Client Portfolio Manager

• Insight

India: The ascent of small and mid-cap stocks

By Robeco Asia Pacific Equities Team and the Canara Robeco India Offshore Equities Team.

The Indian equity market is undergoing a structural shift, with domestic investors driving capital into small- and mid-cap companies. These companies are benefiting from reforms and digitalization, offering high growth and alpha potential for the selective long-term investor.

Authors

Portfolio Manager

Top keywords

Summary

- Retail surge has seen greater investment into mid- and small-cap companies

- Government reforms and digitization are helping small to mid-cap firms develop

- Higher alpha potential but higher volatility compared to large-cap stocks

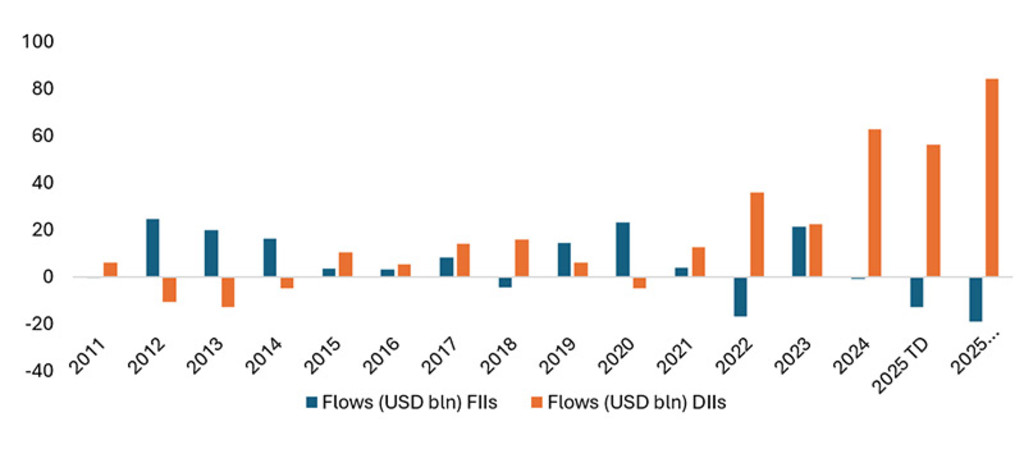

The Indian equity market is experiencing a profound transformation in investor preference toward small and mid-cap listed equities. Before we dwell further on this transformation, it is important to understand that a democratization of equity investing in the country has led to a surge in equity inflows from domestic investors. A near 40% CAGR in local institutional flows since 2019 has resulted in a dynamic transformation of equity market ownership. Foreign Institutional Investors (FIIs) who held a dominant 22% ownership share in Indian equities now hold only 18.6%. Conversely, Domestic Institutional Investors (DIIs) have become the dominating holders of Indian equities, constituting 30% of total ownership.

Figure 1: Annual flows from domestic and foreign institutional investors

Source: Kotak Institutional Equities, August 2025. The final column is 2025 data is annualized.

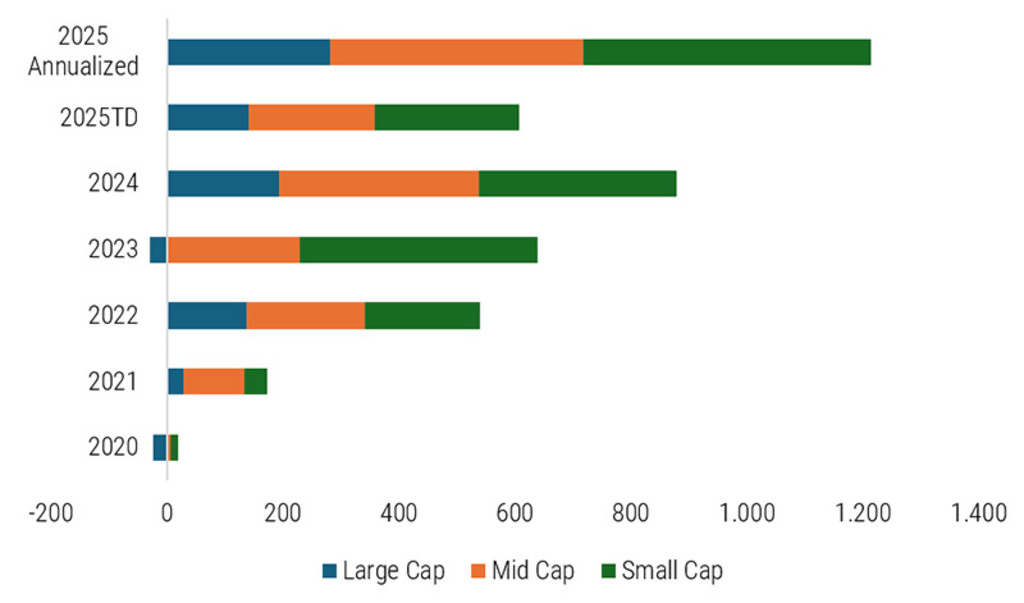

We see a clear and tangible evidence of domestic preference for small and mid-cap companies through an unrelenting flow of capital into dedicated small-cap, mid-cap and flexi-cap mutual funds by local investors.

Table 1: Classification of Indian stocks by market capitalization

Source: AMFI, SEBI, Category classification is as of June 2025

Investment explosions reflect India’s dynamic economy

Traditionally, foreign investors preferred investing institutional capital in the stability and liquidity offered by large, listed companies (large cap), viewing them as the primary proxies of India’s economic narrative. The Covid pandemic however shifted the narrative to a more nuanced story of broad-based growth, where a burgeoning cohort of smaller and mid-cap companies are becoming the engines of wealth creation.

This strategic allocation of capital is a strong reflection of the deep-seated structural changes that are reshaping India’s equity markets, its underlying economy and most importantly the emergence of brand-new fast-growing sectors such as digital insurance and beauty platforms, quick commerce1 and fintech companies.

Figure 2: Annual inflows into large, mid and small-cap funds (INR bln)

Source: AMFI, June 2025

The main drivers of the small-cap market

The sustained influx of domestic liquidity has fundamentally altered market dynamics. Previously, the small- and mid-cap segments were characterized by lower liquidity and higher volatility, often making them a difficult proposition for large-scale institutional investors. However, the sheer scale of inflows has improved liquidity and provided a robust demand floor, enabling a more efficient price discovery mechanism for small and mid-cap stocks.

The concentration of this capital, coupled with public listings from new, fast-growing sectors has begun unlocking value that was previously hidden or overlooked by the market. The buoyancy seen in small and mid-cap companies is inextricably linked to the broader Indian economic narrative. Over the past decade, the government has championed a series of reforms aimed at formalizing and digitalizing the economy, enhancing manufacturing capabilities, and boosting domestic consumption. These initiatives – from the implementation of the Goods and Services Tax (GST) to pushing for infrastructure development and incentivizing domestic manufacturing – have created an enabling environment for many companies, which were earlier more dominant in the informal economy.

Sustained investor interest has also been supported by a marked improvement in corporate governance and disclosure standards across the small- and mid-cap universe. Regulatory oversight has grown stricter, and the pressure from a more discerning investor base has compelled these companies to enhance transparency and financial reporting. This maturing of the ecosystem has reduced the historical risk premium associated with smaller companies, making them a more credible and attractive proposition for a wider audience of sophisticated investors.

What EM opportunities are out there?

Receive our newsletter to dive deep into EM investment opportunities.

Previously inaccessible benefits

Small and mid-sized enterprises, once mired in the complexities of an unorganized system, now find themselves with streamlined supply chains, expanded market access and most importantly, formal credit, allowing them to compete more effectively. This direct government support has not only boosted their bottom lines but has also injected a sense of long-term policy certainty, a crucial factor for investors.

The digital leap

The technological leap, particularly post-2020, has also been a game-changer. Digital platforms have revolutionized how small businesses operate, from customer acquisition and supply chain management to payments and credit access. The widespread adoption of digital tools, backed with some of the lowest bandwidth costs globally, has enabled these companies to scale at a speed and cost that was previously unimaginable. This technological empowerment has not only improved their operational efficiency but has also enhanced their data-driven decision-making, allowing them to compete with larger, more established players on a more equal footing.

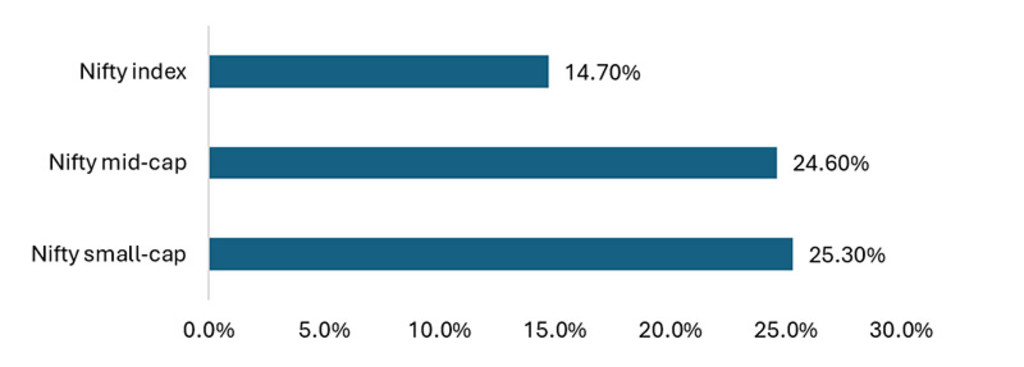

A combination of factors has led to small and mid-cap indices outperforming their large cap peers. Since 2020 as Figure 3 demonstrates, the mid- and small-cap indices have massively outperformed the benchmark large cap index.

Figure 3: Nifty index and sub-index: Compound annual growth rate annualized

Past performance is no guarantee of future results. The value of your investments may fluctuate.

Source: Bloomberg, 1 January 2020 to 2 September 2025

A source of alpha…

The outperformance of small and mid-cap companies, together with massive liquidity infusion into these indices has meant that the most optimal way to create alpha in India is to be able to successfully identify good quality, fast growing companies in these market cap segments. The below reasons highlight why discerning bottom-up stock selection in small and mid-caps is vital. Unlike large-cap stocks, mid and small-cap segments have a lower percentage of holdings by Foreign Institutional Investors (FIIs). This means their price movement is less influenced by foreign fund flows and more by domestic factors, which can be an advantage for domestic fund managers. Consequently, stocks from these sectors display a low correlation with global macro factors and offer a significant hedge for investors, who are looking at purely local factors.

…but a source of portfolio risk

While the alpha generation potential from small and mid-cap stocks is high, the higher volatility and lower liquidity in these segments remain real factors that can lead to sharp corrections, and a thorough due diligence process remains paramount. A fundamental approach, focusing on companies with solid fundamentals, sustainable business models, and prudent management is key. Rigorous stock selection is important to unlock asymmetric upside.

While there will be intermittent periods of froth and irrational exuberance, the booming demand for small- and mid-cap stocks in India is far more than a passing market fad; it is a structural validation of the country’s economic evolution. It signifies a maturing capital market, a financially empowered and fast-growing domestic investor base, and a burgeoning cohort of companies that are well-positioned to capitalize on India’s demographic dividend and policy-driven growth.

Table 2: Robeco’s flexi-cap strategy

Source: Robeco, September 2025.

Calibrated exposure to carefully researched small and mid-cap companies

An actively managed approach to Indian equities, which includes the right exposure to mid- and small-cap stocks, is in our opinion the optimal way to invest in Indian equity markets. The market’s inherent inefficiencies offer skilled investors the opportunity to generate alpha. Unlike mature Western markets where passive indexing dominates, India’s broader mid-cap and small-cap universe, with limited analyst coverage, allows active, bottom-up stock picking.

Robeco Indian Equities’ flexi-cap strategy allows us to invest across the market capitalization spectrum to select high growth companies. Flexi-cap enables institutional investors to capitalize on high-growth companies, diversifying beyond the concentrated large-cap stocks that often dominate passive funds. By dynamically selecting across the market spectrum, investors can outperform benchmarks by identifying emerging winners, managing risk during volatile cycles, and adapting to India’s rapidly evolving economy. We believe that a flexi-cap strategy is an optimal approach for navigating this risk-reward dynamic. Instead of being locked into a rigid allocation like multi-cap funds (where a compulsory allocation of 25% must be made to small, mid and large cap funds), a flexi-cap strategy offers the freedom to tactically shift between market capitalization based on market conditions, valuations and the macroeconomic environment. The flexi-cap approach, allocating 25% to 35% of its portfolio to small and mid-cap stocks while investing the remainder in large-cap stocks. This defined mix is designed to provide investors with a steady, long-term risk-reward together with strong downside protection against market volatility. Alpha is primarily generated by the small and mid-cap holdings, while large-cap stocks offer stability and significant downside defense during periods of market weakness.

This active, dynamic reallocation balances the risk and return, offering our investors an active investment solution to capture India's long-term growth story while mitigating the inherent volatility of its smaller market segments.

Footnote

1 Quick commerce, often called q-commerce, is a type of e-commerce focused on delivering goods to customers extremely fast

Important information

This information is for informational purposes only and should not be construed as an offer to sell or an invitation to buy any securities or products, nor as investment advice or recommendation. The contents of this document have not been reviewed by the Monetary Authority of Singapore (“MAS”). Robeco Singapore Private Limited holds a capital markets services license for fund management issued by the MAS and is subject to certain clientele restrictions under such license. An investment will involve a high degree of risk, and you should consider carefully whether an investment is suitable for you.