Portfolio Manager

• Insight

European equities – Rising stars

With European stocks outperforming the US by a wide margin for the first time in years, investors have even more reason to question their regional allocation, degree of diversification, and opportunity set. Geopolitical shifts have set in motion developments that are likely to gain traction and could benefit European markets.

Authors

Top keywords

Summary

- After years of austerity, fiscal tailwind provides an attractive investment climate

- Investment opportunities abound beyond the defense sector

- Innovation, AI, Consumer and China rebound among the most promising

Ironically, when Donald Trump took office on 20 January 2025, it meant a US American ignited a European market revival. The 47th president’s isolationist’s approach to global trade and security has triggered swift, decisive and far-reaching decisions by European leaders after years of lethargy. As we have written about recently,1 2 3 the European market offers a broad pool of investment opportunities that go well beyond the themes of rearming Europe and German infrastructure.

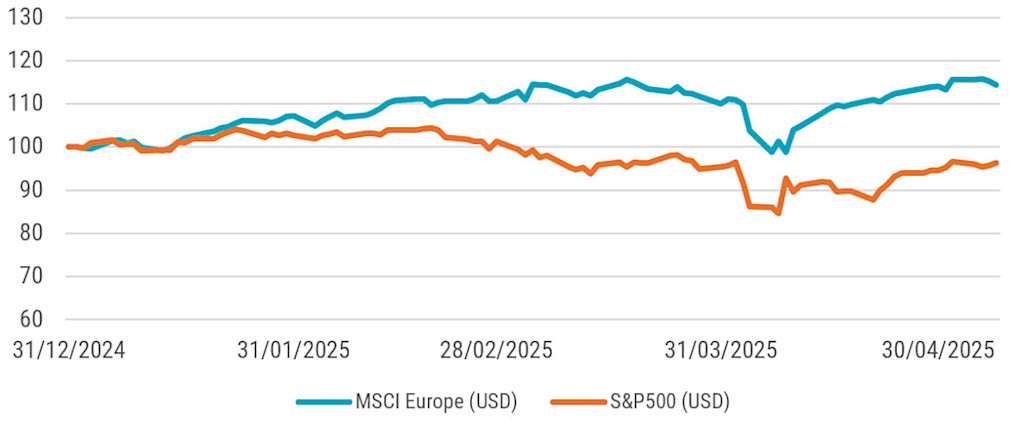

In our August 2024 insight ‘The stars align for European equities’, we showed the extreme valuation disconnect between US and Eurozone equities and the overreliance of world equities on the US stock market. The circa 15% year-to-date outperformance (see Figure 1) of Europe in US dollar terms has reduced the sector-neutral valuation discount to the US to 27% (from ~35% at the end of 2024)4 but it remains materially wider than pre-pandemic.

Figure 1: European equities outperform US stocks year-to-date

Source: Bloomberg, to 8 May 2025.

Past performance is no guarantee of future results. The value of your investments may fluctuate.

Investment flows have started to shift toward European markets, yet remain modest compared to previous outflows and the stark imbalance in geographical allocation. According to Bank of America, European equities saw USD 27.4 billion of inflows year-to-mid-April. While this is the largest inflow in this period over the past five years, it contrasts with a cumulative USD 534 billion of outflows since 2005. Thus, the opportunity from cheaper valuations, soft positioning and re-directing of investment flows remains largely intact.

A new hope amid old habits

As highlighted in previous notes, the writing was on the wall for these shifts. Pessimism against the region owing to long-term underperformance of the European market, political turmoil and a lack of convincing artificial intelligence innovations has been a long-lasting feature leading to peak ‘Sell Europe’ sentiment by the end of 2024.

The flood of US executive orders initially put additional pressure on Europe at first, but it is fair to say it triggered a much-needed reaction from European leaders, in particular in Germany, but also more broadly at the European level. Two main themes emerged:

Infrastructure spending and easing the debt ceiling: The recent German fiscal package includes a EUR 500 billion fund for public infrastructure upgrades over the next decade. This package aims to stimulate economic growth. In addition, defense spending above 1% of GDP will be exempted from deficit ceilings and the ‘Bundesländer’ or German federal states are no longer required to balance their budgets. The fiscal expansion is expected to benefit sectors like construction, energy, technology, and the broader German domestic economy.

Increase in defense spending: Germany plans to raise its defense budget to 2.5-3% of GDP, translating to an additional EUR 60-70 billion annually. The need to re-arm Europe, given the (partial) retreat by the US as its previous NATO partner, is also driving investment plans on a European level. This boost is expected to benefit major European defense contractors and the broader defense sector. The multiplier effect into the wider economy is relatively low.

The market reaction to these announcements has been euphoric. While the investment plan and easing debt brake in Germany was formally approved by the outgoing parliament, wider European investment plans such as those proposed by Mario Draghi5 or the European Commission6 are less concrete. Although other European countries like France, Italy or Spain do not possess the same fiscal leeway Germany does, the European Union in aggregate has more room for fiscal easing after years of prudence. This contrasts with the US whose deficit spending has fueled growth but also pushed debt levels significantly higher.7

We caution that realizing these investments is complex. Europe’s old habit of delaying or even blocking necessary reforms was already illustrated when German Chancellor Friederich Merz did not secure the needed parliamentary votes in the first election round, a first since World War II. The US announced sweeping reciprocal tariffs which are currently paused with final levels being negotiated, but won’t be eliminated completely, and will continue to dampen economic activity and global trade – offsetting European fiscal expansion.

Beyond fiscal push and defense lies a breadth of opportunities

So far, the main stock market beneficiaries have been concentrated in a small group of defense, construction, infrastructure, and German companies with high revenue exposure to domestic markets. The actual opportunity may be much broader over the long term.

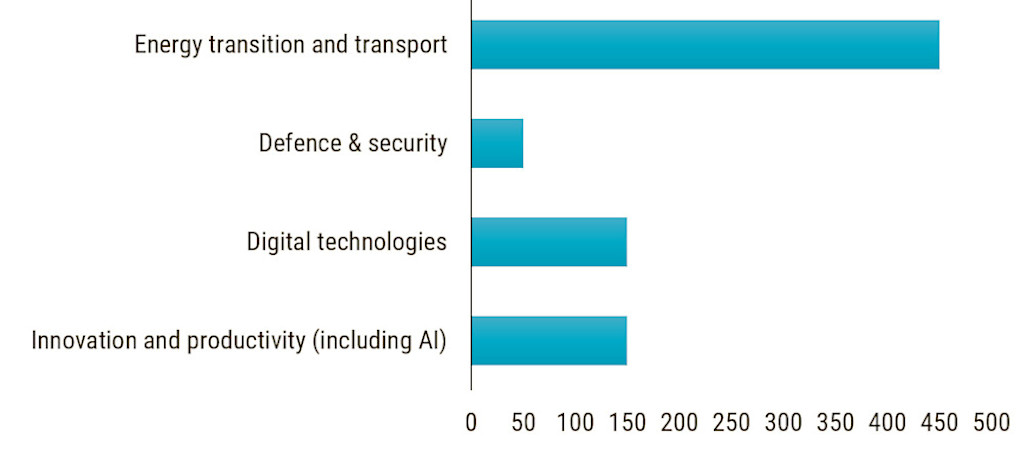

A look at Mario Draghi’s 2024 report on ‘The Future of European Competitiveness’8 reveals not only a need for investment in defence and energy technologies but digital technologies, innovation and productivity enhancements, as detailed in Figure 2.

Figure 2: Broad and deep investment needs in Europe 2025-2030 (in EUR billions

Source: The Draghi Report, September 2024.

Additionally, beyond fiscal push, European consumers have one of the highest savings rates (~15% versus the US ~4%) and sit on a total of EUR 33 trillion in gross financial assets of which a large chunk is sitting in low-yielding deposit accounts that can be mobilized for investment and consumption. The EU ‘Savings and Investment Union’ is an idea that has been floated for years and is being revived today, potentially to energize the region’s capital markets and to tap into this idle money.

The sectors set to benefit from Europe’s renewal

The prerequisites for interesting investment opportunities in listed European equities are in place and broadly spread across industries and themes. Independent of business models,9 the augmented fiscal optionality creates winners beyond the current beneficiaries of increased defense spending. We summarize a (non-exhaustive) list of opportunities here:

AI adopters and enablers: While Europe suffers from lacking foundational artificial intelligence (AI) models and infrastructure (data centers, cloud services, servers, chips)10, several industries and companies are beneficiaries of AI adoption and enabling. These range from software companies, semiconductor and equipment, capital goods, business services to energy networks.

Productivity enhancers: The Draghi report highlights the weaker productivity and a widening gap to the US as the most important driver of long-term growth underperformance of the region. Improvements in productivity through digitalization, industrial automation, improved commercialization, enhanced financing, and innovation would help to close the gap and reinvigorate growth. The technology sector, educational sector, pharmaceuticals, financials, consultancy and professional services are key in achieving this.

Consumer strength: Energy prices and rising rates have driven the saving rate from an already high average 11% to circa 15%.11 In comparison, US consumers are overspending and save only 3.9%,12 a significant decrease from the average 7% in the two years before the pandemic. European consumer markets are generally less advanced than in the US. Both offer significant catch-up potential (for example, in e-commerce penetration and payments).

China rebound: European industries and companies have high revenue exposure to emerging markets (~20% including China) and China (~8.5%). The China drag of recent years is priced in and global investors have significant underweight positions in China. Small economic improvements and stimuli could boost industries and companies doing business in the region. The consumer sector, medical technology, semiconductor (equipment), and industrials are potential beneficiaries.

Innovation gap: Next to adverse demographics, the key driver behind the rising productivity gap in the US has been low investment rates (about half of US spending) and a slow shift in research and innovation spending away from traditional European sectors to new disruptive technologies. Technology, pharmaceuticals, life sciences and the industrial sector could benefit from closing that gap.

Infrastructure (including housing, health care, financial etc.): Infrastructure has been highlighted as one of the key investment areas for both the German fiscal package and proposals at a European level. Infrastructure must be viewed more broadly than roads, bridges and buildings. The scope also includes healthcare, education, and financial infrastructure, all of which play a critical role in enabling long-term growth. As a result, sectors such as healthcare, financial services, communications, and infrastructure-related industries stand to benefit.

Energy intensity reduction: European energy-intensive industries (EIIs) have higher energy prices compared to the US, reducing their competitiveness in global markets. Ensuring access to a stable energy supply, focusing on decarbonization needs, energy independence and lower energy costs will help the EIIs to overcome a competitive disadvantage and provide a boost to growth and profitability. Industrials, cement, chemicals and other materials companies could be key beneficiaries.

Funding gap: The move toward more expansionary fiscal spending could be enhanced by mobilizing and re-patriating private investments through various channels as envisioned by the Savings and Investment Union. Bank lending, private markets, securitization and public market investments can help fill the funding gap.

Figure 3: Investment topics emerging from European investment and spending revival

Source: Robeco Schweiz AG.

The companies are listed for illustrative purposes only and are not necessarily components of the Robeco Sustainable European Stars strategy. This is not a buy, sell or hold recommendation for any particular security. No representation is made that these examples are past or current recommendations, that they should be bought or sold, nor whether they were successful or not.

Get the latest insights

Subscribe to our newsletter for investment updates and expert analysis.

Footnotes

1 The stars align for European equities, Sustainable European Stars, Robeco, August 2024

2Sustainable European Stars, Annual Review 2024 – Robeco, January 2025

3Monthly Outlook, European equity – it’s always darkest before the dawn, 8 January 2025.

4Morgan Stanley, European Equity Strategy, Moment of Truth, 11 March 2025.

5Draghi Report, September 2024.

6European Commission, Joint White Paper for European Defence Readiness 2030, Brussels, 19 March 2025

7J.P. Morgan, Equity Strategy: Could some of the long-held US positives, and European negatives, be turning?

8The Draghi report: A competitiveness strategy for Europe (Part A) and In-depth analysis and recommendations (Part B).

9The stars align for European equities, August 2024; A view of attractive and diverse business models in Europe was presented.

10The “hyperscalers” are all US companies (Amazon, Microsoft, Google) and hold a 70-75% market share in Europe with the remainder distributed among European providers.

11Eurostat, 13 January 2025, Q4 2024

12 Federal Reserve Bank of St. Louis, Personal Saving Rate, March 2025.