Co-Portfolio Manager

• Insight

Battery recycling – a solvent solution for critical mineral supplies?

As sales of electric vehicles accelerate, so does the need to recycle their batteries. This article explores why battery recycling matters for the environment, for raw material supplies and for the economy. It also looks at the evolving technologies, regulations, and business models that make battery recycling a promising long-term investment opportunity.

Authors

Top keywords

Summary

- Disposal of EV batteries poses environmental risks

- Batteries are a source of highly demanded critical metals

- Recycling technologies are accelerating but maturity and scale needed

Electric vehicles (EVs) are a cornerstone of the global transition to a low-carbon economy. But while they eliminate tailpipe emissions, their batteries – packed with critical raw materials like lithium, nickel, and cobalt – pose a new sustainability challenge for the environment.

Figure 1 - Recycling rates are rising but currently inadequate

Ratio of recovered material to annual demand for important critical metals.

Source: Robeco, 2024.

Recycling batteries offers a multi-functional solution that reduces environmental waste and pollution, secures access to critical minerals, while also promoting cost and resource efficiency by reusing materials in the production process.

Despite its powerful potential, recycling must overcome some hurdles of its own. First, EV batteries are resource-intensive to produce and difficult to sustainably dispose. Second, the recycling industry is still nascent, with profitability hinging on volatile raw material prices and regulatory support.

Moreover, questions remain on whether recycling can become a reliable, scalable, and profitable part of the battery value chain. Though now seen as economically unprofitable at best and waste at worst, framed another way, end-of-life batteries can be seen as small mobile mines. In a world facing geopolitical tensions and looming raw material shortages, they represent a powerful opportunity to recover critical minerals and reshape supply chains.

For companies, battery recycling could become a key lever for reducing emissions, lowering supply chain risks, and unlocking new business models and revenue streams. For investors, it’s a chance to get ahead of a structural shift – one that’s being shaped by regulation, innovation, and the growth of EV adoption.

A ‘battery’ of recycling solutions

Today and for the near future, most recycled material will continue to come not from used EVs but from production scrap – defective or excess batteries generated during manufacturing.

Moreover, battery reuse is also a potential option in some markets. Norway is an excellent case study. High EV adoption rates mean it has a steady feedstock of end-of-life (EOL)1 batteries most of which are being repurposed for second-life applications.2

Table 1 – Norway’s first-hand experience in second-hand markets (Li-ion EV batteries)

Norway leads Europe in EV adoption and reuse of lithium-ion (Li-ion) batteries at the end of their first EV life. In 2024, more than 93% were used in second life applications such as stationary energy storage.

Source: Norwegian Environmental Accounts for End-of-Life Collection & Recycling, April 2025.3

Complex forms of recycling are also in the works including hydro- and pyro-metallurgy which use water-based solutions or intense heat to extract and recover metals from batteries and electronic waste. Hydrometallurgy is currently the leading recycling technology, offering high recovery rates with lower energy use than pyrometallurgy.

Direct recycling – which allows the recovery, regeneration, and reuse of battery components directly without breaking down the chemical structure – is promising but remains unproven at scale.

The industry is coalescing around three main recycling technologies:

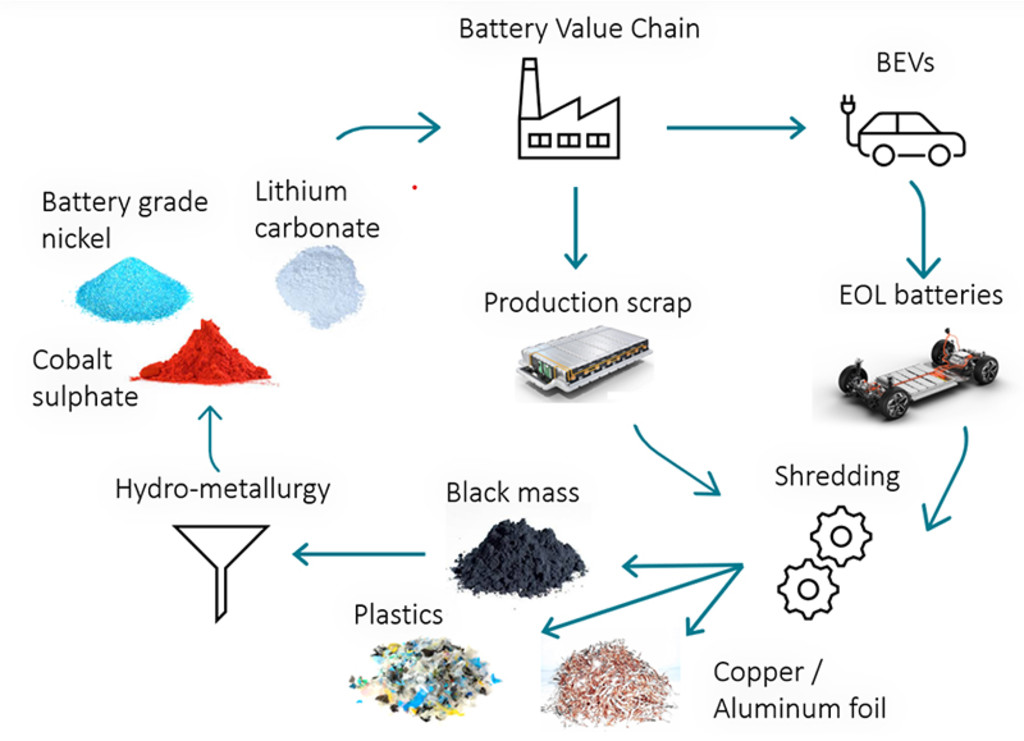

Hydrometallurgy: The current standard, especially in Asia. It involves dissolving metals from shredded battery material (‘black mass’) using chemical solutions (see Figure 2).

Pyrometallurgy: A high-temperature process that’s energy-intensive but simpler in terms of material handling.

Direct recycling: A lab-scale approach that preserves the integrity of electrode materials, particularly cathode materials, but still faces challenges with commercial scalability.

Figure 2 – Battery recycling value chain of (hydrometallurgical process)

Source: Robeco, 2024.

China dominates…

From a market perspective, China is far ahead, accounting for over 80% of global recycling capacity. Most of the major players are vertically integrated which means they are battery manufacturers or cathode producers that have added recycling at the back end of production. Those include CATL and GEM Co. which are not only battery giants but also recycling powerhouses.

Elsewhere, the picture is more fragmented. Europe and the US are still building capacity, with a few promising pure-plays such as Redwood Materials emerging. Moreover, South Korea’s SungEel HiTech is also a pure-play to monitor given its ties with the Samsung Group.4

Our analyses show the most viable business model for non-vertically integrated players appears to be toll manufacturing – charging a fixed fee per metric ton of material processed. This model insulates recyclers from raw material price volatility and aligns with the Extended Producer Responsibility (EPR) frameworks emerging in the EU and some US states.5

Get the latest insights

Subscribe to our newsletter for investment updates and expert analysis.

The EU legislates…

Meanwhile, the urgency for solutions is building, especially in Europe. The EU’s New Battery Regulation, introduced in 2024, mandates progressively higher levels of recycled content in EV batteries, alongside strict recovery and recycling efficiency targets. By 2031, new batteries sold in the EU must contain at least 16% recycled cobalt, 6% recycled lithium, and 6% recycled nickel, with even higher thresholds by 2036.6

These requirements are legally binding and will directly impact the ability of manufacturers to sell into the European market. This regulatory push is accelerating demand for high-quality recycled materials and creates a clear incentive for OEMs and battery producers to secure reliable recycling partnerships.

At the same time, geopolitical tensions and resource nationalism are making supply chain resilience a top priority. Recycling offers a way to reduce dependence on mined materials and to localize critical parts of the battery value chain – especially for regions such as Europe that lack domestic mining capacity. In this context, battery recycling is not just a sustainability initiative – it’s a strategic imperative.

We are encouraged that some of our integrated battery manufacturers holdings are already at the forefront of the transition

The investment outlook

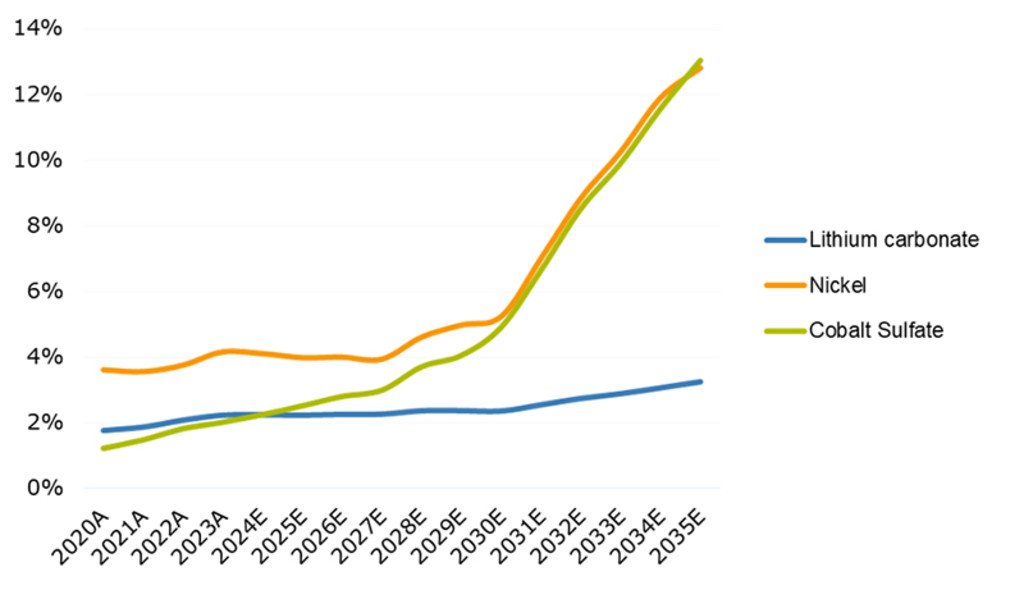

The outlook is promising but nuanced. Our model suggests that by 2035, recycled materials could meet over 12% of global demand for nickel and cobalt, and nearly 4% for lithium. That’s significant but still means recycling alone won’t solve supply constraints.

Commercialization is underway, but uneven. Most companies are still in the early stages – building capacity, refining processes, and securing feedstock. The economics are highly sensitive to raw material prices, and capital intensity remains a barrier.

We’re closely monitoring developments across the battery recycling value chain and are particularly encouraged that some of our integrated battery manufacturers holdings are already at the forefront of the transition. This has strengthened our conviction in their long-term investment cases and reaffirmed our confidence in the strategic foresight of their management teams.

Their leadership in adapting to evolving sustainability requirements means they are well positioned to capture future value and mitigate future risks. Moreover, we also believe investable opportunities will emerge where regulation, technology, and business models align – such as toll recyclers with strong OEM partnerships.

Footnotes:

1The performance of EOL batteries drops to only 20-30% of its original capacity, making it insufficient for EVs but suitable for other applications.

2In February 2025, 95% of all new passenger cars sold in Norway were electric powered models. Bloomberg, March 2025.

3Miljøregnskap for Autoretur 2024, Rapport No. 10-2025, Samfunnsøkonomisk Analyse AS. April 2025.

4According to Bloomberg, Samsung SDI and C&T have a combined ownership of 13% of SungEel HiTech.

5The Extended Producer Responsibility (EPR) policy approach is a group of economic instruments that raise revenues and set incentives for the collection and recovery of material at the post-consumer stage of the product lifecycle. OECD, Policy Perspectives, Policy Paper No. 41. 2024.

6Regulation (EU) 2023/1542 concerning batteries and waste batteries

Important note:

The companies referenced are for illustrative purposes only in order to demonstrate the investment strategy on the date stated. The companies are not necessarily held by the strategy. This is not a buy, sell or hold recommendation, nor should any inference be made on the future development of the company.

Important information

The contents of this document have not been reviewed by the Securities and Futures Commission ("SFC") in Hong Kong. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice. This document has been distributed by Robeco Hong Kong Limited (‘Robeco’). Robeco is regulated by the SFC in Hong Kong. This document has been prepared on a confidential basis solely for the recipient and is for information purposes only. Any reproduction or distribution of this documentation, in whole or in part, or the disclosure of its contents, without the prior written consent of Robeco, is prohibited. By accepting this documentation, the recipient agrees to the foregoing This document is intended to provide the reader with information on Robeco’s specific capabilities, but does not constitute a recommendation to buy or sell certain securities or investment products. Investment decisions should only be based on the relevant prospectus and on thorough financial, fiscal and legal advice. Please refer to the relevant offering documents for details including the risk factors before making any investment decisions. The contents of this document are based upon sources of information believed to be reliable. This document is not intended for distribution to or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Investment Involves risks. Historical returns are provided for illustrative purposes only and do not necessarily reflect Robeco’s expectations for the future. The value of your investments may fluctuate. Past performance is no indication of current or future performance.