Head of Sustainable Investing

• Insight

How sustainable investing can stay the course amid disruption

Today’s geopolitical landscape has placed sustainable investing in a state of greater flux than ever. Carola van Lamoen, Robeco’s Head of Sustainable Investing and Lucian Peppelenbos, Robeco’s Climate & Biodiversity Strategist explain how Robeco is navigating strong currents of scrutiny on issues such as financial performance, a decelerating transition, investing in arms and defense as well as stewardship and engagement.

Authors

Head of SI Thought Leadership and Climate & Biodiversity Strategist

Summary

- Financial performance is just one of many investment goals

- Flexibility of approach is critical as investors confront on the ground realities

- Stewardship is a critical tool to be proactively defended

“Sustainable investors pursue more than just stock performance – that’s clear from the broad range of sustainability features captured in portfolios,” says Robeco’s Head of SI, Carola van Lamoen. “Those range from mitigating ESG risks to reducing environmental impact such as pollution, waste, and resource use.” SI strategies must often be balanced across multiple objectives, creating trade-offs across expected outcomes.

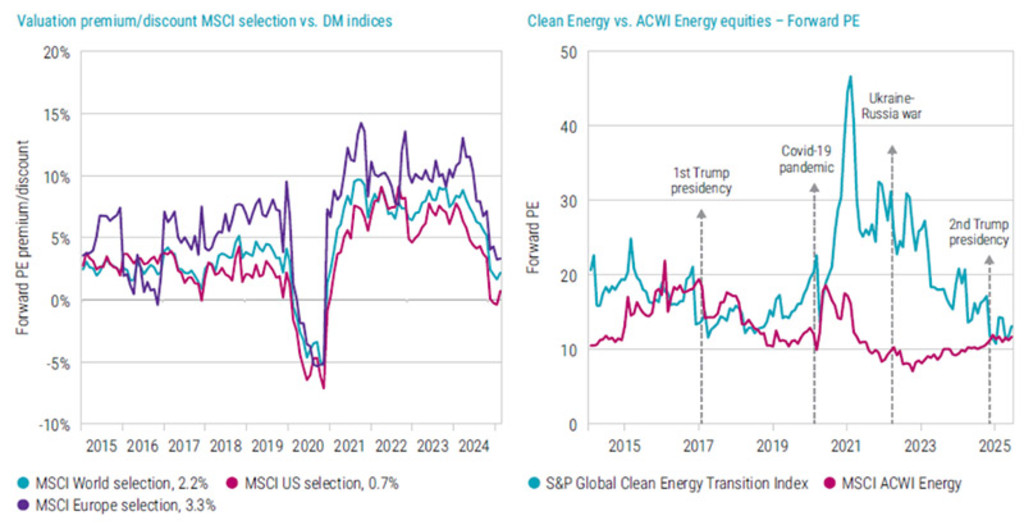

She says, these competing objectives are partly reflected in SI performance, which may diverge from broader benchmarks – sometimes outperforming, sometimes lagging. “Throughout the past decade, ESG equities have demanded a higher valuation premium relative to broader developed market indices” (measured as the forward-price-to-earnings ratio in Figure 1).

“However, those spreads have reduced of late and it is still unclear how shorter-term performance will evolve.” Despite declines, she remains optimistic, noting that lower valuations create attractive entry points for investors. She also stresses that short-term results, whether historical or present, do not predict long-term outcomes. This is especially relevant when considering systemic risks of climate change, which are rarely factored into mainstream investment models.

Figure 1 – Like any stock, ESG valuations shift over time

Source: Bloomberg, Robeco, May 2025.

Pricing climate risk

According to Lucian Peppelenbos, Robeco’s Climate and Biodiversity Strategist, climate risk is not simply a background factor, but a material risk with economic costs. This is why it plays a role in Robeco’s five-year capital market return assumptions. He says costs can arise from transition risks –for example, higher carbon prices or tighter regulations – or from physical risks such as when extreme weather disrupts supply chains, destroys physical assets or diminishes demand for a product or service. “The pricing of climate risk is still evolving, and investors who can accurately assess these dynamics should be better positioned to outperform over the long term (all else equal).”

He adds that Robeco’s fifth annual Global Climate Investing Survey1 which found that nearly half (49%) of global institutional investors believe society is doing “much too little and much too late’. There was even a slight increase in investors concerned that lacking policy action was pushing us toward a ‘hot house world’ (from 8% to 11% since 2024).

“Investors are resetting their expectations on the speed of policy action and re-considering their investment options. For Robeco that means leaning into ‘transition leaders’: high-emitting companies that are rapidly decarbonizing relative to sector peers and credibly transitioning toward a lower-carbon economy.” He summarizes that transition leaders are “key nodes on the net-zero adoption curve – helping scale decarbonization across the broader economy so we can reach net-zero goals faster.”

Robeco is leaning into ‘transition leaders’: that are rapidly decarbonizing relative to sector peers and credibly transitioning toward a lower-carbon economy

Net zero is not a linear transition

Net-zero investor initiatives got off to a rocky start. Their launch at COP26 in Glasgow in 2021 was understandably celebrated as a watershed moment, with USD 130 trillion of private capital waiting to be deployed for the net-zero transition. In hindsight, however, it vastly oversimplified the net-zero challenge and inflated investor expectations on the speed of transition because they failed to consider the critical role of government in the process. From railways to the internet, great transformations – both past and present – are based on public sector investment.

Adopting and adapting

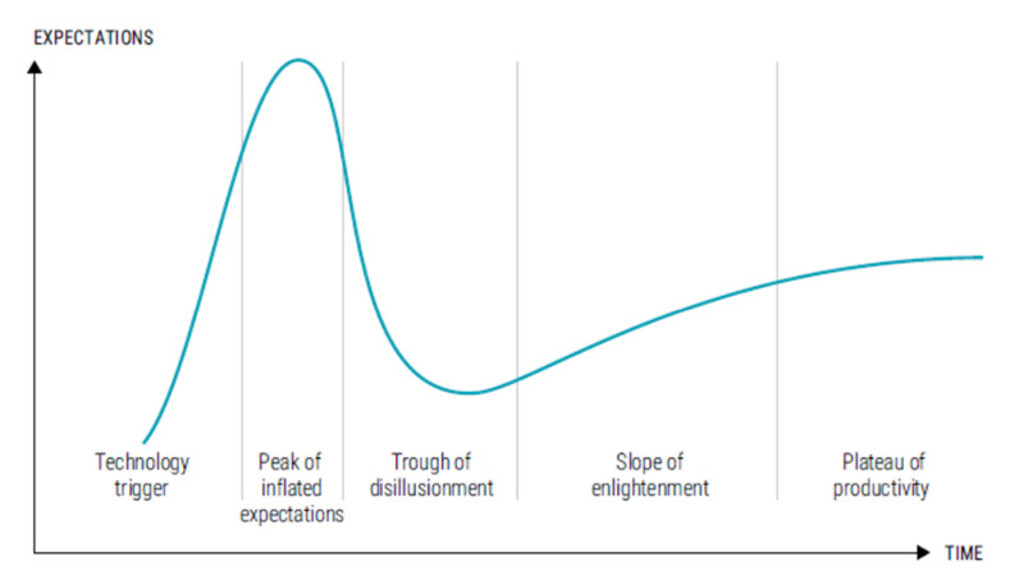

“Looking ahead, we believe that net-zero initiatives will follow the same learning curve as other important trends: from their breakthrough birth through to productivity gains and scaled adoption,” explains Peppelenbos.2

“The science hasn’t changed, so committed investors are staying the course, albeit with different tactics.” He says that the singular focus on portfolio decarbonization has created obstacles for the broader uptake of SI strategies. However, net-zero initiatives are finding newfound momentum via transition finance based on forward-looking emission analytics. He says the narrative has evolved from “reducing financed emissions toward financing the reduction of emissions.”

The narrative has evolved from ‘reducing financed emissions toward financing the reduction of emissions'

This can be seen in the positive evolution as more and more countries decouple economic growth from increasing emissions which “brings peak emissions within reach,” he notes.3 Unfortunately, this long-term trend is unlikely to accelerate in the current geopolitical landscape marked by fragmentism and nationalism. “Despite stalling policies, the imperative for climate action is only increasing.”

Figure 2 – Innovation-adoption curve

Source: Gartner Research, Robeco.

Keep up with the latest sustainable insights

Join our newsletter to explore the trends shaping SI.

Defense investing: A delicate dilemma

With regional conflicts intensifying and war in Ukraine and the Middle East, the debate around investing in defense has resurfaced in earnest.

In June, NATO members agreed to raise defense spending to 5% of their respective national GDP. Similarly, in spring the EU’s ‘ReArm Europe/Readiness 2030’ mobilized EUR 800 billion to support the defense of Member States. Van Lamoen explains that as countries ramp up spending to counter emerging threats, the defense sector is poised for structural growth which could benefit some types of SI portfolios. “While controversial weapons are categorically excluded in Robeco’s entire investment range, conventional defense and non-lethal support industries have always been eligible for investment within our mainstream strategies.” 4

She emphasizes that the evolving geopolitical landscape demands flexibility in investment strategies, and sustainable investors must be prepared to engage with sectors that contribute to societal resilience.

Table 1 – Robeco’s defense and weapons exclusions

Source: Robeco, 2025.

Stewardship: Amplifying voices and votes

With naturally long-term investment horizons and the wider public as their beneficiaries, institutional investors are deemed well suited to effectively advocate for long-term value creation and a more sustainable economy. Van Lamoen says that despite significant advances, stewardship activities have come under pressure – and not just in the US. “European regulators are looking to make corporate law more ‘business friendly,’ which may also impact company transparency and ESG disclosures moving forward.”

She’s concerned that deteriorating conditions are negatively impacting the effectiveness of stewardship efforts, with fewer resolutions and a reluctance to take a public stance on issues. She urges shareholders to take steps to fortify their influence. That means engaging regulators, refining guidance, and developing industry standards that ensure all shareholders retain a meaningful voice and vote. “With concerted action, stewardship can reassert its powerful influence for steering corporate behavior.”

Conclusion

While acknowledging challenges, both see opportunities. “As investment pioneers, we’re catalyzing crises toward innovation. We look beyond conventional investment frameworks to identify pragmatic transition solutions that enable the shift from today’s complex realities to tomorrow’s net-zero economy,” says Peppelenbos. Van Lamoen adds that stakeholder engagement is also a significant force in influencing corporate behavior, and Robeco is proactively working with regulators and policymakers to ensure all shareholders have a voice.

We look beyond conventional investment frameworks to identify pragmatic transition solutions that enable the shift from today’s complex realities to tomorrow’s net-zero economy

This article is an excerpt of a special topic in our five-year outlook.

Footnotes

1 Robeco Global Climate Investing Survey 2025, June 2025.

2 The Gartner Cycle describes the hype-adoption cycle of innovative trends in business and society.

3 From Our World in Data using data from Eurostat, OECD, World Bank, and Global Carbon Budget, accessed June 2025.

4 Robeco deems controversial weapons to be cluster munitions, anti-personnel mines, white phosphorus and depleted uranium ammunition, along with chemical, biological and nuclear weapons. Nearly all are banned under international treaties. These are part of Level 1 exclusions and apply across our entire investment range, making the companies ineligible for investment.