Quantitative investing

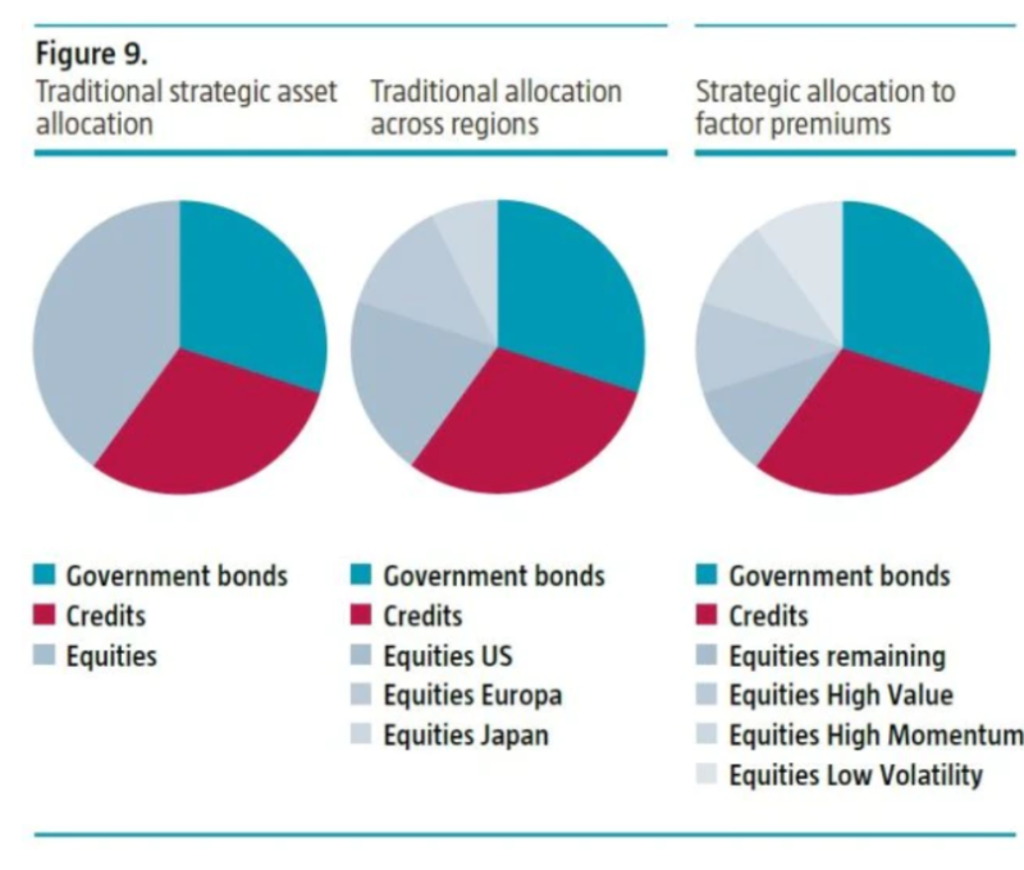

Traditionally a portfolio is constructed by distribution over asset classes (asset allocation), followed by allocation to subsegments such as regions or sectors. Factor investing applies strategic allocation according to factors.

The example below illustrates this process of moving from traditional strategic asset allocation towards strategic distribution according to factor premiums for equities.

Source: Robeco, Quantitative Research, 2014

A factor portfolio divides the equities class into premiums such as low volatility, value and momentum, irrespective of regions and sectors.

See also