Strategist

Get the latest insights

Subscribe to our newsletter for investment updates and expert analysis.

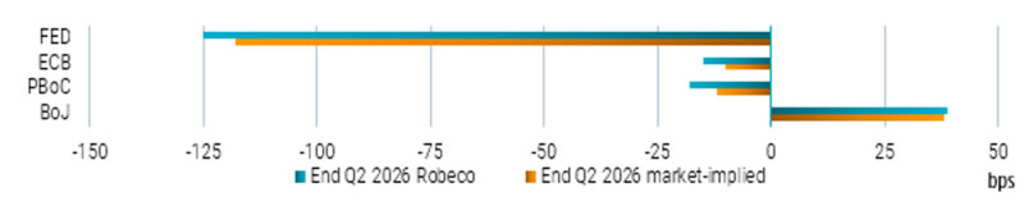

In this edition of the Central Bank Watcher, we explore what’s next for the Fed, ECB, PBoC, and BoJ, and how shifting policy trajectories are shaping yield curves worldwide.

There is a long-standing market belief that the ECB tends to follow the Fed with a delay. However, this assumption has proven inaccurate over the past 18 months. In fact, the ECB has been ahead of the Fed in easing monetary policy and has already returned to a neutral stance.

We suspect the Fed will soon follow the lead of the ECB on a rate-cutting path toward neutrality. Indeed, following the recent slowdown in job growth and significant downward revisions, expectations for rate cuts resuming on 17 September have now become the consensus. Nonetheless, we believe the Fed will be constrained in its ability to go ‘all-in’ on easing, given the inflation side of their mandate and despite the seemingly relentless political pressure. Historically, central banks that have yielded to pressure from their country’s leader on interest rate decisions have often faced the consequence of elevated inflation.

The ECB seems to be entering a prolonged pause in their rate cycle. In the press conference after the September ECB meeting President Lagarde expressed an optimistic view on economic conditions in the euro area, while signaling an end to the disinflation phase.

In China, the PBoC recently indicated a preference for holding rates steady. However, persistent issues in local government finances and the real estate sector, ongoing trade tensions, and the potential for a slowdown in credit growth suggest the PBoC’s rate-cutting cycle may not yet be complete.

In regards to the Bank of Japan, we are more hawkish relative to markets, mainly due to the fact that we believe the BoJ can increase its policy rate earlier than the market expects.

Source: Bloomberg, Robeco, based on money market futures and forwards, 12 September 2025

Subscribe to our newsletter for investment updates and expert analysis.