Strategist

• Insight

What to do when safe havens turn into stormy waters

The traditional safe-haven asset of US Treasury bonds is not as safe as it once was, say Peter van der Welle, Laurens Swinkels and Martin van Vliet, in an excerpt of a special topic produced for our five-year outlook.

Authors

Head of Solutions Research

Strategist

Summary

- Safe-haven assets can withstand turbulence and keep their value over the long term

- US Treasuries’ safe-haven status has been steadily eroded by deficits and inflation

- Gold, defensive equities and fiat currencies like the Swiss franc are good alternatives

A safe-haven asset can retain or even gain value during market turbulence or stock market downturns. They are widely accepted and easy to sell, even during crisis periods, as they tend to be relatively insensitive to new information about whatever is causing the panic. In the long run, safe-haven assets keep their value in real terms.

Government debt has long been seen as a natural safe haven. However, investors have begun to question governments’ willingness or ability to pay back bondholders without causing high inflation, which reduces their safe-haven status. At other times, central bank policies keep interest rates below inflation, reducing their long-term store of value.

Several episodes in the past three years have cast further doubts. The Covid pandemic prompted governments to take unprecedented fiscal measures to counter the economic impact of lockdowns, causing deficits and government debt levels to reach new highs, raising concerns on debt sustainability.

The role of government bonds as a hedge against equity market volatility was further challenged in 2022, when they posted large negative returns during that year’s stock market falls, offering little diversification benefits. The UK Gilt market experienced its own crisis in September 2022 when the proposed budget of Liz Truss triggered a sell-off in the vast liability-driven investment market, leading to her resignation as prime minister.

More recently, French government bonds (OATs) came under pressure after President Macron called for snap elections in June 2024. This surprised bond markets and caused the yields on OATs to widen significantly versus German Bunds.

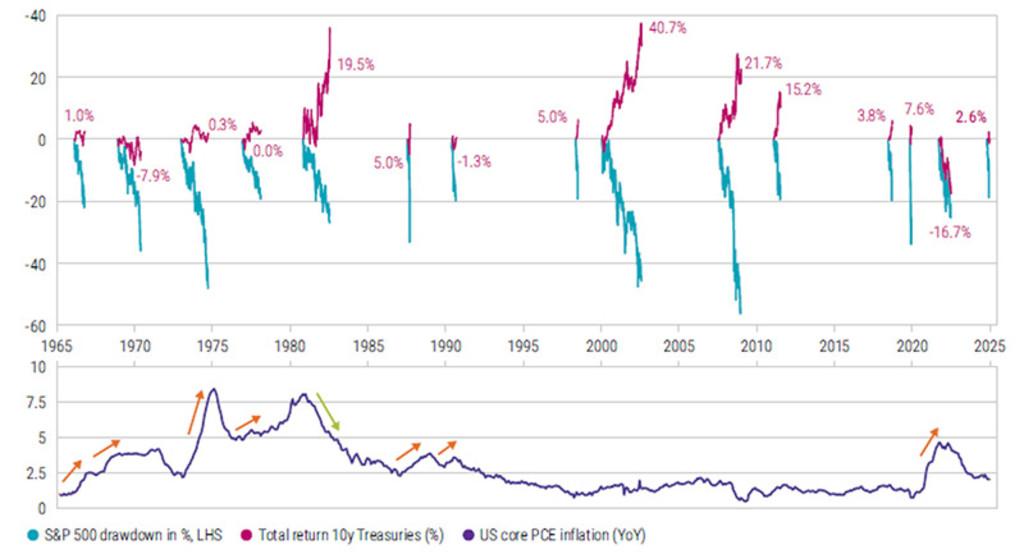

To assess whether the safe-haven status of US Treasuries has truly been compromised, we began by compiling an overview of historical equity market corrections exceeding 15% over the past 60 years. We then analyzed the performance of 10-year Treasuries during these corrections. Figure 1 below illustrates a total return of approximately 2.5% during the nearly 20% correction in the S&P 500 that began in February 2025 and ended on 9 April.

This 2.5% return stands in stark contrast to the high returns seen after the dotcom bust (2000/2001) and the Global Financial Crisis (2008/2009), when the Federal Reserve significantly lowered short-term interest rates. However, it is notably better than the 16.7% negative return in 2022, when the Fed aggressively raised rates in response to high inflation, and better than the returns during the 1960s and 1970s, when high or rapidly rising inflation caused similar issues.

Figure 1: Performance of 10-year Treasuries during S&P 500 corrections of at least 15%

Past results are no guarantee of future performance. The value of your investments may fluctuate. Source: Robeco, July 2025.

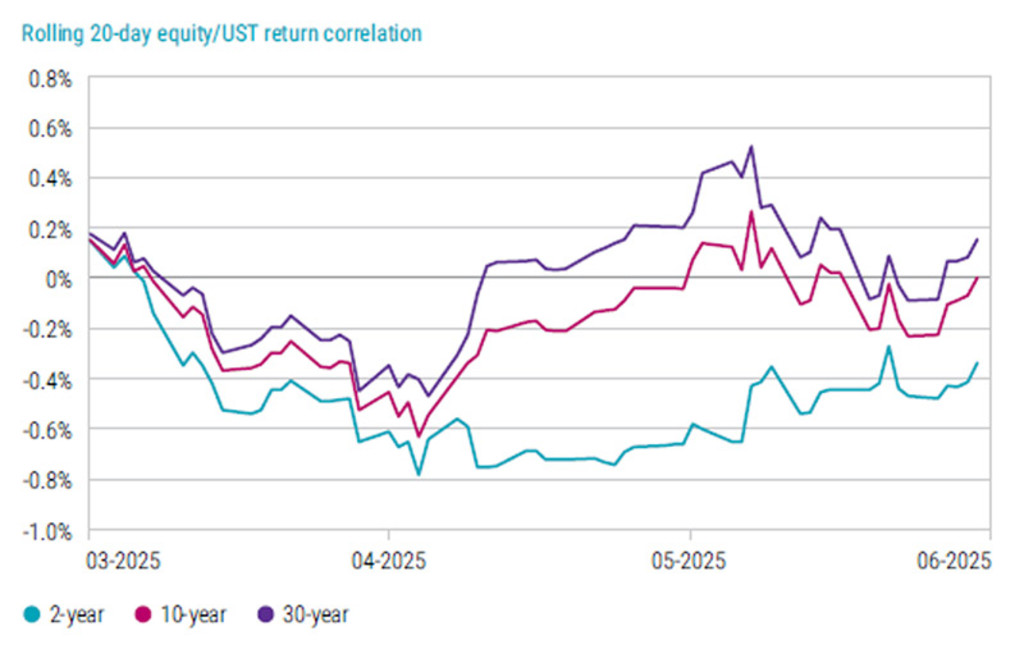

At first glance, 10-year Treasuries thus appear to have fulfilled their expected role: preserving capital or delivering a positive return during a significant equity market downturn. However, a closer look at the panic phase of the correction – late March to mid-April 2025 – reveals a different picture. During this period, 10- and 30-year bonds failed to perform their safe-haven function.

In fact, the correlation between equity and bond returns turned from negative to positive. Interestingly, the equity/bond correlation for 2-year Treasuries remained negative (see Figure 2 below), indicating that short-term bonds continued to act as safe havens. This is somewhat surprising, given that the trade tariffs announced in early April – though temporarily inflationary – would have been expected to impact shorter maturities more severely.

Figure 2: Correlation between US Treasuries and US equity markets

Past results are no guarantee of future performance. The value of your investments may fluctuate. Source: Robeco, June 2025.

Get the latest insights

Subscribe to our newsletter for investment updates and expert analysis.

Can other asset classes be safe havens?

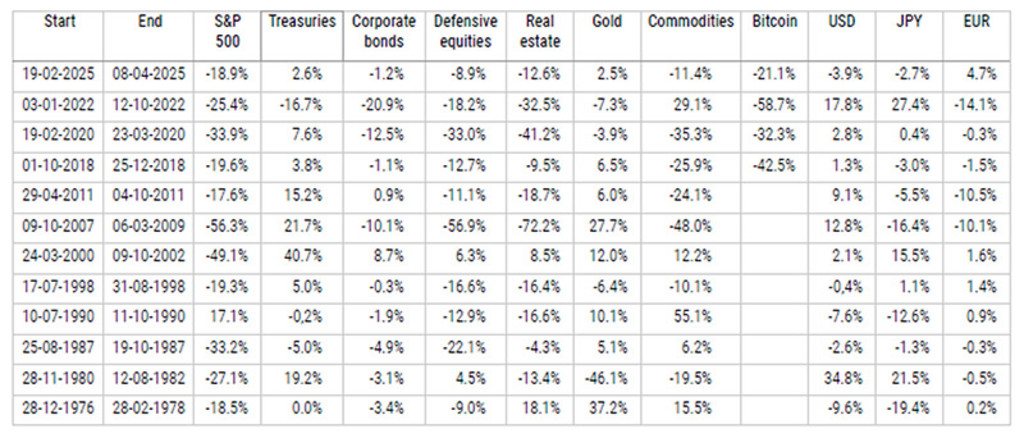

It’s not just US Treasuries that can act as a safe haven of course. Gold has been considered one for centuries. Other asset classes include highly rated corporate bonds, defensive equities and fiat currencies – but are they reliable? The table below shows asset class returns during major falls in the S&P 500 since the 1970s.

Table 1: Asset class returns during equity market corrections

Past results are no guarantee of future performance. The value of your investments may fluctuate. Source: Robeco, LSEG, June 2025.

Highly rated corporate bonds can sometimes have lower interest rates than government bonds but are not reliable safe havens. This is due to their small volume and sensitivity to changes in credit risk, which is in turn vulnerable to a changing macroeconomic landscape. Their liquidity tends to dry up during crisis periods, and so they may not be good stores of long-term value during times of financial repression.

Inflation-linked bonds protect against inflation but also tend to become less liquid during crises due to limited supply. They are however a relatively new asset class, and future scenarios with increased inflation risk may increase their safe-haven status, especially due to their long-term store of real value.

Defensive stocks that supply essential goods such as food, utilities, and health care have lower risk. Table 1 shows that defensive equities outperformed the general equity market during large drawdowns on average by more than 10%. They are less prone to long-term real value erosion than government debt or cash, and may therefore be a better store of value.

Turning to gold for millennia

And then there is gold, which has historically been used as a foundation for paper currency systems due to its rarity, durability, and ease of transaction. It has maintained its value over millennia; banks recognize gold as Tier 1 capital under Basel regulations. However, gold can be stolen and does not generate income, incurring storage costs instead.

Table 1 shows that during Global Financial Crisis, gold outperformed all other asset classes. Commodities, which are dominated by energy products such as oil, also tend to perform well during crash periods, such as in 2022 when the Russian invasion of Ukraine caused oil and gas prices to soar.

Finally, traditional currency markets such as the US dollar and Japanese yen perform well during equity drawdowns. Since its introduction, the euro has not been such a good safe haven as the other two currencies, but it outperformed in the last drawdown caused by the Trump tariffs. A stealth erosion of international USD reserve holdings has been ongoing for the last decade.

Taking a diversified approach

In conclusion, investors who are not able to predict the nature of the next crisis may need to take a diversified approach toward safe-haven assets. Since US Treasuries have gone from safe haven to stormy waters, German Bunds, defensive equities, gold, commodities, and fiat currencies may offer better protection during the next episode of market turbulence.

This article is an excerpt of a special topic in our five-year outlook.