the relaxation of regulation, but the continent does have a tailwind of lower funding costs as the European Central Bank (ECB) cuts rates.”

US financials are the second-best performers on earnings per share growth. Source: Robeco, UBS.

Much depends on regulation, which is expected to be slashed in the US but remain high in Europe, and the future path of interest rates that dictate net interest margins – the difference between the rates at which banks lend to borrowers and pay out to savers.

“We are seeing better-than-expected economic activity in Europe and China, so we need the US economy to slow, though the probability of recession remains low,” Graham says. “Slower US growth will allow interest rates to drift lower, supporting net interest margins – one of the key measures needed to support profitability.”

“Loan demand remains anaemic outside the consumer sector, with much of the demand fulfilled by private credit, which benefits from a lower regulatory burden. We should note that the higher-for-longer US rate outlook with rising lending standards supports more expensive financial debt securities such as AT1s and the contingent convertibles (CoCos).”

FinTech XH CHF

- performance ytd (31-3)

- -17.77%

- Performance 3y (31-3)

- 4.81%

- SFDR (31-3)

- Article 8

- Dividend Paying (31-3)

- No

- Current Price (6-5)

- 91.13

Past performance is no guarantee of future results. The value of the investments may fluctuate. Annualized (for periods longer than one year). Performances are net of fees and based on transaction prices.

An M&A bonanza

One of the biggest tailwinds is the expected consolidation in the US banking sector, which has hundreds of small, regional banks whose business models have been disrupted by fintech firms, and who may be too small to survive without mergers.

“Since the US election, excitement in M&A teams is at fever pitch in anticipation of a much more permissive regulatory regime under Trump 2.0, with the financial sector in general, and global fintech in particular, likely to be in focus for dealmakers,” says Patrick Lemmens, Portfolio Manager of the Robeco Fintech and New World Financials strategies.

“Looking ahead, we see the pipeline for M&A deals and IPOs as significant tailwinds for overly fragmented US regional banks, and also for Chinese banking and property consolidation. While some politicians have voiced objections, the strong desire from the ECB to have more cross-border mergers should ultimately lead to M&A heating up and getting done in the European financials landscape.”

Get the latest insights

Subscribe to our newsletter for investment updates and expert analysis.

Targeting the underbanked

Another tailwind is the new business that could be gained bringing banking services to millions of people who don’t have bank accounts.

“While the use of environmental, social and governance (ESG) factors may be facing headwinds in the US, the social benefits of banking are undeniable, so financial inclusion and servicing the under-banked are trends that are here to stay,” Lemmens says.

“The emerging finance trend focuses on the growth of the global middle class, especially in emerging markets, where financial penetration is still low. On top of that, you have the digital finance trend where fintech companies offer smart digital solutions to customers with no bank account or who receive poor banking services.”

This can also be seen in the US, following a survey conducted by the Federal Deposit Insurance Corporation (FDIC) in 2023 to discover who holds no bank account (unbanked), or who owns an account but uses alternative financial services (underbanked). The results are shown in the table below:

Taking an active approach

So, where to find the best picks? Here, targeted stock picking is essential as fintech continues to disrupt the system, while M&A offers opportunities and an aging population creates more demand for financial services in general, Lemmens says.

“The rapid pace of fintech evolution requires an active investment approach,” he says. “We prefer fintech companies operating from one technology platform, with superior software that means they can operate at much lower costs than rivals, and certainly cheaper than traditional banks.”

“Better and faster service helps to grow toward a significant customer base to whom you can offer an increasing number of products and services. Active investments in those kinds of winners should deliver the best stock returns in the longer term, as long as you buy growth at a reasonable price (GARP).”

“Stock selection is absolutely critical in our view, given the competition between the huge start-up ecosystem, existing players, and traditional financial sector incumbents attempting to defend old business models.”